In the minutes of the last monetary policy committee (MPC) meeting held in June 2022, Ashima Goyal, a member of the panel and the Prime Minister’s Economic Advisory council, and a professor at the Indira Gandhi Institute of Development Research, suggested that the Reserve Bank of India could opt for multi-tier excess reserve system to address the surplus liquidity position in the market. This explainer helps understand the surplus liquidity situation in the markets and whether a multi-tier excess reserve system can help address the problem.

What is liquidity and what is its relationship with central bank policy rates?

The financial markets and especially banks constantly manage their liquidity positions. If the balance sheet is in surplus, it lends liquidity to markets and if in deficit, it leads to borrowing liquidity from markets. Central banks play a crucial and natural role in this liquidity management function of banks. If banks need liquidity, central banks provide it at a set interest rate and if banks have excessive liquidity, the central bank absorbs it at another rate of interest.

These two interest rates in turn become the key monetary policy interest rates of any central bank. For instance, the RBI infuses liquidity at the repo rate and absorbs liquidity at the standing deposit facility (SDF) rate. The SDF rate is lower than repo rate by 25 basis points (bps) and changes automatically with changes in policy repo rate.

Commercial banks maintain two kinds of reserves with the central bank. The first are minimum reserves that are for safety and interbank transfer payments. The second are funds that exceed minimum reserve requirement. These funds either remain on the central bank’s balance sheet as excess reserves or are parked by banks with the central bank’s deposit facility. In the case of the RBI, the cash reserve ratio is the minimum balance.

What is the relationship between inflation, policy rates and liquidity?

If inflation is higher than target and expected to remain higher, central banks increase policy rates. The higher rates will be effective only if liquidity is also tight. If liquidity is tight, financial markets will borrow from the central bank at higher interest rates. This will have a knock-on effect on other rates such as those governing deposits, loans and bonds. The idea is that the higher interest rates will moderate economic activity and lower inflation.

If inflation is trending lower than the target, central banks lower policy rates. The lower rates will be effective only if liquidity is in surplus and financial markets will now deposit liquidity with the central bank. In a reverse of the previous scenario, financial markets and particularly banks will pass on the lower interest rates to other interest rates such as those on deposits, loans and bonds. The lower interest rates will increase economic activity and lead to higher inflation.

What is the status of managing inflation, policy rates and liquidity?

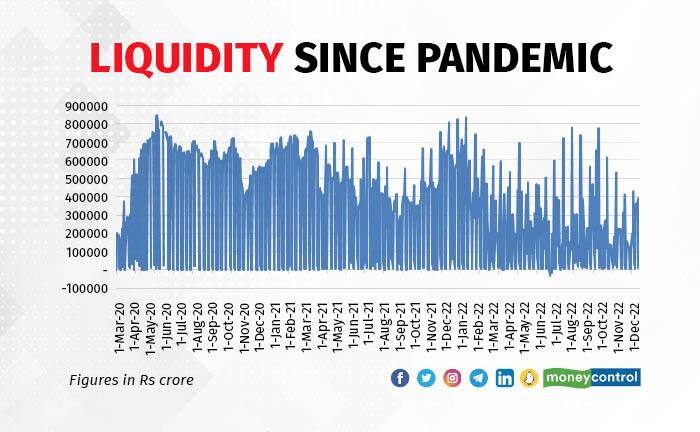

The pandemic led to heightened concerns over growth and financial stability. The RBI not only lowered policy rates but also significantly infused liquidity. The surplus liquidity absorbed by the RBI averaged Rs 3.25 lakh crore from March 2020 to April 2022.

The economic situation changed dramatically in the wake of the Russia-Ukraine war in February 2022. Inflation started to rise dramatically across the world. In May 2022, the RBI increased its policy rate by 40 bps at an off-cycle meet and further by 50 bps in June 2022. The RBI had started withdrawing liquidity even earlier. As explained above, in the case of tighter monetary policy, liquidity should ideally be in deficit mode. Since May 2022, the surplus liquidity has declined and averages Rs 1.76 lakh crore but continues to remain in surplus.

MPC member Goyal raised this very concern in her MPC statement, saying, “Under the external benchmark system, as it works currently, banks may not need to raise deposit rates commensurately until excess liquidity is sufficiently absorbed so that they have to borrow at the repo.” Her reasoning was that under the current surplus liquidity scenario, banks were unlikely to raise deposit rates. If banks do not do so, bank interest rates will not increase and the purpose of the RBI raising policy rates would not be achieved.

