Ultratech Cement is set to present its earnings report for the second fiscal quarter of FY25 on October 21. India's largest cement manufacturer is expected to deliver a subpar performance in Q2FY25 both sequentially and yearly, primarily due to weak prices, and a decline in average realisations which will impact earnings.

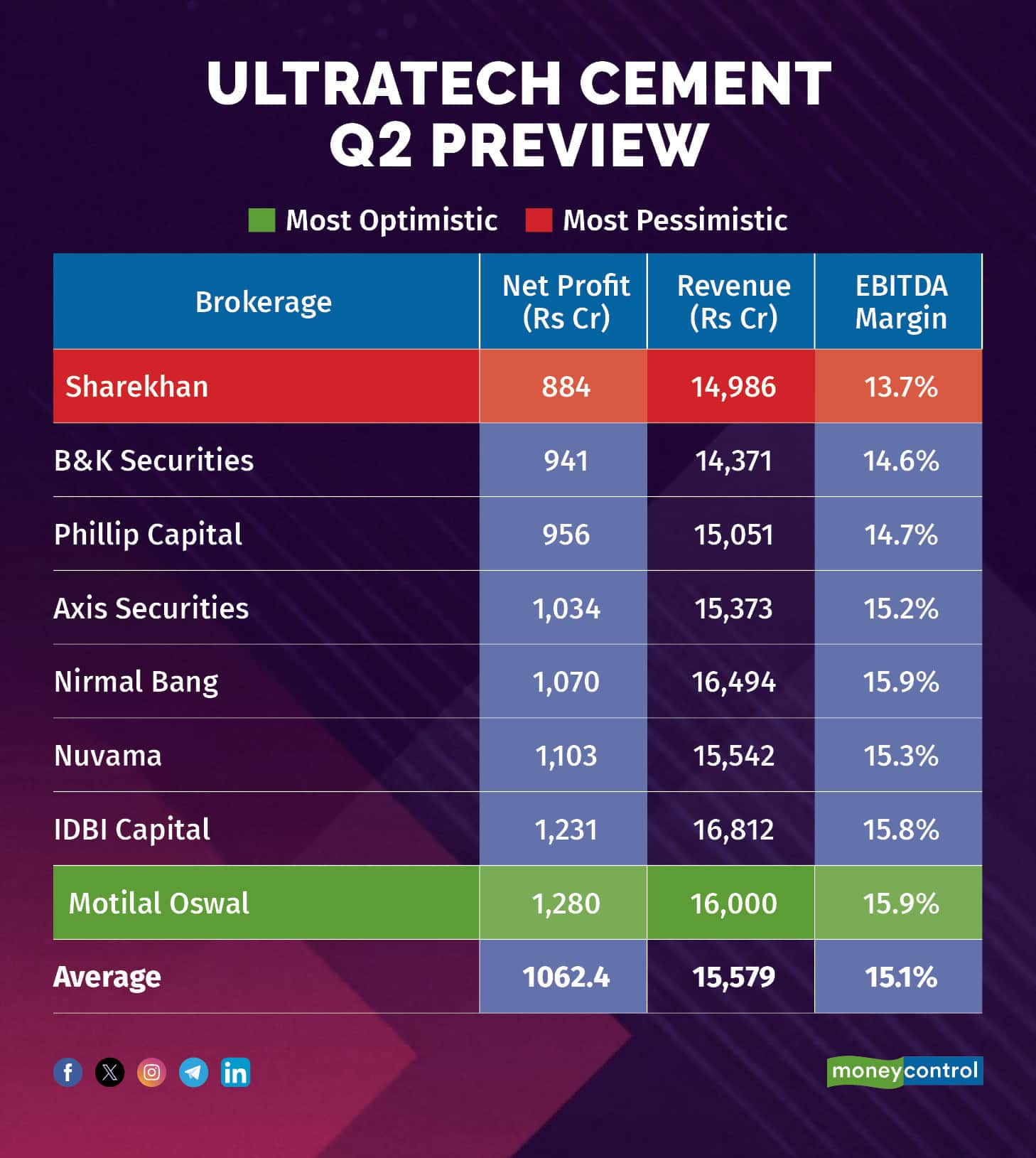

According to a Moneycontrol poll, Ultratech Cement is expected to record a 2.7 percent on-year fall in revenue to Rs 15,579 crore. Net profit is expected to slump 17.06 percent YoY to Rs 1,062 crore. EBITDA Margin is seen falling 500 basis points YoY to 15.1 percent

Even Motilal Oswal's most optimistic estimate sees Ultratech Cement's net profit falling sequentially and year over year. Sharekhan's most pessimistic projection suggests that net profit might sink 40 percent YoY while revenue may slump 6.41 percent.

What factors are driving the earnings?Demand Slowdown: The delayed infrastructure activities following the general election, unavailability of sand, above-average monsoon rains, and flooding in various regions across the country adversely impacted cement sales. Scorching heat, labour shortages in some regions further dented demand during Q2FY25.

Muted prices: Pricing remained under pressure across regions. While multiple attempts were made by cement manufacturers to hike prices during the quarter, monsoon, floods, and lack of infrastructure activities led to hikes being rolled back, keeping cement realizations under pressure.

Decline in realisations: Even volume growth in Q2FY25 is estimated to be lower due to extended monsoon in many parts of the country, putting further pressure on prices which will dent realisations.

Price realisation in cement refers to the average revenue a company earns per unit sold. It helps gauge the average income per ton, with higher realisation indicating better profitability per unit.

High Costs: The cement maker's depreciation/interest expenses are estimated to increase up to 7 percent/5 percent on-year likely causing a negative operating leverage, which occurs when a company's fixed costs are high, causing profits to decline disproportionately as sales decrease.

Combined with lower price realisations, this can significantly hamper net earnings.

What to look out for in the quarterly show?Analysts will be keeping a close eye on management commentary on the demand scenario amidst a weak quarter, price sustainability amidst intensifying competition, and consolidation in the sector.

Timely execution of capacity expansion plans and cost trajectory will also be eyed in Q2 results.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.