Dear Reader,

Indian markets rang in 2026 with remarkable strength, as the Nifty50 scaled a fresh all-time intraday peak of 26,340 during Friday's trading session on January 2. The rally marked the second consecutive week of gains, fuelled by robust automobile sales figures and growing optimism around the earnings outlook. Investors appeared undeterred by lingering geopolitical tensions and continued foreign institutional investor (FII) selling.

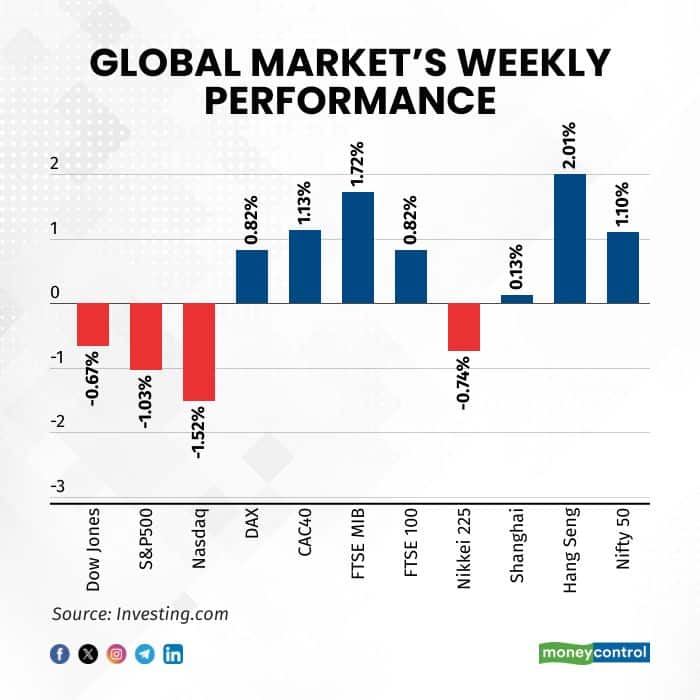

The week's performance revealed a notable divergence across market segments. While the Nifty50 advanced 1.09 percent and large-cap stocks climbed 1.3 percent, mid-cap stocks emerged as the strongest performers with a 1.7 percent gain. Small-cap stocks rose a modest 1 percent during the period.

Despite turning net buyers on Friday, foreign institutional investors remained net sellers for the week, offloading equities worth Rs 13,180.09 crore in the opening week of 2026. Meanwhile, the Indian rupee continued its downward trajectory against the US dollar, settling at 90.19 on January 2—a decline of 34 paise from its December 26 close of 89.85.

Across the Pacific, US markets weakened during the holiday-shortened trading week, though most major indices had concluded 2025 on Wednesday with double-digit gains for the third consecutive year. Trading volumes remained subdued throughout the abbreviated week.

Looking ahead, the coming week is expected to bring heightened volatility following a dramatic US military action in Venezuela that resulted in the arrest of President Nicolás Maduro and his wife. Energy and financial markets may experience an initial shock at the start of the week. However, if no coordinated response materializes from other nations, markets are likely to stabilize relatively quickly, allowing corporate earnings and other fundamental factors to resume their influence on market direction.

Room for upside

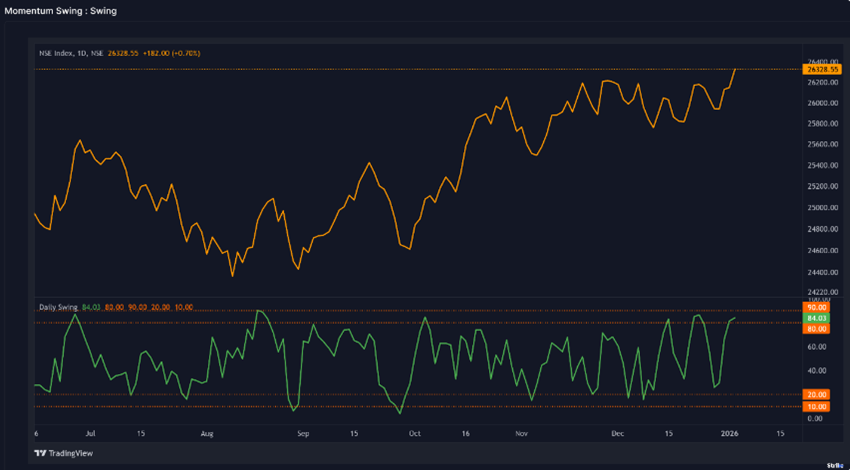

The Nifty defied weakening momentum signals from weekly indicators to notch a fresh all-time high—a testament to the market's resilience and the power of prevailing sentiment. For months, sentiment indicators have consistently pointed toward further upside rather than a downturn, and the market has validated that view time and again.

