")

Ruchi Agrawal

Moneycontrol Research

Hindustan Oil Exploration Company (HOEC) reported stellar performance in Q4 on the back of robust volume growth resulting in strong uptick in revenue and profits. With multiple projects reaching the stage of monetisation, firm energy prices and undemanding valuations, the company beckons investor attention.

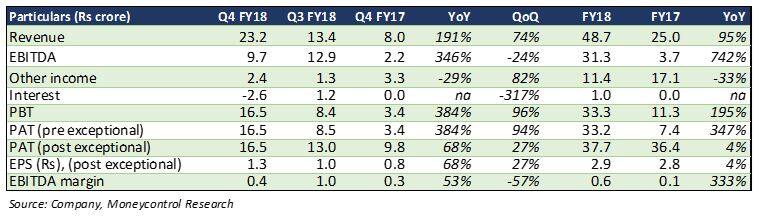

Q4 FY18 performance

Realisations were supported by rising crude and gas prices during Q4. Decline in other income was on account of lower income from mutual funds after liquidation of a portion to fund ongoing expansion at gas field PY1. Operational expenses increased with increased production from the Dirok block. The uptick in the employee expenses comprised a one-time non-recurring charge. Depreciation reduced due to reassessment of reserves.

With the ramping up of production at the Dirok (Assam) field, the company is on the cusp of a turnaround and positioned for a fast paced acceleration. The healthy performance was in line with the management’s guidance and further strengthens our conviction. With major assets in the production phase and strengthening crude prices, HOEC stands in a sweet spot.

Ramp up Dirok contribution

Production from Assam’s Dirok block started in August last year. The block has now started contributing significantly towards revenue and profit. In Q4, it operated on a 4 inch pipeline but from April it shifted to a 12 inch pipeline, which increased production capacity significantly. Its modular gas processing plant was commissioned in March.

The company achieved 30 million standard cubic feet per day (mmscfd) and 700 barrels of oil per day (bopd) in May, close to its target of 36 mmscfd and 1,000 bopd of oil condensate. It saw a strong increase in gas volume during Q4. Given the upward momentum in crude prices, we expect gas prices to follow suit. With a six monthly revision structure for HOEC’s contracts, we see gas realisations improving further.

As per independent assessments, total reserves are expected to be higher-than-expected in this field. The management plans to further drill and monetise the same. It has also expressed interest in acquiring and exploring reserves around the Dirok block under the government’s open acreage licensing policy. Positive outcome for the same could further add value to the Assam block in the long term.

PY1 commissioning on track

HOEC completely owns the PY1 block in the Cauvery basin and is currently undertaking drilling work for re-entering in two wells to enhance production. Drilling and commissioning work is in full swing and is expected to be completed by July. The company plans to fund the entire work through cash generated internally and maintain the debt free status as of now.

Realisations from incremental production are expected to start after its July completion, which would provide another boost to revenues and profits. Moreover, total reserves in the basin are now believed to be much higher that initial projections which would also work in favour of the company in the long term.

B80 following timeline

The field development plan for the B80 basin in Mumbai High was approved in December last year and block execution is on track. The management expects to commence production from the block from April 2020.

Geopetrol acquisition

In April, HOEC acquired Geopetrol International, which has a 30 percent participating interest in the Kharsang field in Arunachal Pradesh. The entire acquisition was funded through internal accruals. The management feels this acquisition is in line with the company’s plans of expanding its presence in the Northeast and bodes well with the already invested infrastructure. It also makes the company the largest private player in the Northeast.

Outlook

The company has a debt-free balance sheet, immense scope to benefit from leveraging in the future and capacity for inorganic as well as organic expansion. The company has an asset portfolio of discovered reserves in all blocks with a plan to systematically monetise resources and seems well positioned for future growth.

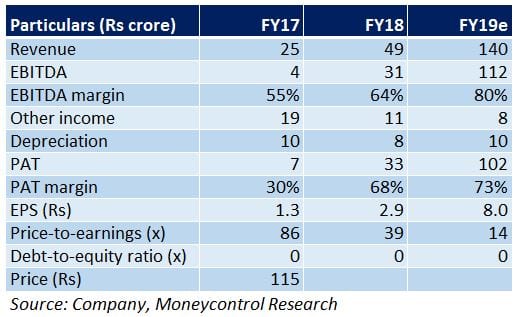

The stocks has run up 66 percent in the last 12 months and is currently 25 percent below its 52-week high. It is trading at a FY19e price-to-earnings of 14 times. With a turnaround in revenue and profitability, we see scope for a re-rating. HOEC is a growth stock. Investors with a penchant for investing in high growth businesses should look to add on any weakness in the current market volatility.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.