How can a multi-tier system address this?

The central banks of developed economies such as Japan, Switzerland and the European Union have opted for a multi-tier system of reserves. The central banks in these economies kept policy rates at zero and deposit rates at negative levels. The negative deposit interest rate implies that banks have to pay an interest for depositing surplus funds with the central bank! The negative interest rates should have provided incentives to banks to lend but the European banks preferred to park their reserves with the European Central Bank and incur higher interest expenditure.

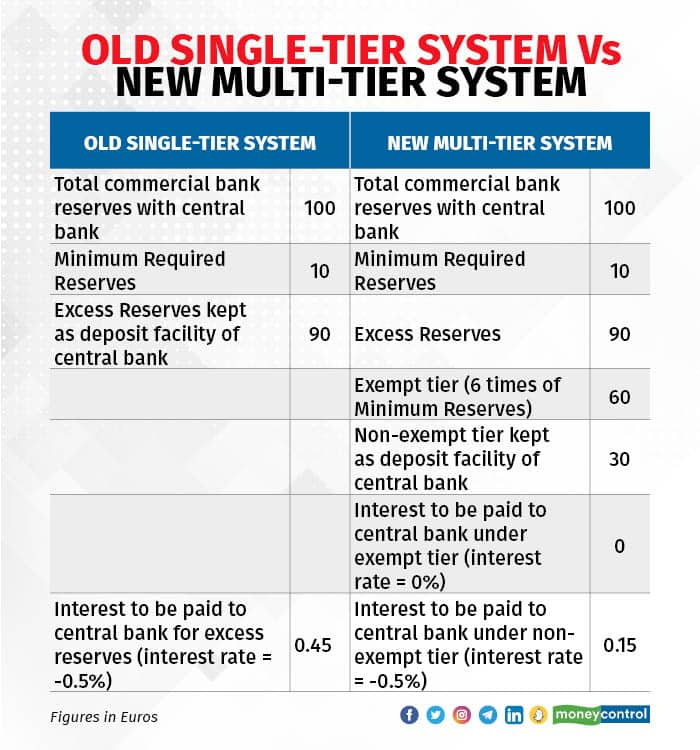

In order to address these multiple issues because of excess reserves, the central banks introduced a multi-tier reserve system (see summary here). The excess reserves were divided into two tiers. The first is the exempt tier which was estimated at six times the minimum reserve requirement for any bank. Excess reserves up to this level will be remunerated at zero percent, implying no cost. Excess reserves beyond this level will continue to be remunerated at the negative deposit facility rate.

We can understand this change via the illustration below. In the old single-tier system, the banks were paying interest rate on the entire excess reserves worth €90. In the new multi-tier system, banks pay interest only in the non-exempt tier of the excess reserve. This lowers the interest rate costs and encourages lending by banks.

The multi-tier system shows mixed results. Early research shows that in Switzerland there were variations in banks’ experience with multi-tier reserve system. In the case of the European Central Bank, lenders continued to maintain large excess liquidity at negative rates. As most of these central banks barring Bank of Japan are now increasing policy rates and withdrawing liquidity, we have to see whether they will continue to have excess liquidity as well.

What does all this mean for the RBI?

Taking a leaf from the above central banks, Goyal suggested, “If excess liquidity persists, yet policy rates rise, the ECB multi-tier excess reserve system is an option. Higher rates paid on a part of reserves held at the central bank could be conditional on banks passing on a share of this to depositors.”

The RBI’s surplus liquidity could also be divided into two tiers: exempt and non-exempt. The exempted tier could be approximated as a percentage of minimum CRR reserves and remunerated at a rate higher than the SDF rate. However, this should be conditional on banks passing the higher interest rates to deposits and eventually leading to higher interest rates on loans too. The non-exempted tier will continue to be remunerated at the SDF rate.

The RBI could opt for this multi-tier system based on its forecast of liquidity conditions. If liquidity remains persistently in surplus mode, then it can experiment with the multi-tier system. If liquidity is expected to be in deficit mode in one or two months, then such a measure will only lead to more confusion in the markets. Liquidity is also spread differently in some banks and banking groups. So it is not an easy policy call.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.