Bank Nifty delivered an even more impressive performance, avoiding the whipsaws that plagued weekly indicators despite prolonged sideways consolidation. It too closed at a record high, reinforcing the strength of the financial sector. The breadth of the rally is particularly encouraging: the Nifty Midcap 100 has also reclaimed its all-time high, suggesting this move is well distributed across market segments rather than concentrated in a handful of stocks.

However, one short-term concern looms. The daily swing indicator sits at 84, a level that has historically preceded selloffs lasting several days. Each recent approach to this threshold has triggered a pullback, and there's little reason to believe this time will be different—though one can always hope. Unfortunately, that hope hasn't been rewarded in the past.

In a genuinely bullish trend, markets shouldn't experience such pronounced corrections. Whether this pattern repeats itself remains to be seen, but it's worth watching closely in the sessions ahead.

Source: web.strike.money

Market breadth is showing clear improvement as the 20-day moving average (20dma) has rebounded above the red line and exited the oversold zone. This suggests further improvement is possible, and until a breadth spike occurs, there is room for markets to trend higher.

Source: web.strike.money

FIIs continue to hold net short positions, consistently adding to their shorts on every market dip. The key question now is whether they will finally cover these positions as the market approaches all-time highs.

Source: web.strike.money

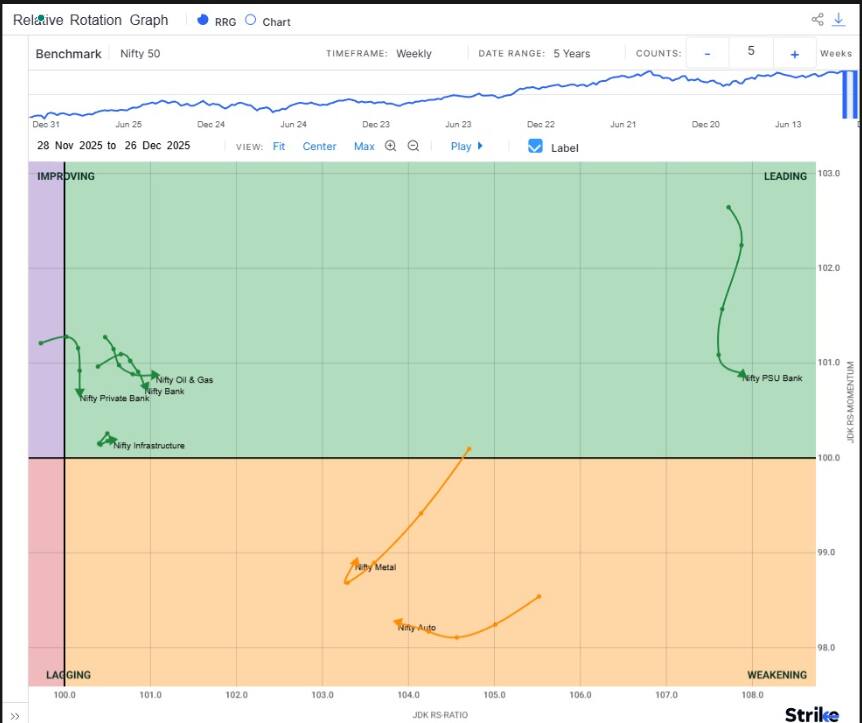

Nifty 50 – The Benchmark Index ended lower by +1.10% this week and closed at 26328.55.

