Asset allocation is no longer an alien word to the investor community. Many of them may not be following the process. However, they are aware that it makes sense to distribute the investments into different asset classes, to diversify the risk, and optimise returns.

Asset allocation is generally decided on the basis of risk profile of the investor and goals targeted. The allocation is rebalanced at regular intervals so that the portfolio should not be overboard on a single asset class due to its recent performance. In financial planning asset, allocation rebalancing is one of the important steps in the complete process.

While formulating asset allocation strategy, sometimes the long term goals are kept as base and a strategic asset allocation is decided, but In some cases looking at the market performance and under expectation of the near term performance considering factors like Price to Equity (PE) or Price to Book (PB), a tactical asset allocation is formed for a short time frame.

Practically, I have experienced that in the distribution stage i.e. when one is very near to the goals and is about to start using the money accumulated, neither strategic nor tactical allocation serves the purpose in investment management. This stage calls for completely different strategy, so as the money should not be lying idle in the savings bank account and also it should not be into high risky category of equity, which calls for timely rebalancing.

Generally, the two important distribution stages, where the money usage is divided into different years and calls for a specific and different strategy are the child education and retirement. Child higher education years are generally of 4-6 years, and one should be ready for those at least 2 years before the goal starts, thus one need to plan and allocate the money for 6-8 years’ time frame with annual withdrawal.

Same way in the case of retirement, one should not park the complete money in debt oriented investments to seek out the safety only, and to manage the Inflation part one cannot avoid equity completely. Since, retirement is quite a sensitive stage, so one need to have a balanced approach in allocating the money to take care of regular income requirement of the retiree.

Mutual funds play a very important role here. As they come up with different structures and strategies, so they easily get fit in the requirement.

In the case of child education, one can make use of different mutual funds structures by following a laddering strategy. In laddering, the different years requirement are invested into different funds suitable for that particular time frame, so that one should not compromise with the returns and manage the inflation well. Let’s understand this with an example.

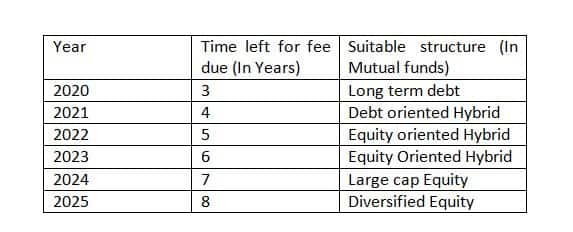

Saurav’s daughter’s education is due three years from now. She would be going for engineering and then MBA. Saurav has saved enough money for this goal, and followed strategic asset allocation of 70 equity and 30 debt. But now when he is getting near to the goal, he is finding difficulty in managing investments the asset allocation way, as going forward the confusion will increase as to which asset class one should withdraw to pay off the education cost. Moreover this is also said that one should reduce the equity exposure while nearing to the goal. All this leads him to allocate with purpose.

He can divide the complete education cost into different years of requirements and invest the money into different products, looking at the product structure and risk prevalent

Since the first fee installment would get due 3 years from today, so it is not advisable to park the money in equity and last fee would be due after 8 years, so debt may not be suitable for that.

Following this strategy, investor can manage the risk of inflation very well, without compromising on the growth aspects.

Coming to retirement, which is spread across many years, and one may not sure where is the end, so in those years the laddering strategy may not work. One needs to follow a completely different investment allocation strategy, called as bucketing.

The complete retirement corpus to be divided into three buckets with different investment products, so that the requirement of monthly income can be met with ease adjusted to inflation.

The first bucket is meant for immediate monthly requirement, which is invested in products giving regular interest payouts like post office schemes or bank FDs or which can be used for SWP like ultra short term or short term mutual funds to further supplement the monthly income.

The second bucket is meant to feed the first bucket as and when required, but is not invested in the regular interest bearing instruments and also not in highly volatile instruments. So hybrid funds suit this bucket.

The third bucket is meant for the overall growth of the portfolio, and thus the corpus is invested in equity instruments for long term. Though this bucket may be used to keep feeding the second bucket through dividends, but is not to be used for regular withdrawal.

Depending on the requirement, risk tolerance and other incomes coming from different sources, money can be invested for in different buckets. Do remember to keep one bucket to manage the health Issues too, so you may say it’s a three and half bucket for retirement years.

Conclusion:Allocating with purpose works best in the distribution years of the Investor, and there has to be well thought of approach while selecting investments for different strategy. Taxation along with inflation needs to be managed properly.

Manikaran is a member of The Financial Planners’ Guild , India (FPGI). FPGI is an association of Practicing Certified Financial Planners to create awareness about Financial Planning among the public, promote professional excellence and ensure high quality practice standards.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.