Global investors are wondering these days if Beijing has decided to ease a yearlong regulatory crackdown that has cost them more than $1 trillion in losses. After all, China accounts for about one-third of the emerging markets benchmark index. It’s simply too big to be ignored.

With no clear statement of policy on offer, asset managers have resorted to reading tea leaves. For instance, a deal that would allow the US securities watchdog to review the audit documents of New York-listed Chinese companies in Hong Kong could be a sign that China is again eager to attract foreign investments. Beijing can also try to appease capital markets by reviving the listings of Didi Global Inc. and Alibaba Group Holding Ltd.’s fintech affiliate, Ant Group Co.

So far, there have been mixed signals. Take the housing market, where local governments have been flip-flopping. On September 15, industrial hubs such as Qingdao and Suzhou scrapped second-hand and non-resident home purchase restrictions, respectively, only to backtrack the morning after. These hiccups prompted investors to conclude that President Xi Jinping’s mantra that housing is to be lived in, not speculated upon, remains firmly in place. As such, August’s mini-rally in property developers’ high-yield dollar bonds quickly lost steam.

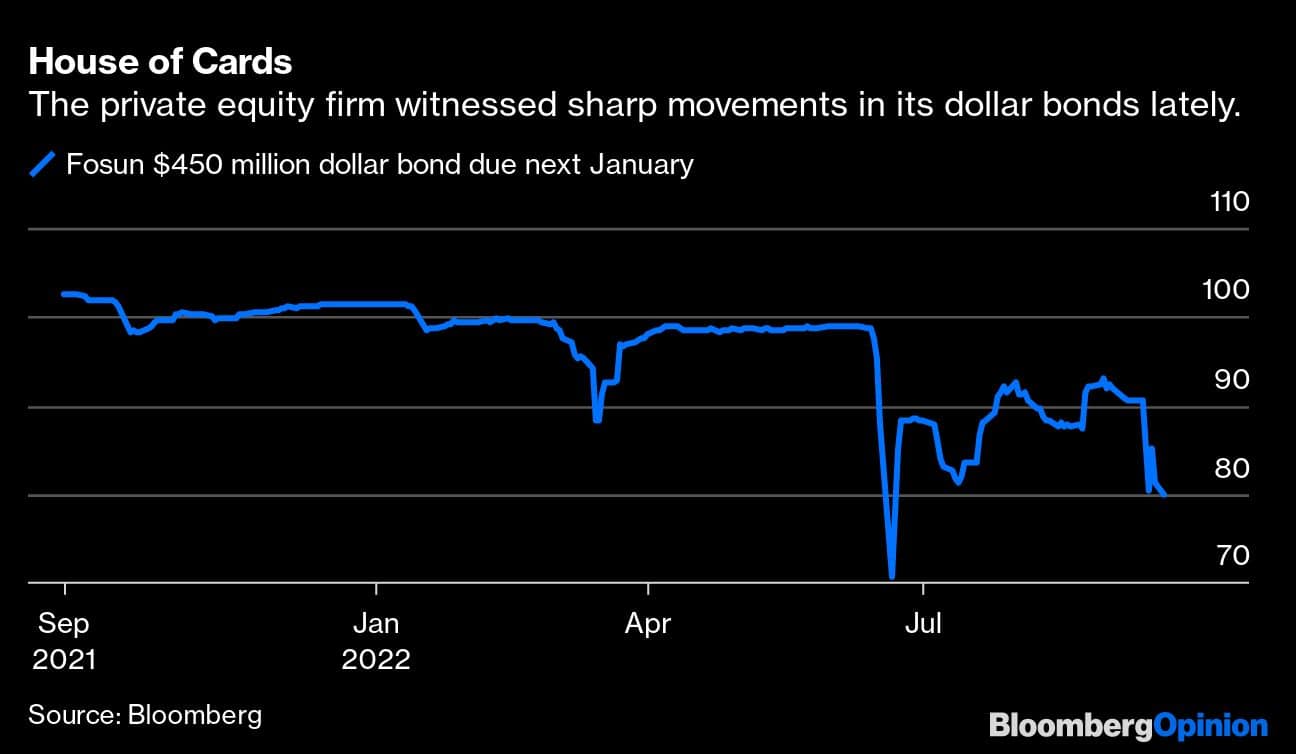

Adding to the mixed bag is Shanghai-based private equity giant Fosun International Ltd., whose empire includes an English Premier League football club, Portugal’s biggest bank, and French resort group Club Med. Its stocks and bonds witnessed sharp selloffs recently, as global ratings agencies downgraded the company, citing refinancing risks.

Those risks reflect investor worries over meddlesome government authorities. Last week, Fosun’s in-house Communist Party secretary paid a visit to the Beijing branch of Sasac — the State-Owned Assets Supervision and Administration Commission of the State Council — the company said in a statement.

The powerful agency has witnessed selling pressure in some of its portfolio companies lately. In early September, a Fosun subsidiary pledged a 7.9 percent ownership stake in Beijing Sanyuan Foods Co. to a brokerage. Sanyuan’s largest shareholder is a State-owned enterprise directly supervised by the Beijing Sasac.

Fosun said Beijing Sasac conducted a routine information-collection survey with the company, and the agency has issued such notices to other enterprises before. The two parties conducted in-depth exchanges on the long-term co-operation between Fosun and Beijing’s State-owned businesses.

In another era, investors might have just dismissed Fosun’s Sasac visit. But coming off a bruising crackdown, where little-known government agencies sprang out of nowhere to wipe billions of dollars off companies’ market values — think of the cybersecurity watchdog’s hawkish stance that ultimately led to ride-hailing giant Didi’s delisting from New York — traders are understandably skittish.

If we use loan-to-value ratio as a measure of financial safety, at 39 percent, Fosun’s balance sheet is healthy for an investment-holding company. However, with not enough cash on hand and dollar bond market access closed, Fosun must rely on bank-loan refinancing and speedy asset disposals to meet its short-term obligations. About 53 percent of its debt will mature in a year, according to S&P Global Ratings. In other words, Fosun’s ability to quickly divest its investments is crucial.

With only 117 billion yuan ($17 billion) in debt, Fosun is nowhere close in scale to China’s indebted developers. However, the company matters because it is a key barometer in the high-yield corporate bond market. Last year, when real estate developers crumbled – about one-third of the top 100 builders defaulted or asked for loan extensions – Fosun became the natural destination where investors could park their cash. It’s got scale, liquidity — and until recently — a decent credit rating. Fosun has about $4 billion of dollar bonds outstanding, with its smallest issue at a respectable $450 million. It used to be a BB-rated company.

Now, that safe haven may not be so safe. The high-yield corporate dollar bond market has chilled some more.

When a company edges toward distress, credit analysts can always point fingers at one metric or another, saying its cash flow management could be better. However, even the best private businesses can go bad if the government gets overly zealous or meddlesome.

In capital markets, the Chinese government doesn’t have the best reputation right now. If Beijing still wants foreign capital, it needs to tell its various agencies to stay low and keep quiet. Their unprompted visits with business scare investors.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. Views are personal, and do not represent the stand of this publication.Credit: BloombergDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.