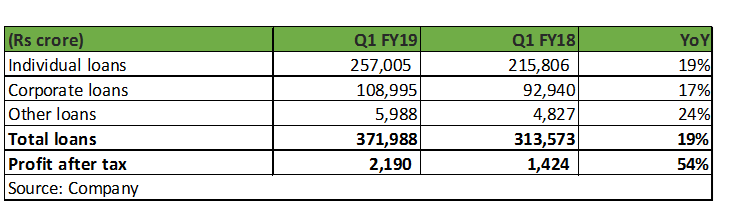

Housing Development Finance Corporation (HDFC), the largest housing finance company, reported net profit growth of 54 percent at Rs 2,190 crore in Q1 FY19 on a low base and aided by strong loan book growth. The latter remains strong and margins stable though transition to Ind-AS led to restatement of certain line items.

The stock has outperformed the Nifty year to date, but there’s more to follow. While the core mortgage business is on a stable growth trajectory, the financial conglomerate stands to gain from equally strong performance of its subsidiaries. Investors cannot ignore this financial powerhouse.

Loan growth and margin are the two key monitorables for HDFC and it didn’t disappoint on either. Despite its large size (high base), HDFC is growing its mortgage book faster than the industry. On the margin front, spreads continue to remain in a narrow range of 2.2-2.35 percent irrespective of the interest rate cycle. While competition has increased manifold in the housing segment, the current interest rate cycle shouldn’t alter the lender’s financials significantly as it continues to have edge on funding vis-à-vis other non-banking financial companies (NBFCs).

Robust loan growth, size not a deterrent Total lending book stood at Rs 371,988 crore as of March-end, up 19 percent year-on-year (YoY). Growth in the total loan book after adding back loans sold in preceding 12 months was 23 percent YoY. Individual loan book grew 19 percent YoY (25 percent after adding loans sold) and now constitutes 72 percent of the total book. Non–individual book increased 17 percent, aided by traction in lease rental discounting and construction finance.

The management is increasingly targeting the economically weaker section (EWS) and lower income group (LIG) segments in affordable housing. The latter constituted 37 percent of approvals (incremental sanctions) in volume terms and 19 percent in value terms during Q1. Average loan size for the EWS and LIG segments stood at Rs 10.1 lakh and Rs 17.6 lakh, respectively, much smaller when compared to the average loan size of Rs 26.7 lakh in the individual segment. Lower ticket sizes in affordable segment means growth will be volume driven and contingent on project launches.

HDFC stands to benefit from structural growth drivers in the sector (GDP growth, under penetration in the mortgage space, etc) as well as government initiatives (interest subvention scheme, tax incentives, Housing for All by 2022, infrastructure status accorded to affordable housing). Despite its size, its loan book growth looks sustainable.

Spreads stable, aided by diverse funding profile Spreads in the overall book remained almost stable at 2.28 percent (individual book: 1.91 percent and non-individual book: 3.14 percent) demonstrating the company’s ability to maintain the same across interest rate cycles, amid rising competition.

HDFC’s resource profile is well diversified. This has enabled it to maintain its competitive cost of funds. Majority of its funding is sourced through debt market borrowings and fixed deposits, constituting 57 percent and 29 percent of total borrowing, respectively, as on March 31.

Apart from aiding low cost of funds, its resource raising capabilities and mix helps in mitigating the inherent tenure mismatch and interest rate risks in the housing finance business (HFC). We are encouraged by the fact that HDFC runs a well matched asset liability maturity (ALM) book with lower gaps in medium term buckets as against peer HFCs.

Impeccable asset quality, excess provisions provide cushion With gross non-performing loans at 1.18 percent, asset quality continues to be pristine. Non-performing loans in the individual portfolio stood at 0.66 percent while that of the non-individual portfolio stood at 2.32 percent as of June- end. The management’s policy of creating 30 percent provisions from one-off gains has resulted in total provisions at 1.27 percent of loan book, which is in excess of the regulatory requirement.

Under Ind-AS, the lender’s assets have been classified based on exposure at default (EAD). As a result, HDFC disclosed standard stressed assets (stage 3 assets) of 2.52 percent. It has adjusted excess provisions outstanding on the balance sheet against the stressed assets, resulting in provision coverage ratio of 28 percent. Since HDFC carries provisions in excess of the regulatory requirement, its net worth has not been impacted by this adjustment. Impact of the transition to Ind-AS on its networth will be reported in the next quarter.

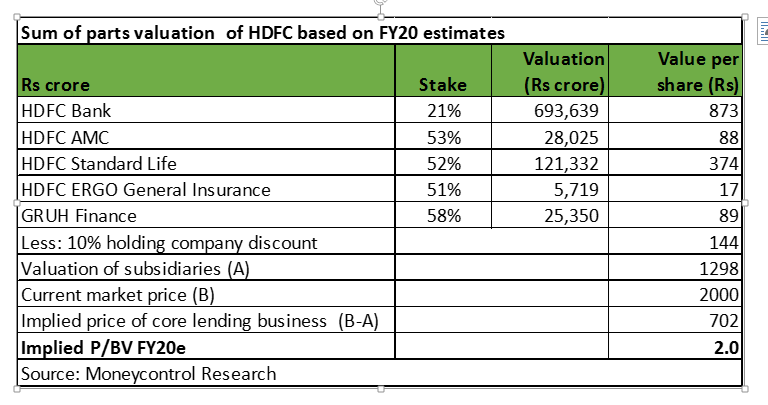

Improving performance of subsidiaries HDFC’s superior performance is just not restricted to its mortgage business. Its subsidiaries (HDFC Bank, GRUH Finance, HDFC Standard Life and HDFC Asset Management Company) have an equally blazing track record. Subsidiaries and associate companies contributed 33 percent of consolidated profit for FY18. With increasing scale and profitability of subsidiaries, more than 50 percent of the value of the company is now derived from subsidiaries.

Well capitalised The company is well capitalised after raising capital worth Rs 13,000 crore and expected warrant conversion. It utilised Rs 8,500 crore from the proceeds to maintain its stake in HDFC Bank (it is raising capital in view of its promising growth outlook) and plans to use rest for inorganic growth. The ongoing initial public offering of HDFC AMC will result in additional capital gains.

Compelling valuations The company should be able to maintain core return on assets (RoA) of 1.8 percent and core return on equity (RoE) of 17 percent aided by strong loan growth, steady margin, stable asset quality and low cost-to-income ratio of around 7-8 percent. With considerable value being created by subsidiaries, at the current market price, the core lending business is getting valued at 2 times FY20 estimated book value, which is at a meaningful discount to its historical average.

We acknowledge that core earnings growth in mid-teens is lower in comparison to many smaller HFCs. However, HDFC’s ability to deliver consistent performance across rate and growth cycles in spite of its large size and high competition commands a high premium to its peers. It is a rarity to find a quality financial services franchise (not just a housing finance play) at a reasonable valuation. Investors should utilise this opportunity to buy into the stock.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!