Dear Reader,

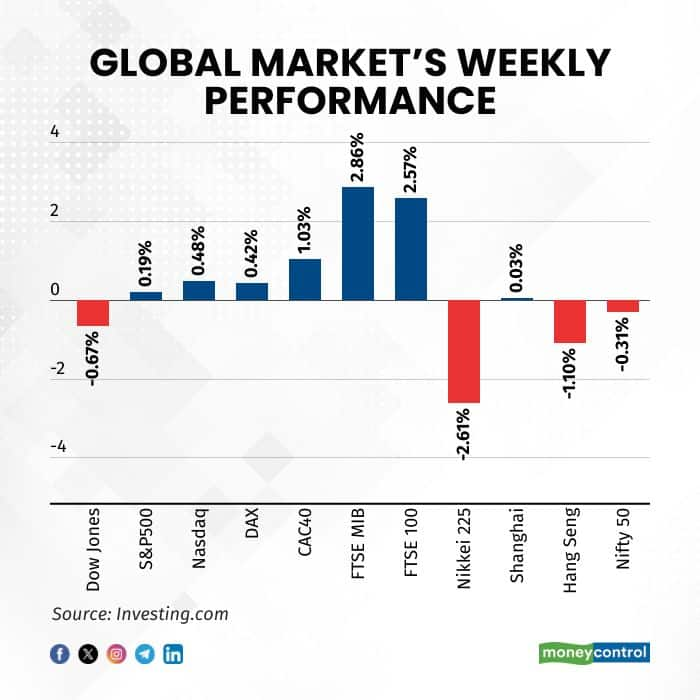

The Indian equity market concluded a turbulent week on a relatively flat note, with the benchmark Nifty 50 index slipping 0.31 percent. The modest decline came against a backdrop of lower than usual FII selling that has persisted since late September.

The week's standout performers were information technology stocks, which staged an impressive recovery by surging 3.47 percent, extending their upward momentum. The only other noticeable gainer was the automobile sector which closed the week 0.59 percent higher.

However, most sectors closed in the negative, including defensive sectors like FMCG that lost 0.71 percent and pharmaceutical stocks dropped by 0.22 percent. The energy sector fell by 1.62 percent, and real estate by 1.11 percent.

The US markets also experienced subdued trading activity as the year-end holiday season approached. A positive development for US equities was a pause in selling pressure seen in artificial intelligence stocks, which had been facing increased scrutiny over elevated valuations.

However, concerns emerged from the labour market, where the unemployment rate held steady at 4.6 percent in November 2025, the highest in four years.

Looking ahead, market participants anticipate a period of directionless trading, primarily due to reduced activity in global markets during the holiday season. Trading volumes typically thin out during this period, leading to increased volatility and less reliable price signals. However, there remains a glimmer of optimism based on historical precedent—the final weeks of the calendar year have traditionally been positive for Indian markets, a pattern investors hope will repeat itself in the current year.

Awaiting clear signals

The Nifty index registered its third consecutive week of losses, yet the underlying momentum trend remained intact according to the Rohit Momentum Indicator (RMI). This development offers an encouraging signal, particularly as the index has reached the lower end of its daily trading range and bounced from that support level. More significantly, the midcap and smallcap indices closed the week in positive territory, kindling hopes that the prolonged selling pressure in the broader market may finally be subsiding. While these are early days, one more positive week could confirm a potential reversal.

The breadth indicators beneath the surface tell an equally promising story. The percentage of small-cap stocks trading above their 20-day moving average had plummeted to just 10 percent. However, during the past two days—even as markets declined—this reading never fell below 26 percent. By week's end, it had improved. This divergence suggests that while headline indices may have weakened, the underlying market breadth has been quietly strengthening—a technical development that often precedes broader market recoveries.

Source: web.strike.money

The 20-day advance-decline ratio has declined to oversold levels when measured against historical benchmarks. However, the ratio is now showing signs of improvement, rising steadily and poised to break out above the oversold range marked by the red dotted threshold.

Source: web.strike.money

The daily swing indicator proves most valuable when it reaches extreme readings, though such conditions don't always materialize. Several days ago, at the market's peak, the indicator registered a reading above 80, signalling overbought conditions. Under normal circumstances, if the market had subsequently fallen to new lows, one would expect the indicator to reach oversold territory. However, this hasn't yet occurred. The absence of either extreme leaves us without a clear directional signal from this particular technical measure, suggesting that further price action is needed before the indicator can provide meaningful guidance.