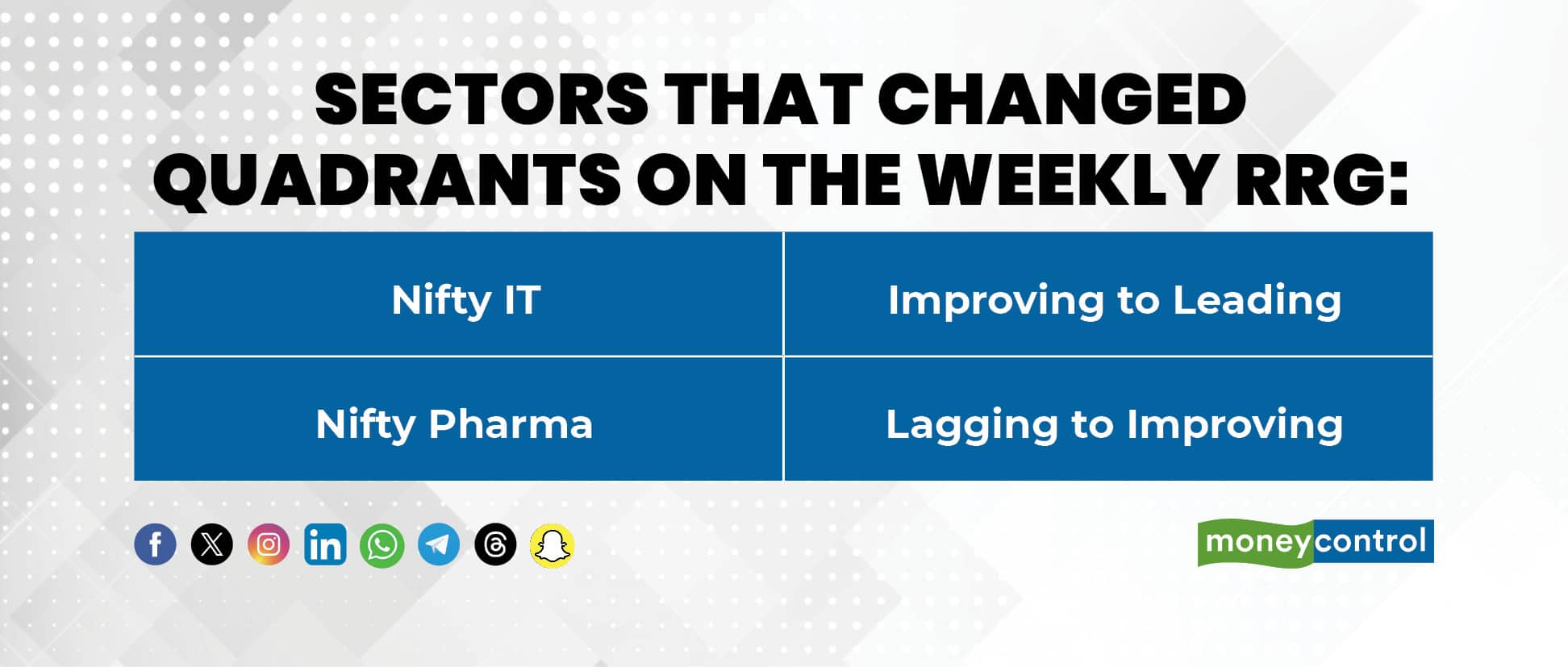

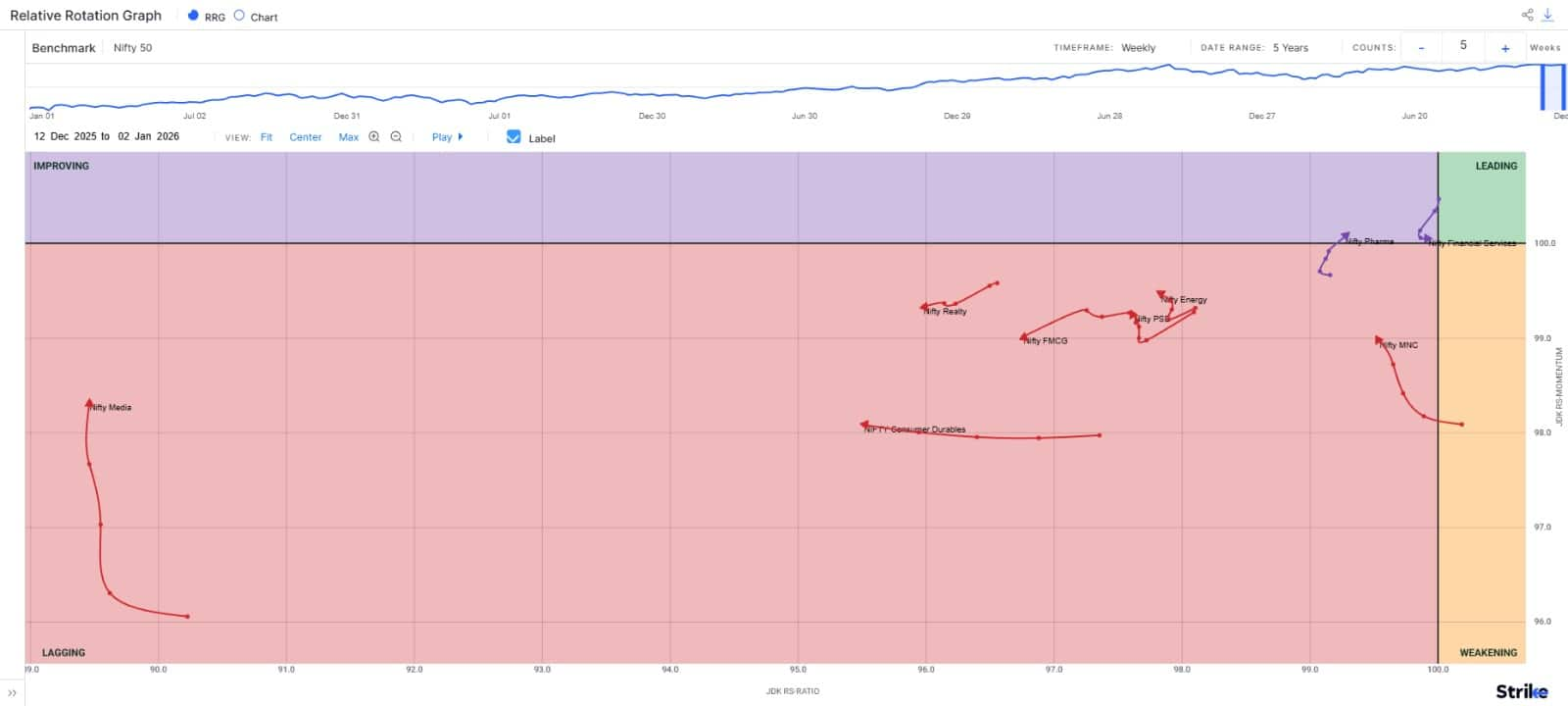

Weekly RRG:

Leading Quadrant:

Nifty IT has entered the leading quadrant this week and has seen a strong uptick in both momentum and relative strength. Nifty Private Bank continues to see a decline in momentum, but the relative strength has improved this week. Nifty Oil & Gas has seen a sharp decline in momentum this week. Nifty Infra and Nifty PSU have seen a sharp decline in momentum and relative strength this week, which is not a good sign.

Weakening Quadrant:

Nifty Metal and Nifty Auto have seen a significant uptick in momentum in the past few weeks, but a pick-up in relative strength is still awaited.

Improving Quadrant: Nifty Financial Services index’s momentum decline has been arrested, and it has seen an uptick in relative strength. Nifty Pharma has entered the improving quadrant this week. This index is gaining momentum and relative strength.

Lagging Quadrant:

The Nifty FMCG index has seen a sharp deterioration in momentum and relative strength. Nifty MNC, Nifty PSE, Nifty Energy, and Nifty Media are seeing improving momentum over the last few weeks. Improvement in relative strength is awaited. The Nifty Consumer Durable index continues to show deteriorating relative strength, but it has seen some improvement in momentum this week. Nifty Realty has seen a dip in both momentum and relative strength this week.

Stocks to watch

Among the stocks expected to perform better during the week are Tata Consumer, Eicher Motors, Marico, Titan, Nestle, AU Bank, Torrent Pharma, Maruti, Manappuram, HDFC Bank, IDFC First, Phoenix and Federal Bank.

Cheers,

Shishir Asthana

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.