The Budget for the current fiscal year, along with the usual fiscal maths, would look to provide a road map for achieving the new government’s core objective – doubling the size of the economy to $5 trillion over the next 5 years.

In light of growth slipping to an 18-quarter low as per the last GDP reading, the immediate focus will be to counter the slowdown through a fiscal stimulus. That, along with the easing bias of the monetary policy, would help in a cyclical recovery back towards the potential growth rate of about 7 percent over the year.

Pushing the potential growth rate higher though will require reforms to provide activity momentum beyond just a cyclical recovery. The question then is what are the fiscal policy reforms that can help in accelerating growth to help reach a $5 trillion economy. A June 2015 IMF policy paper titled ‘Fiscal policy and long-term growth’ provides some very important insights on that issue.

The paper analyses the relationship between fiscal reforms and subsequent growth accelerations in a cross-country setting for 112 economies over 1975-2013. The study focuses on 143 episodes of protracted growth accelerations over the sample period and relates them to entrenched improvements in revenue and expenditure composition ahead of those episodes.

Growth acceleration is defined as durable increase in five-year average growth of at least 1 percent. Fiscal reforms are defined as protracted growth-friendly improvement by at least 2 percent over 3 consecutive years at least in key revenue and expenditure indicators. Based on that analysis, the paper concludes that fiscal reforms have a high probability of being followed by a growth acceleration, but the exact likelihood varies across country groups and reform types.

For instance, a combined package of both revenue and expenditure reforms has a 60 percent likelihood of being followed by growth acceleration, but the association is strongest in advanced economies (80 percent) followed by emerging economies (67 percent) and low-income countries (38 percent). However, standalone revenue reforms or expenditure reforms are followed by growth accelerations in 26 percent and 21 percent of reform cases, respectively. For emerging economies, revenue reforms are found to be more growth supportive compared to advanced economies where expenditure reforms provide better results.

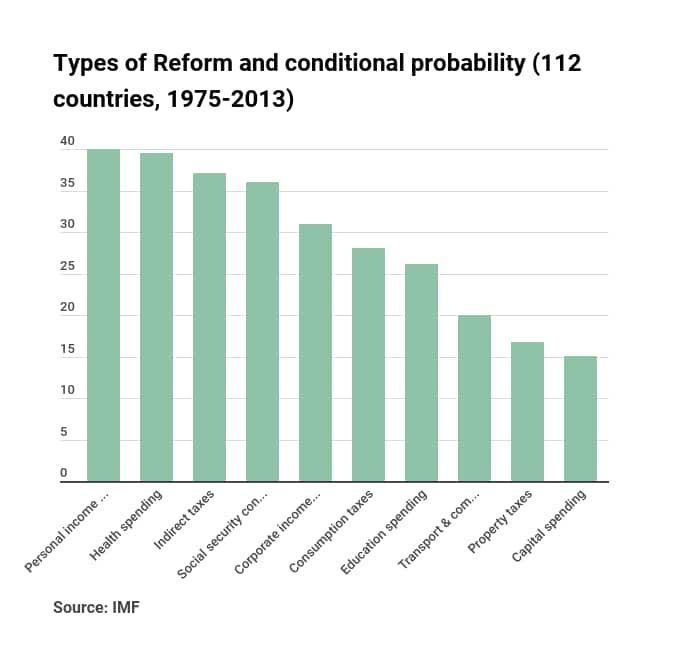

The paper further explores specific revenue and expenditure reforms and their relationship with growth acceleration. On the revenue side, measures aimed at reducing the share of direct taxes (corporate, personal and social security contributions) are most likely to be followed by growth accelerations. The probability was the highest in cases of personal income taxes at 40 percent, with a 31 percent probability in cases of corporate tax reduction, as these reforms help improve supply of labour and capital.

Reform in areas of consumption and property taxes were found to subsequently accelerate growth in 28 percent and 17 percent cases, respectively. On the expenditure side, sustained increase in health and education spending was followed by growth acceleration in 40 percent and 26 percent of the reform cases respectively, as they help in further improving labour productivity. Similarly, increase in capital spending and more specifically targeted increase in transportation and communication spending, are found to accelerate growth in 15 percent and 20 percent cases, respectively.

Using an alternative model to study the effects of fiscal policy changes on growth, the paper finds that even Budget neutral fiscal reforms aimed at enhancing the tax system efficiency or shifting the composition of Budget spending towards infrastructure investment, may lift long-term growth by 0.5 percent and 0.25 percent, respectively. The paper, therefore, makes a case of a comprehensive package of revenue and expenditure reforms, to complement other structural reforms, to help push up growth over the long term. (See Fig. 1)

Over the last 5 years, fiscal policy in India too has seen some major reforms, focused mainly on the taxation side, through the introduction of GST and steps to improve compliance rates on the direct taxes. On the expenditure side, where the scope for re-orientation is limited, due to committed nature of almost three-quarters of total spending (on salaries, subsidies, interest payments, transfers to states etc.), the main focus has been on capping the subsidies bill by reducing leakages and vulnerability to oil prices. Capital expenditure has also been increased on roads and railways network though a large part of the capex has come from off-Budget spending by central public sector entities.

Over the next 5 years, drawing on above-mentioned the cross country experience, a combined revenue and expenditure fiscal reforms package would help accelerate long-term potential growth. On the tax revenue side, a shift in composition towards indirect taxes by simplification and broad basing of the GST, along with a reduction in direct tax rates with a rationalisation of exemptions, should be pursued.

That would help reduce reliance on non-tax revenue sources like disinvestment and RBI dividend. While the new direct tax code is awaited, this Budget can initiate the process of rationalizing the structure by providing a road map for removing exemptions and reducing direct tax rates, which would help in improving the compliance levels. On the expenditure side, the case for higher capital spending on infrastructure is a strong one, given its growth enhancing nature.

The April 2019 monetary policy report of the RBI estimates that the peak fiscal multiplier for capex by the central government is 3.25 i.e. a Re 1 increase in capex would raise GDP by Rs 3.25, versus Re 0.45 in the case of revenue expenditure. Given that the room for fiscal stimulus is limited by the need to reduce the fiscal deficit and public debt to 3 percent and 60 percent of GDP, respectively, over the next 5 years, a balancing act would be required and therefore, the pace of tax rationalisation or expenditure orientation, would accordingly be slower. However, the need for pursuing fiscal reforms cannot be understated in the endeavour to push growth to higher levels on sustainable basis.

Even on the institutional front, the time has come to consider setting up an independent fiscal council, to oversee sustainability of the fiscal policy, especially on the consolidation front. This was recommended by the FRBM Committee, too. Another 2014 IMF study of Budget institutions in G-20 countries showed that strong Budget institutions tend to deliver a more growth-friendly fiscal adjustment, considering that debt and deficits have an impact on long-term growth.

Another area which the Budget should address is transparency around financing spending through off-Budget borrowings of the CPSUs. While these entities have traditionally supported public investments through their borrowings along with direct budgetary allocation for capex, concerns have been raised by the use of such borrowings to defer the subsidy payments, especially for food and fertilisers, in order to meet fiscal deficit targets.

In summary, 2019 Budget should be used as an opportunity to initiate fiscal reforms which will push up the potential growth of the economy by enhancing labour, capital and total factor productivity. And, as fiscal stimulus is required for a cyclical recovery in the short run, some fiscal deficit slippage is likely and plausible as long as the fiscal consolidation path ahead is set firmly.

(The author is the chief economist of IndusInd Bank. Views are personal.)Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.