Source: web.strike.money

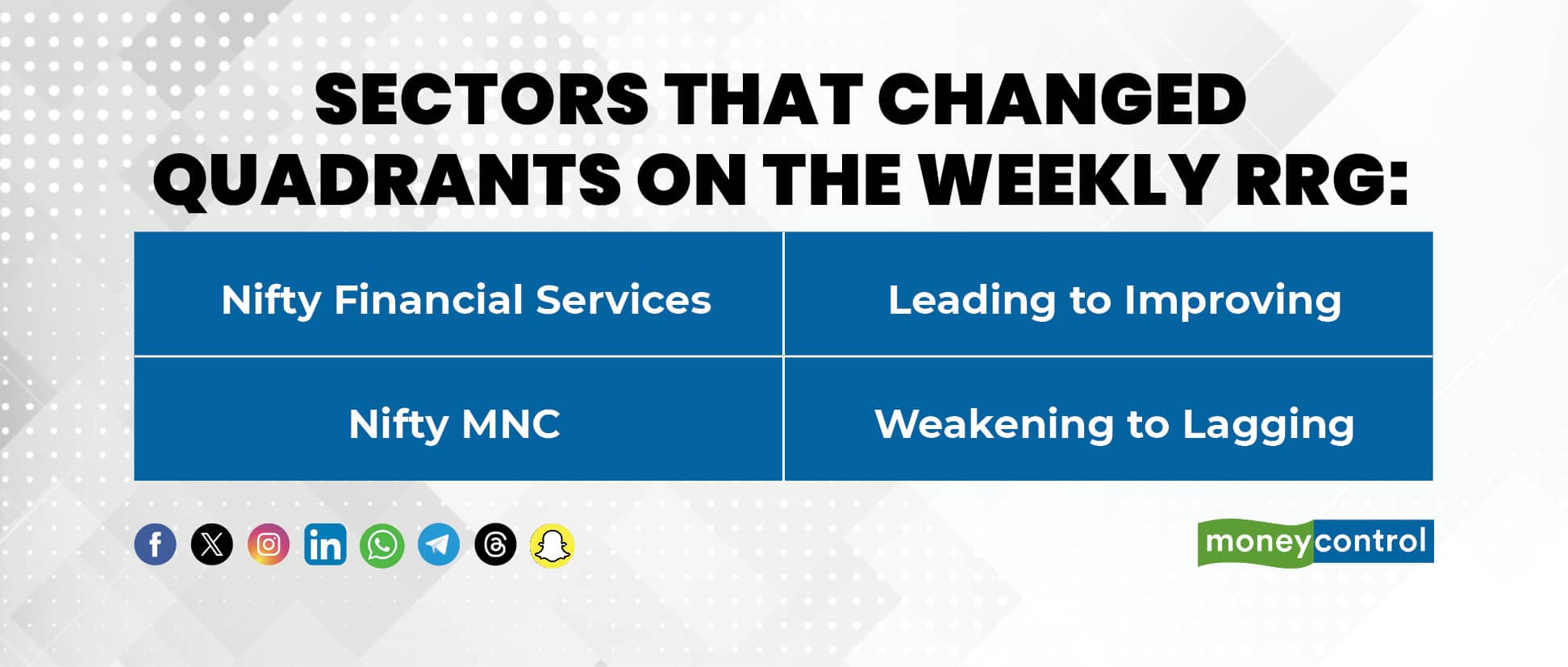

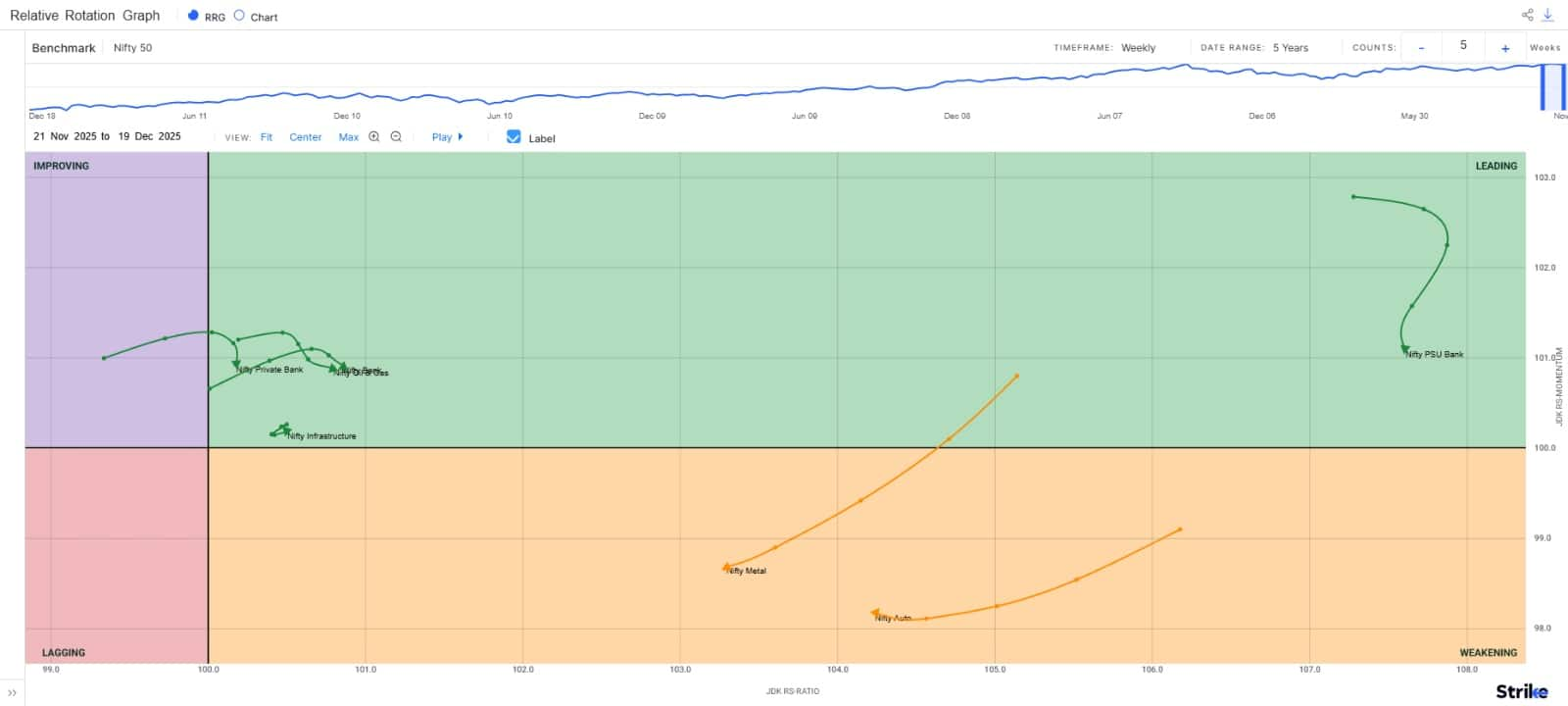

Sector Rotation

Nifty 50 – The Benchmark Index ended lower by -0.31% this week and closed at 25966.40.

Weekly RRG:

Nifty Private Bank and Nifty Financial Services have seen some improvement in relative terms, but the momentum has fallen for all indices. Nifty PSU Bank continues to see a dip in momentum as well as relative strength. Nifty Infrastructure has seen an improvement in both momentum and relative strength this week.

Weakening Quadrant:

Nifty Metal continues to experience a decline in momentum and relative strength. Nifty Auto has seen some improvement in momentum this week, but the relative strength continues to weaken.

Improving Quadrant:

Nifty IT has seen a sharp improvement in momentum and relative strength for the third consecutive week. Nifty Financial Services is back in the improving quadrant from the leading quadrant due to the decline in momentum as well as relative strength.

Lagging Quadrant:

Nifty Realty, Nifty Energy, Nifty PSE, Nifty, and Nifty Consumer Durable continue to see deteriorating momentum as well as relative strength. Nifty Media and Nifty FMCG have experienced some turnaround in momentum this week, and both these indices saw an improvement in momentum. However, the relative strength continues to weaken for both these indices. The Nifty Pharma index also saw some improvement in momentum, but the relative strength continues to decline.

Stocks to watch

Among the stocks expected to perform better during the week are Shriram Finance, PNB Housing, Laurus Labs, Reliance, MCX, Indus Towers, Federal Bank, ICICI Prudential, and Titan.

Cheers,

Shishir Asthana

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.