Which pocket of the Government should be enriched has taken forty-four years to decide — a classic case of what ought not to be!” — Thus began a scathing judgment from the Supreme Court recently. The dispute wasn’t particularly remarkable. The assessee was the government-owned National Cooperative Development Corporation (NCDC), set up by Parliament in 1962 to advance loans or grant subsidies to co-operative societies, out of funding from the central government.

The funds so received from the central government were a capital receipt, and therefore not chargeable to tax. The interest received by the NCDC on loans advanced by it is chargeable as business income — again undisputed. The dispute was only whether the interest paid by the NCDC to the government on funds received was allowable as a business expense. After protracted litigation spanning four decades, the Supreme Court ruled that the expense was deductible, but not without admonishing the government for its role in the mounting case-docket confronting the judiciary.

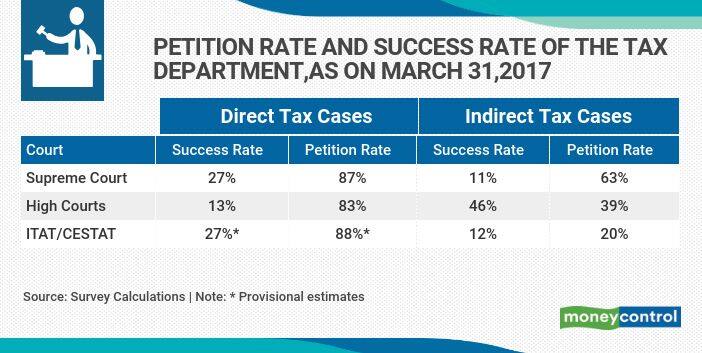

To be sure, the government is well aware of the problem. The Economic Survey 2017-18 estimated that as of March 2017, there were 137,176 pending tax cases, out of which 66 percent involved each less than Rs 10 lakh in claimed amount, and cumulatively constituting a mere 1.8 percent of locked up value of the total pending cases. What is even more surprising is that 90 percent of all of these petitions are filed by the department, while its success rate was under 30 percent. [Table Below].

Remember, the effort taken, as well as the cost incurred, in prosecuting cases are the same, irrespective of value (unless it is a high-profile case such as the Vodafone tax case). Similarly, a judge spends the same amount of time deciding each of these low value cases as they do for the others. The more cases pending before a judge, the longer each of them will take to decide, on an average.

From the point of the small-taxpayer too, these are not merely an avoidable distraction, but also a needless cost in the form of defending claims. Compensation for ‘costs incurred’ are very rarely awarded — even in the instant case, parties were left to bear their own costs. It is a no-brainer that the department can significantly reduce the number of cases they are contesting. More so, when a 66 percent reduction in total cases equates to only 2 percent in foregone revenue.

Most tax disputes can anyway be traced to instances where a given rule can be interpreted in two ways. For a risk-averse officer, the easy solution is to adopt the interpretation advantageous to the department. Then there are also ample tales of instances where tax officers pass adverse orders simply because their palms were not greased.

A scheme introducing Faceless Assessments, where the officer will be blind to the identity of the taxpayer being assessed, was notified on September 25. Assessment orders will have to be approved by a superior to the tax officer concerned. This will inject accountability at the earliest stage of the litigation itself. However, tax officers caution, this could lead to even more chaos.

Typically, before passing an order, the assessing officer grants the taxpayer an opportunity to explain a suspicious or unexplained transaction. However, under ‘Faceless Assessments’, the officer will have to make a decision entirely on the basis of the material that has been filed. It is quite likely that anything that is doubtful will be decided to the prejudice of the taxpayer — this could mean even more cases, and longer time for resolution.

The judgment, instead, proposes (in cases of tax disputes with government companies) a system of Advance Ruling where the assessee is given an estimate of how a certain transaction will be taxed a priori. However, the Advance Ruling system that is already followed in cases involving non-resident taxpayers is anything but satisfactory.

One could shrug ones shoulders and call this a beast that will not be tamed. That doesn’t serve the purpose. Perhaps the answer is to not see taxpayers as adversaries and tax-cheats in the first place. Greater forbearance will also mean that efficiency of tax-officers should not be assessed purely on the basis of the tax collected. This would also free up departmental resources to pursue tax-evaders and high-value assesses with better investigations and forensic analysis.

Both of these are within the government’s powers. With a robust Tax Deduction at Source in place, it is quite likely that most citizens do pay their fair share of taxes anyway.

Abraham C Mathews is an advocate practising in Delhi, and a chartered accountant. Twitter: @ebbruz. Views are personal.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.