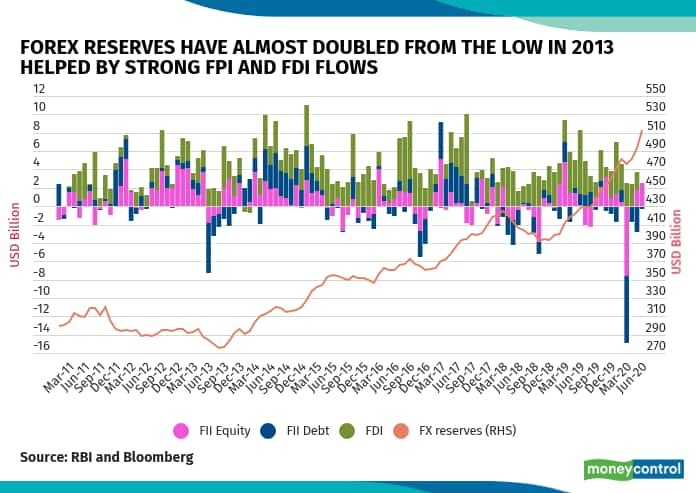

The improvement in India’s external fundamentals is a notable and positive development amidst the sombre economic mood in the backdrop of COVID-19. The country’s foreign exchange reserves have grown rapidly to cross $500 billion.

The pace of reserves accumulation too has increased. Reserves have jumped by $30 billion so far this financial year compared to $65 billion in 2019-20. That’s because India’s external financial requirement has reduced with a sharp fall in the current account deficit (CAD) from 2.4 percent of GDP in FY19 to 0.9 percent in FY20. At the same time, net capital flows have picked up from 2 percent of GDP in FY19 to 3 percent in FY20. Importantly, stable FDI inflows accounted for almost half the net capital inflows and external commercial borrowings, another 28 percent.

During the first quarter of the current financial year, the current account, which showed a small surplus in the last quarter of FY2019-20, would have seen a bigger surplus as imports fell thanks to the collapse in oil prices and the national lockdown. In fact, merchandise trade recorded a surplus for the first time in 18 years in June. Capital inflows, on the other hand, have remained strong. The Reserve Bank of India has intervened in the markets to absorb these flows and also prevented a sharp appreciation of the rupee.

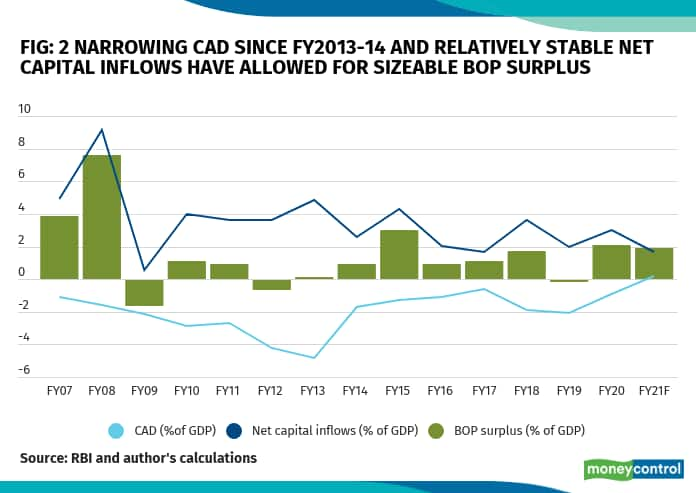

The central bank has been accelerating its addition to forex reserves ever since the rupee came under intense depreciation pressure during 2011-2014 as the CAD widened sharply. Since then, lower oil prices and targeted measures to reduce imports of gold and electronics have helped reduce the CAD to manageable levels while an improvement in the domestic business environment and abundant global liquidity have seen net capital inflows increase in size. The RBI has been absorbing the resultant BoP surplus to build foreign exchange reserves and buttress the economy’s macroeconomic stability.

A sizeable reserve position enhances the ability of Indian central bank to deal with episodes of sharp rupee depreciation and curb volatility in the short-term in a flexible exchange rate regime. If forex reserves are inadequate, then the central bank may have to raise rates rapidly to attract capital or raise dollars through other costly means like issuing bonds to NRIs. The RBI aims to curb sharp volatility in the exchange rate of the rupee in either direction.

This year’s reserve build-up has also been the main source of money creation at a time when monetary policy has been put to use extensively to counter the negative growth shock and tightening of local financial conditions. A rapid increase in the foreign exchange assets of RBI has been a key source of infusing large amounts of liquidity in the banking system, in support of the broader monetary accommodation.

While $500 billion is a big number, is it adequate? We assess the adequacy of foreign exchange reserves on the basis of external financing requirements, which is measured by the months of import cover, expected current account deficit and external debt maturing over the next one year. The International Monetary Fund looks at these yardsticks and more.

As per the IMF metric, over 2015 to 2019, India’s minimum requirement for reserves increased from $230 billion to $281 billion; actual reserves increased from 156 percent to 169 percent of that requirement. Based on the 2019 metric, the current reserves position is at 180 percent of the minimum requirement.

However, post COVID, the risk of lumpy capital outflows due to events such as the global risk sell-off in March 2020 and the expected contraction in GDP this year call for abundant caution.

In FY21, the current account is likely to register a small surplus (around 0.3 percent of GDP) on the back of a contraction in non-oil, non-gold imports as demand weakens, and lower oil prices despite a likely contraction in merchandise exports, NRI remittances and even software exports. This makes the current reserves position fairly comfortable. Forex cover for external debt has also improved to 86 percent of the total debt by the end of March 2020, the best in 8 years. Of the total debt, the short-term debt by residual maturity is about $235 billion and the cover for that debt is at 49.5 percent. With a significant part of the country’s debt due for repayment in the current fiscal year, there is enhanced refinancing risk considering the global financial market backdrop and COVID-19.

Sizeable foreign exchange reserves place India in a better position to deal with this risk, especially in case global financial conditions tighten again for emerging market borrowers. Moreover, the BoP is likely to record a surplus in FY2020-21 too, though smaller than a year ago because of muted and volatile capital flows. Capital flows from FPIs could turn negative over the year and other inflows like external commercial borrowings and even FDI could slow down on protracted global capital flows to EMs. That in turn implies that the pace of reserve accretion this year would be lower than last year, despite the sharp increase seen in the first quarter.

The comfortable reserves position imparts a certain degree of independence to monetary and fiscal policy to provide more stimulus as foreign exchange reserves act as the first line of defence to counter any sharp depreciation pressures on the rupee. Sovereign ratings agencies and international investors too look at emerging markets with strong foreign exchange reserves position and low external financing requirements, favourably.

That in turn will provide the central government greater freedom to follow an expansionary fiscal policy to support the economy, without having to unduly worry about the near-term ramifications on the availability of external financing and the exchange rate. After depreciating sharply against the US dollar in March 2020, the rupee has stabilized over the first quarter of this fiscal year.

Depreciation pressure on the rupee can rise again over second or the third quarter as the growth retarding effects of lockdowns become clearer along with fiscal slippage concerns. A contraction in the economy for the first time in 40 years, uncertain duration of the COVID-19 crisis and a clouded inflation outlook, could trigger another round of FPI sell-off in debt and equity. A comfortable foreign exchange reserves position will help in managing large portfolio capital outflows, if that happens, without putting undue pressure on domestic financial and credit conditions.

(The author is the chief economist of IndusInd Bank. Views are personal.)Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.