Dear Reader,

It was a volatile week for Indian equity markets, benchmark indices managed to hold their ground better than the broader market, edging up 0.39 percent even as the small-cap index slipped by 0.50 percent. The volatility was on account of geopolitical tensions, rising crude oil prices, and persistent selling pressure from foreign institutional investors.

Sector performance was mixed with PSU Bank stocks gaining 5.5 percent gain, and energy stocks added 2.4 percent. On the other side, Auto, IT, and Media indices all ended the week in the red. Notably, IT stocks came under pressure especially because of the global artificial intelligence summit in the country.

Adding to the uncertainty, mixed signals emerging from US-Iran peace talks kept markets on edge and lent further support to elevated oil prices. Foreign institutional investors, meanwhile, extended their selling streak into a second consecutive week, offloading equities worth Rs 637.68 crore.

Across the Atlantic, in a holiday-shortened week, Wall Street managed to close higher, even as the Supreme Court struck down the Trump administration's sweeping global tariffs. Rather than treating the ruling as a setback, markets took their cue from President Trump, who not only signalled his intent to press ahead with the tariffs but actually raised them further — from 10 percent to 15 percent.

For Indian markets, however, the outlook remains uncertain. With Trump's revised tariff regime now taking shape, volatility is expected to persist as traders and investors weigh the implications for trade flows, corporate earnings, and global risk appetite.

Bearish undertone continues

Nifty continued to reflect underlying weakness this week, closing at 25,571 — a modest gain of just 0.39% that does little to alter the broader bearish picture. The RMI remains entrenched below the zero line, reinforcing the negative bias that has characterised recent price action.

Adding to the concern, a bearish crossover has emerged on the daily timeframe, lending further weight to the downside signals already in play. The 20-day moving average continues to act as a formidable resistance zone, and with prices facing repeated rejections at higher levels, the bulls have struggled to make any meaningful headway.

Taken together, these technical signals point toward continued selling pressure in the week ahead, with another negative reaction appearing likely unless market conditions shift meaningfully in favour of the buyers.

Source: web.strike.money

FIIs continue to maintain a decisively negative stance in the derivatives market, with their net index futures position standing at -1,33,664. This level of sustained short positioning underscores the bearish sentiment that FIIs have held in recent weeks.

From a technical standpoint, the indicator has now returned to a resistance area that has proven significant on multiple occasions in the past — a zone where short-term corrections have consistently followed. With the indicator once again testing this familiar ceiling, history suggests that a pullback or even a broader reversal could be on the cards from current levels.

Source: web.strike.money

The Daily Average Swing Indicator, a mid-term measure of market momentum, currently stands at 43.86. Notably, the indicator had moved into overbought territory just a few days ago before turning lower from that level — a behavioural pattern that has historically preceded corrections in the index.

While no signal is definitive in isolation, the precedent set by similar readings in the past suggests that some degree of short-term weakness may be on the horizon. That said, the situation warrants close monitoring, and further price action will be key to confirming whether a meaningful correction is indeed underway.

Source: web.strike.money

One of the key diffusion indicators — specifically, the percentage of stocks carrying an RMI buy signal — has climbed into extreme overbought territory and is now beginning to turn lower from those elevated levels. This is a pattern that has not gone unnoticed historically; on previous occasions when the indicator behaved in a similar fashion, the broader market followed with a period of correction or weakness.

Given the striking resemblance to those past episodes, there is a reasonable case to be made that a similar scenario may be unfolding at present, adding yet another layer of caution to the near-term market outlook.

Source: web.strike.money

The put-call ratio open interest, measured on a nine-day moving average, currently stands at 0.83. What makes this reading particularly noteworthy is the emergence of a bearish hidden divergence — a subtle but telling disconnect between the indicator and the index. While the put-call ratio has been registering higher highs, the index itself has been carving out lower highs, and it is precisely this divergence that raises a flag.

Such a pattern is rarely coincidental. When the indicator and the index move in opposing directions in this manner, it has historically served as a warning sign that the index may be setting up for lower levels in the period ahead.

