Krishna Karwa Moneycontrol Research

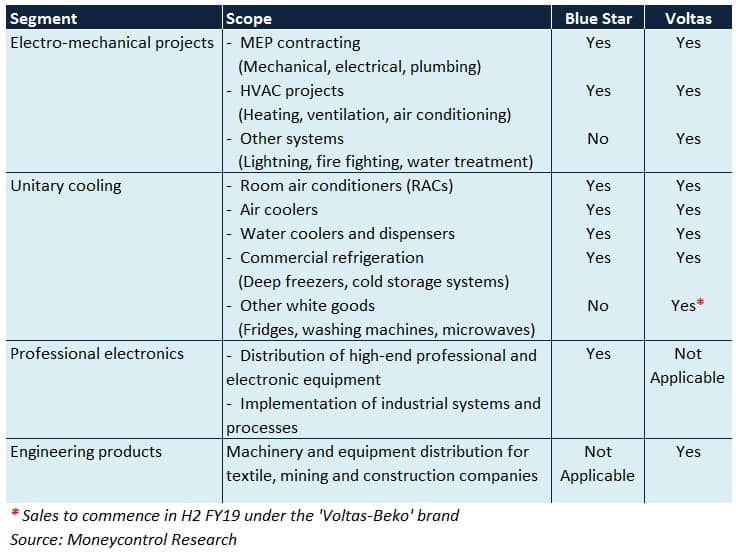

Blue Star and Voltas cater to a wide range of clients through their diversified product/service portfolio, particularly in the fields of cooling and engineering.

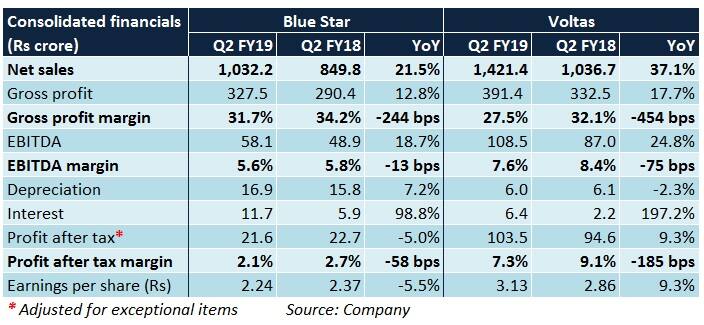

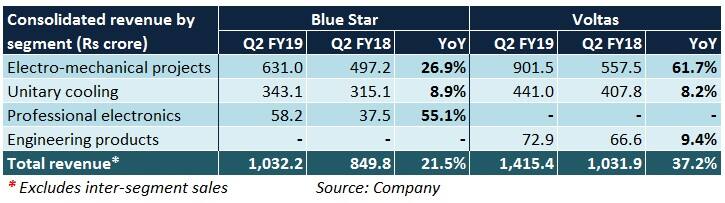

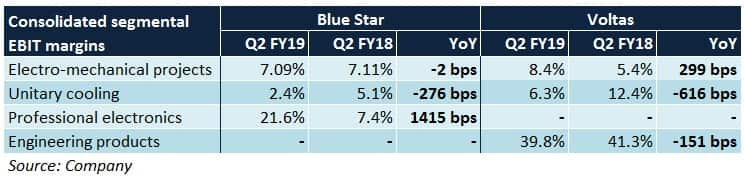

Q2 review

The electro-mechanical segment of both companies witnessed healthy top-line growth and an uptick in margin. For Blue Star, strong project execution capabilities (mainly government and education-based) and procurement efficiencies led to the improvement. For Voltas, domestic electrification projects, an increase in international orders and foreign exchange benefits were the key performance drivers.

The unitary cooling segment of both companies bore the brunt of weak Onam sales (because of Kerala floods), unfavourable weather (rains) and higher input costs. This led to a sharp margin contraction as well.

For Blue Star, increased billing, commission revenue from supply of CT scanners to the Uttar Pradesh government and sale of non-destructive testing equipment worked in favour of its professional electronics segment.

For Voltas, focus on after-sales services (in connection with textile machinery) and the relatively profitable Mozambique-based operations (involves sale and services pertaining to mining and construction activities) helped the engineering products segment report a decent set of numbers.

The path ahead

(A) Electro-mechanical projects

Government contracts and urban infrastructure projects (airports, metros, malls, hospitals, hotels, electrification) are anticipated to drive most of the order book growth.

To reduce strain on the working capital and improve profitability, Blue Star and Voltas will be selective in choosing new projects. Only those assignments that meet specific criteria (on fronts such as ticket size, reasonable cash flow certainty and margins) defined by each company will be preferred.

