Bajaj Corp’s quarterly result underlined better offtake in rural areas, underlining improving consumption demand. High single digit volume growth was comforting though the same was aided by a weak base. However, fragile recovery in light hair oil segment, competitive intensity and higher raw material cost keeps us on the sidelines.

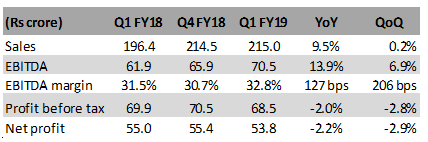

Result snapshot: Growth aided by base effect The company reported Q1 FY19 sales of Rs 215 crore which is at the same level as Q4 FY18 and translates to a 13.2 percent year-on-year (YoY) growth after adjusting for Goods & Service Tax. Volume growth of 8.7 percent was aided by soft base as was the case last year, wherein there was a volume de-growth of 7.8 percent.

Q1 FY19 financial snapshot

Earnings before interest, tax, depreciation and amortisation (EBITDA) margin was robust at 32.8 percent on account of moderate increase in raw material cost (7 percent YoY) and flattish other expenses, despite a steep rise in employee cost (31 percent YoY). Net profit, however, declined due to lower other income.

Adjusted landed cost of Light Liquid Paraffin (LLP), which is about 30 percent of total cost, was a mere 4 percent higher than last year after accounting for relevant input tax credit. However, this may not be like-for-like comparison after accounting for the GST impact. Sequentially, LLP landed prices increased 7 percent and remains a key parameter to look at. Another important cost input - refined oil prices (13 percent of total cost) - remains at same level as in Q4 FY18.

Volume growth pick up but on a low base Overall topline growth was driven by 11.2 percent YoY volume growth of flagship product (Almond Drop Hair Oil), where rural demand seems to be gaining traction. ADHO offtake growth in rural areas was 1.3 times higher than urban in both volume and value terms. The management emphasised that ADHO value and volume growth in rural was higher than the overall total hair oil market, which implies that some premiumisation is at play.

Volume growth (4 percent YoY) in Nomarks was weak on account of reduced trade pipeline prior to its relaunch in Q1 FY19. While there has been a perceptible slowdown in category, the management acknowledges higher competitive intensity but is also hopeful of a 25-30 percent growth in the next 3 years.

Other products have been disappointing on the revenue front. However, offtakes for Bajaj Coco Jasmine Hair Oil and Bajaj Brahmi Amla Ayurvedic Hair Oil have improved due to distribution expansion.

Volume growth on an uptrend

Trade channels performance skewed Both general trade and modern trade channels have exhibited double digit sales growth. Excluding Canteen Stores Department (CSD) domestic business value growth was 18.6 percent YoY. Exports and CSD sales have been sore points for the company. Regarding exports, the management is hopeful of an improvement from Q3 FY19 onwards.

Positives for the company from the Q1 earnings include growth revival in rural areas and improving distribution reach. Key challenge for HUL accrues from changing hair oil industry dynamics, which includes competition from low-cost manufacturers. While there is an improved traction for light hair oil industry last quarter, what needs to be seen is a re-emergence of trend in favour of light hair oil.

What keeps us cautious despite the inexpensive valuation multiple (27 times FY19e earnings) is the fact that volume growth (on a 2 year average basis) is still mediocre. The key risk is its ability to pass on higher input cost to the end consumer is formidable and remains a high business risk for a single product company.

Follow @anubhavsaysFor more research articles, visit our Moneycontrol Research pageDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.