Indian equities are set to face a cautious start in March despite a strong historical trend of gains in the month, as rising geopolitical tensions following US and Israel strikes on Iran weigh on sentiment. A continued rally in Asian markets such as Korea and Taiwan, along with increasing investor preference for safe-haven assets like gold and silver, is also raising concerns about a potential diversion of investment flows away from India.

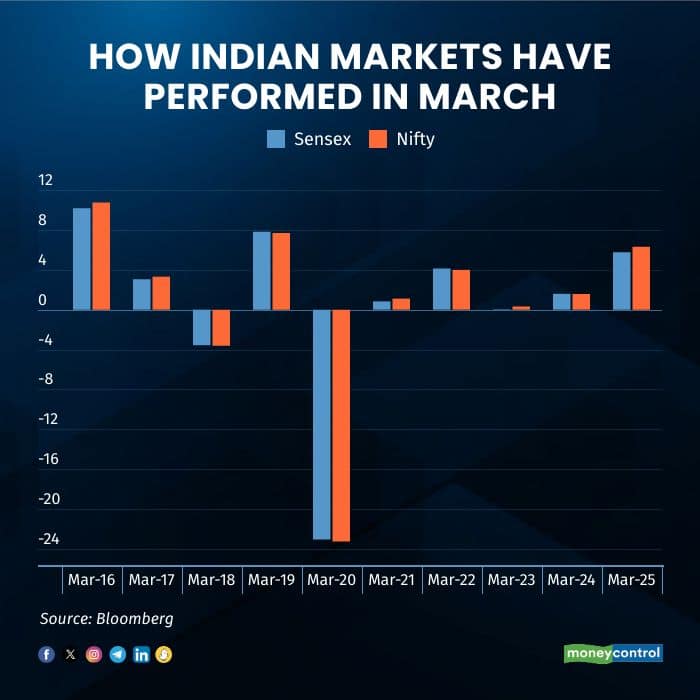

Sensex and Nifty have posted gains in March in eight of the past ten years. In March 2025, both indices advanced about 6 percent, while March 2024 saw gains of 1.6 percent each. March 2023 recorded marginal increases, and in March 2022, both benchmarks rose over 4 percent.

This year for March, however, the backdrop appears more challenging. The US and Israel have struck targets across Iran, escalating tensions in the oil-rich Middle East. Iran responded with missile strikes on Israel and US bases in the region, while several Persian Gulf nations shut their airspace. Although the prospect of a full-scale war remains uncertain, persistent tensions have already begun influencing energy markets. Brent crude rose as much as 13 percent to $82 per barrel, the highest in four years, and is up nearly 30 percent so far this year amid US-Iran tensions.

For India, a major crude importer, higher oil prices could increase inflationary pressures and widen both the current account and fiscal deficits.

Beyond geopolitical risks, strong gains in Asian markets are drawing investor attention. Analysts note the rally has shifted from being valuation-driven to earnings-driven. So far in 2026, Taiwan and Korea markets have gained 24 percent and 51 percent respectively, while Japan has risen 19 percent. The Shanghai Composite is up 12 percent and Philippines markets have gained 14 percent.

Korea’s forward PE has declined to 10.4x from 12.8x in late October even as the market rose 39 percent, while Taiwan’s PE moved from 19.1x to 18.7x alongside a 19 percent market gain, reflecting earnings-led strength. India, in contrast, has not seen earnings estimate upgrades.

Foreign investors returned to Indian equities in February, buying stocks worth $2.5 billion following improved sentiment from rapid trade deals with the EU and the US. However, declining consensus EPS estimates suggest it may be too early to call a sustained reversal.

Domestic flows have also weakened, with mutual funds turning net sellers in February for the first time in three years, offloading over Rs 4000 crore. Investors have continued to trim exposure to Indian IT stocks amid AI-related concerns. At the same time, demand for defensive assets has strengthened. Gold and silver rose 8 percent and 10 percent respectively in February and are up 22 percent and 31 percent so far this year.

Reflecting these pressures, Indian markets saw a sharp sell-off on Friday, with the Sensex falling 961 points and the Nifty slipping below 25,200. The focus has now shifted to whether the market can hold key support levels amid global volatility.

Akshay Chinchalkar, Managing Partner and Head of Markets Strategy at The Wealth Company, said the situation could trigger a risk-off phase if tensions persist. He noted that the Nifty closed below its 200-day average, bringing the 24,600 support zone into focus. A breach of this level, in the absence of swift de-escalation, could put the medium-term uptrend at risk, while a weekly close above 25,700 would be required to stabilise sentiment.

Chinchalkar added historically speaking, drops of 2-3% in the first few sessions have been followed by quick recoveries, but with Iran striking US bases in other parts of the Middle East, this time could be different. "We have to remember that India is an emerging market that imports a significant percentage of its annual oil demand, so unless OPEC+ surprises with an out-of-the-box production hike to cap oil prices, we should expect the rupee, bond yields and stocks to be hit, at least initially", he said.

Experts said a short-term correction of around 1-1.5 percent is possible, with automobiles, financials and FMCG likely to face pressure. IT and export-oriented sectors may find relative support amid global risk aversion and a stronger dollar. Energy-intensive industries such as aviation, logistics, paints and chemicals could see margin pressure from higher input costs, while upstream oil producers may benefit from elevated crude prices. Broader market reactions may include short-term corrections, capital outflows and depreciation pressure on the rupee.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.