Going forward, though projects in India will be prioritised, there is no dearth of opportunities in the Gulf countries. Events such as Expo2020 (UAE) and FIFA world cup (Qatar, 2022) could provide both a chance to bag new big-ticket contracts.

However, the possibility of industrial capex or growth reviving in the near future is bleak, especially in case of private sector enterprises. This is attributable to negative market sentiments and liquidity tightening in the banking system. Cost escalations, longer gestation periods and changes in regulatory policies are among the other risks in this segment.

(B) Unitary cooling

In the long run, impetus will be laid on boosting the contribution of inverter air conditioners (ACs) to total revenue because of their margin-accretive nature. On a positive note, the commercial refrigeration domain (primarily food storage, restaurants and medical facilities) is promising.

A weak Q1 (unseasonal rains in most regions of India in summer), followed by a sluggish Q2 (due to monsoons), has caused an AC inventory build-up across the trade channels. In recent times, festive demand hasn’t been up to the mark either.

Furthermore, in Q3 and the first half of Q4, sales will remain subdued because of winters. Consequently, FY19 should be a lacklustre year as far as this segment is concerned.

To liquidate stocks and tackle stiff competition from other brands, steep discounts may be offered by taking price cuts. Rupee’s depreciation versus the US dollar, coupled with a hike in basic customs duty (BCD) on certain white goods and components thereof, will put downward pressure on margin.

For Voltbek, a 50:50 joint venture between Voltas and Arcelik, the impact of higher BCD will be even more. This is because it will import finished goods (washing machines, refrigerators, microwave ovens, dishwashers, other kitchen appliances) from Thailand, China and Turkey till the manufacturing facility at Sanand, Gujarat, commences operations. Given the high dealer margins and increased marketing spends, achieving break even in the initial years seems unlikely.

(C) Professional electronics (Blue Star)

Supply of high-tech cameras (50 percent of such orders was executed in H1) will be concluded by FY19-end. As per the management, 20 percent margins are sustainable in this segment because of the niche nature of products.

(D) Engineering products (Voltas)

Mining operations in Mozambique have been witnessing good growth momentum of late, which should facilitate machinery sales. In contrast, there isn’t much to look forward to on the domestic front.

High cotton costs, leveraged balance sheets and low yarn realisations are the issues that plague India’s textile industry at the moment. With no turnaround in sight anytime soon, textile machinery sales aren’t going to pick up.

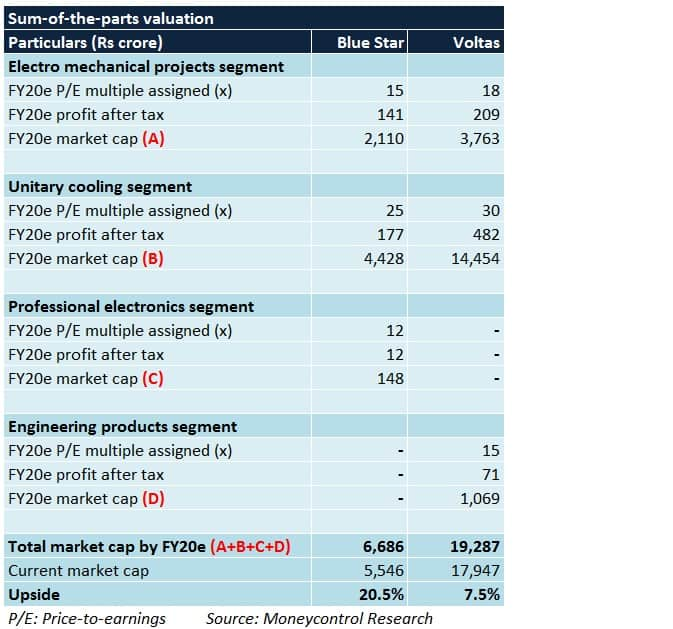

Outlook

Barring unforeseen climatic disruptions, air conditioning as an industry is secular in the Indian context. This is predominantly attributable to low penetration levels of ACs, tropical weather and higher disposable incomes. An extensive pan-India network provides Blue Star and Voltas a good opportunity to capitalise on this advantage.

Both companies have also been working towards achieving brand extensions and bolstering their pan-India visibility. For instance, Blue Star is scaling up its water purifier sales, whereas Voltas has forayed in the air cooler space.

FY19 will end on a low note for Blue Star and Voltas. This is because the unitary cooling segment, comprising nearly 50 percent of annual consolidated revenues in case of each company, has already faced major difficulties in H1 FY19. To add to the woes, for the most part of H2 FY19, there is not much to look forward to in terms of AC sales. Therefore, we advise investors to buy these stocks on price weakness.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.