Sector Rotation

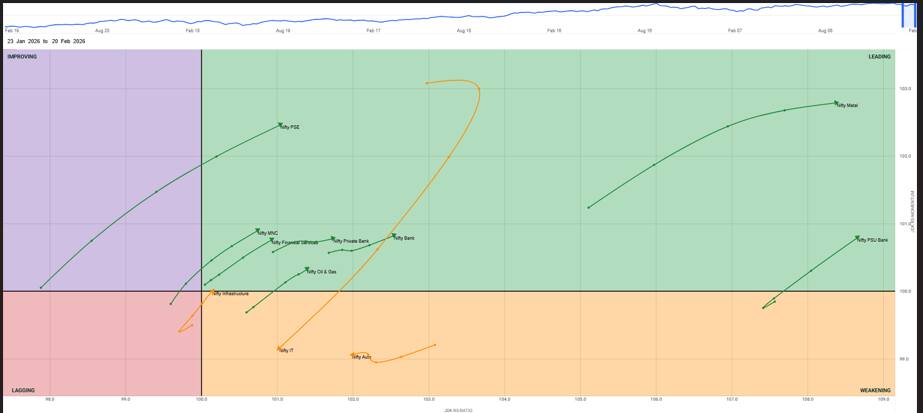

Nifty 50 – The Benchmark Index ended lower, by 0.39% this week and closed at 25,571.25.

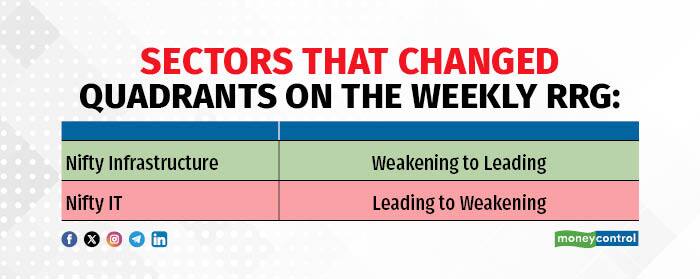

Leading Quadrant: For this week, Nifty Infrastructure has moved from the weakening quadrant into the leading quadrant along with an improvement in momentum. Other sectors such as Nifty PSU Bank, Metals, Nifty Bank, Nifty Oil & Gas, Nifty Private Bank, Nifty Financial Services, Nifty MNC, and PSE also remain firmly positioned in the leading quadrant, with momentum improving compared to the previous week. Notably, Nifty PSU Bank has shown a stronger acceleration in momentum, while Nifty MNC and Nifty Financial Services have also recorded a clear pickup in relative strength. Overall, the relative rotation continues to favour PSU Banks, Financials, and MNC as the key outperforming sectors for the week.

Weakening Quadrant: In the weakening quadrant this week, Nifty IT continues to lose momentum, showing a further decline, while Nifty Auto appears to be moving sideways, lacking clear directional momentum. Both sectors remain under watch for potential further deterioration.

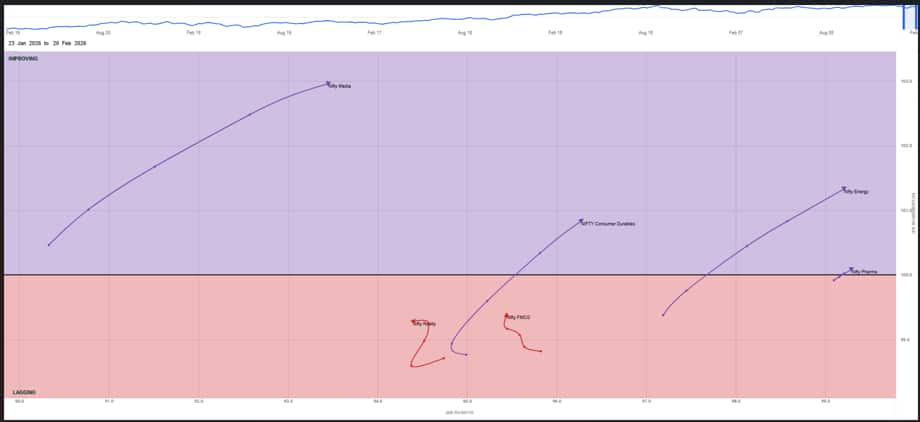

Improving Quadrant: In the improving quadrant, Nifty FMCG has seen a strong increase in momentum, indicating improvement, while Nifty Realty is also gaining momentum but remains relatively weaker compared to other indices.

Lagging Quadrant: In the lagging quadrant, Nifty Media stands out with a strong increase in momentum, followed by Nifty Consumer Durables, Nifty Energy, and Nifty Pharma, all showing rising momentum, though still trailing behind leading sectors.

Stocks to watch

Among the stocks expected to perform better during the week are NTPC, LT, ABSLAMC, Voltas, Power India, KEI, Indian Bank, JB Chemicals, SBI, MFSL, AU Bank, Union Bank, and Polycab.

Cheers,

Shishir Asthana

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.