Dear Reader,

The truncated trading week saw Indian equity markets navigate in a narrow band, ultimately ending unchanged. The convergence of early corporate earnings announcements, persistent apprehensions surrounding trade tariffs, and unrelenting selling pressure from Foreign Institutional Investors collectively weighed on market sentiment.

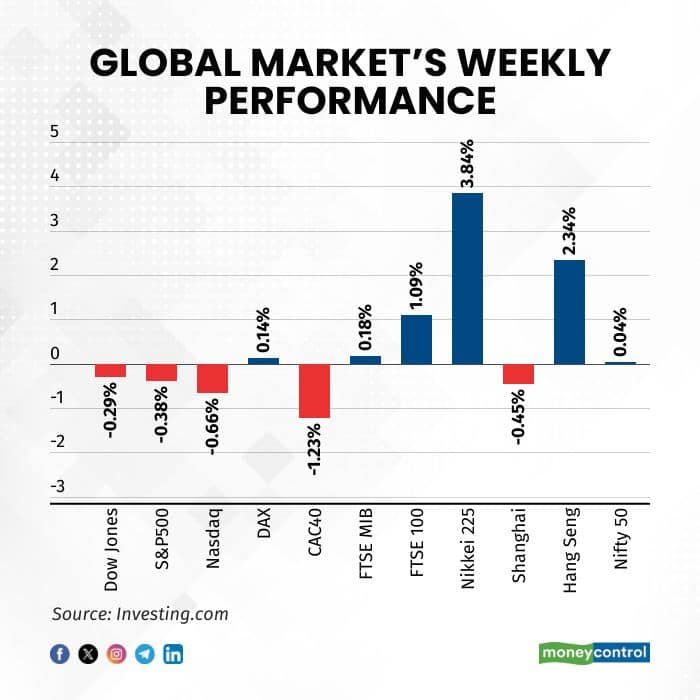

The Nifty50 managed a modest advance of 0.04 percent by week's end, while broader market indices slipped marginally into negative territory. Beneath this calm surface, however, significant sectoral rotation was underway.

Consumer Durables, Realty, Pharmaceutical, and Healthcare stocks each declined approximately 2 percent, with the Auto index retreating 1.75 percent and Media stocks falling 1 percent. Conversely, PSU Banking and Metal stocks surged 4.5 percent each, while the Nifty IT index climbed 2.8 percent.

FIIs maintained their withdrawal from Indian equities, offloading shares worth Rs 14,265.58 crore during the week.

Across the Atlantic, US indices finished mixed, with small-cap stocks notably outperforming benchmark indices. The earnings season commenced with major banks reporting fourth-quarter results, prompting varied market responses.

Looking forward, markets are likely to contend with the ripple effects of the US President's decision to impose a 10 percent tariff on the European Union following disagreements over Greenland—a development expected to reverberate across global markets. Domestically, benchmark indices may experience heightened volatility as several Nifty heavyweights released earnings over the weekend, with additional results scheduled for announcement in the coming days.

Bears in control

The Nifty index continues to consolidate beneath its support line, signalling that bearish forces remain in command. In the near term, the recent low of 23,473 represents a critical support level, while 26,030—the 61.8 percent retracement of the latest decline—stands as a significant resistance threshold. A decisive break beyond this range could trigger a short-term directional move; absent such a breakout, the Nifty is likely to trade sideways or continue its downward trajectory.

The market-wide Open Interest Put-Call Ratio (OI PCR) is approaching the lower boundary of its typical range at 0.72. Historically, the OI PCR has fallen as low as 0.66, suggesting room for further short-term correction in the broader indices. For a genuine reversal in the Nifty index, a turnaround in the OI PCR must materialise first. A decisive close above 26,030 would confirm a price action reversal.

Nevertheless, the short-term outlook for the Nifty remains bearish, as the OI PCR continues its decline and the index trades below its support trendline.

Source: web.strike.money

The percentage of Nifty constituents trading above their 20-day Simple Moving Average showed marginal improvement this week, though the indicator remains positioned in the middle of its historical range. With the Nifty index having breached its trendline support, the short-term trend has turned decisively downward. For a meaningful bottom to establish itself, this breadth indicator would need to decline below the 20 level—a threshold it has yet to reach.

Under current conditions, the market favours a sell-on-rise strategy until the Nifty index closes above 26,030, which represents 61.8 percent of the recent decline. Until such a reversal materializes, traders should approach rallies with caution.

Source: web.strike.money

FIIs currently hold a net short position of 1,90,375 contracts in index futures. This represents a slight reduction from the record high of 1,99,134 contracts—adjusted for the recent lot size change—reached earlier this week. The percentage of long positions in index futures remains in single digits, reflecting exceptionally bearish sentiment among FIIs.

Historically, such extreme positioning has often preceded double-digit returns over the subsequent three to four months once a market bottom forms. However, as previously noted, two key short-term indicators—the market-wide OI PCR and the percentage of stocks trading above their 20-day SMA—continue to suggest that further downside remains likely in the near term before any sustainable recovery can take hold.

Source: web.strike.money

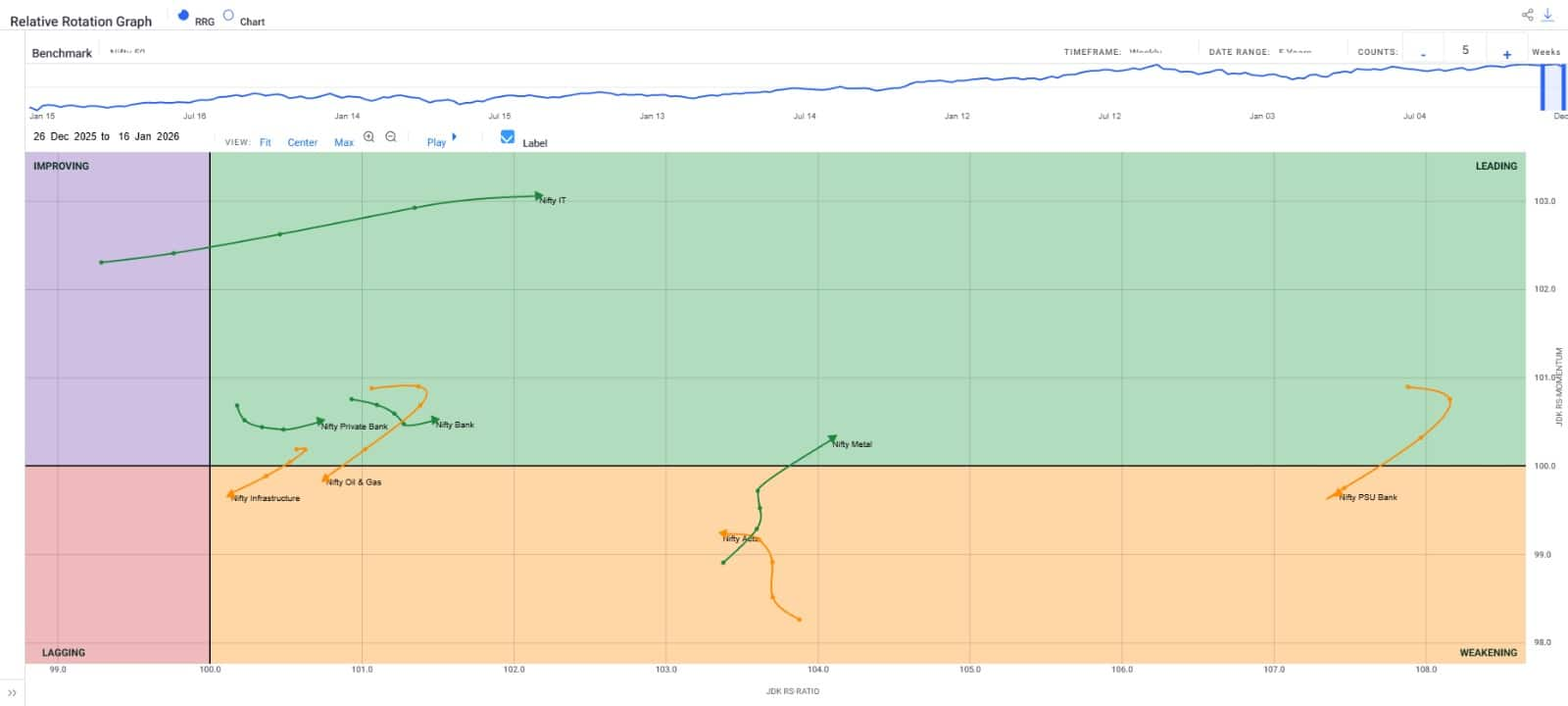

Sector Rotation

Nifty 50 – The Benchmark Index ended flat, up by +0.04% this week and closed at 25694.35.

Leading Quadrant:

The Nifty IT index continues to gain momentum and relative strength, with strong outperformance this week. Nifty Bank and Nifty Private Bank saw a turnaround in momentum this week, with sharp improvements in relative strength. Nifty Metal saw significant momentum and relative strength improvements, pushing this index into the leading quadrant this week.

Weakening Quadrant:

Nifty Oil and Gas has entered the weakening quadrant this week, as it continues to lose momentum and relative strength. The Nifty Infrastructure index also continues to lose momentum and relative strength after entering the weakening quadrant last week. Nifty Auto has seen a meaningful decline in relative strength this week. If this trend continues, the index is expected to underperform in the coming weeks. Nifty PSU Bank has shown initial signs of a turnaround in momentum and relative strength this week, but we need to see further evidence.

Improving Quadrant: The Nifty Financial Services index is back in the improving quadrant and has seen improvements in both momentum and relative strength. If this trend continues, it can enter the leading quadrant in the coming weeks and outperform the benchmark index.

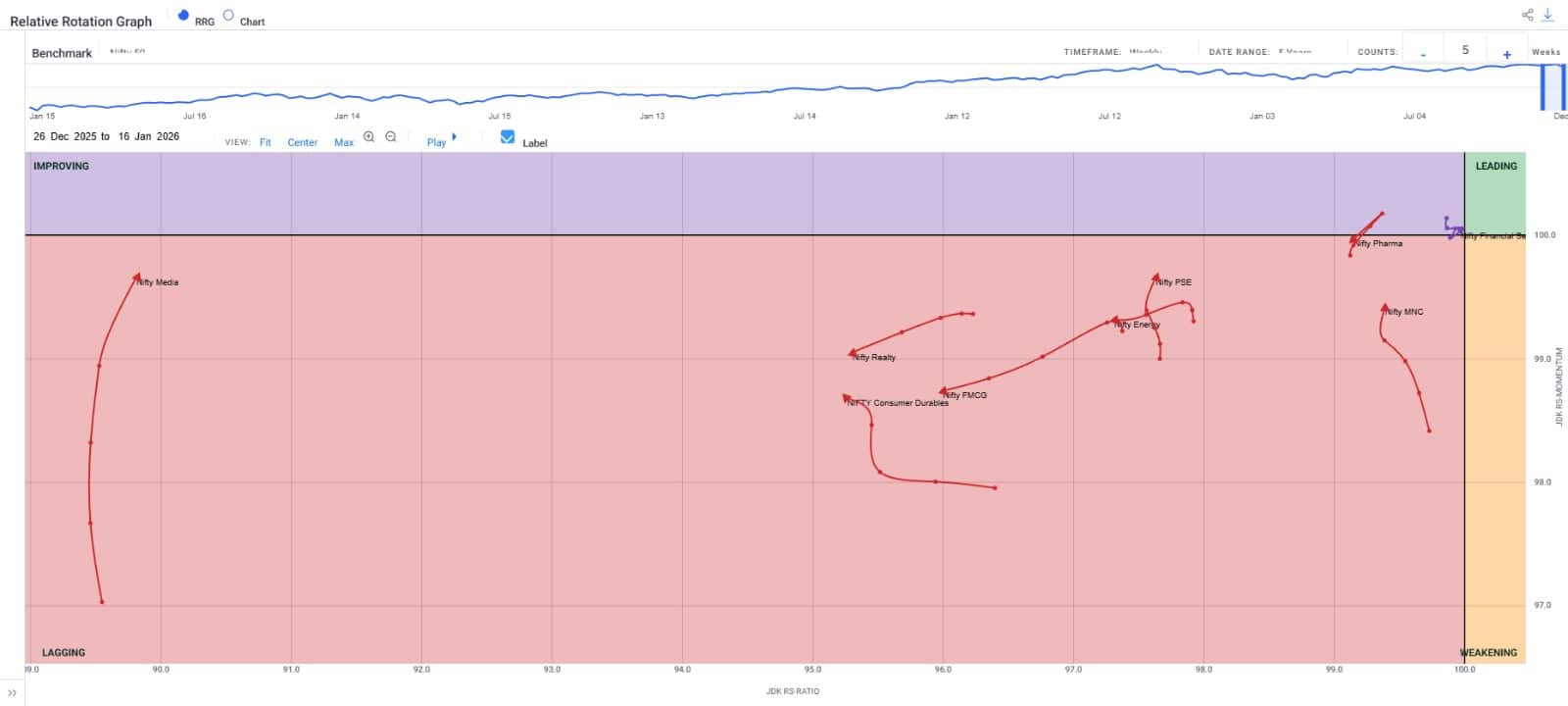

Lagging Quadrant:

Nifty Pharma saw a significant turnaround in momentum and relative strength, pushing it back into the lagging quadrant from the improving quadrant. Nifty MNC continues to gain momentum, but relative strength has not improved yet. If relative strength improves, the Nifty MNC could be an interesting sector to watch in the near term. Nifty PSE and Nifty Media continue to gain momentum, and both indices have seen a minor improvement in relative strength this week, making them interesting sectors to watch. Nifty Energy, Nifty Realty, and Nifty FMCG continue to deteriorate in both momentum and relative strength. Nifty Consumer Durable was showing signs of a comeback, but that did not last long, as relative strength has weakened once again this week.

Stocks to watch

Among the stocks expected to perform better during the week are Federal Bank, AU Small Finance Bank, LTI Mindtree, Bank of India, PNB, MCX, Vedanta, Nestle, and Alchem Labs.

Cheers,

Shishir Asthana

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.