In a world where equity markets swing due to geopolitical headlines and fixed deposits (FDs) struggle to beat inflation, tax-free bonds stand out as an oasis of stability for investors.

With the RBI hinting at further rate cuts, the allure of locking in tax-efficient, fixed-income returns has never been stronger. But what makes tax-free bonds — particularly those traded in the secondary market — the cornerstone of savvy portfolios?

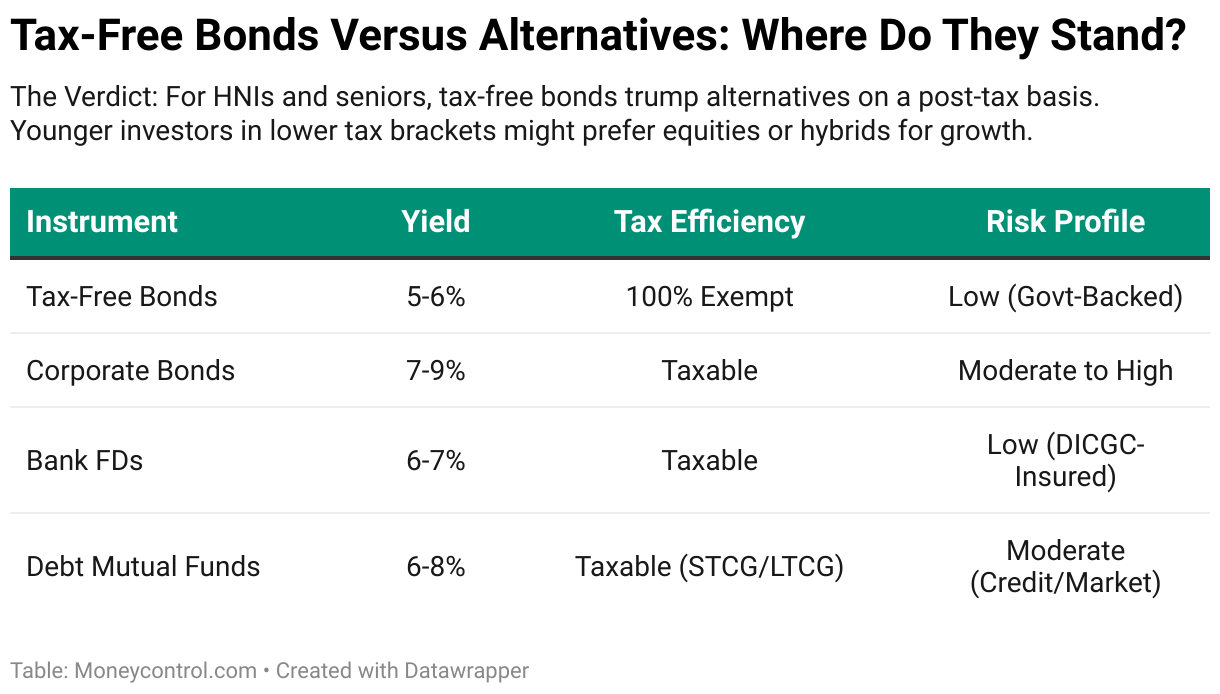

These bonds are debt instruments issued by government-backed entities like NHAI (National Highways Authority of India), REC (Rural Electrification Corporation), or PFC (Power Finance Corporation). Their defining feature? The interest earned is entirely exempt from income tax under Section 10 of the Income Tax Act. For high-net-worth individuals (HNIs) and senior citizens in the 30+ percent tax bracket, this exemption makes a modest 5-6 interest equivalent to 7-8 percent pre-tax returns from taxable instruments.

Also read | 34 SGB issues coming up for premature redemption: Should you redeem or hold?Consider this math:• Taxable FD at 7 percent: For a ₹10 lakh investment, ₹70,000 annual interest becomes ₹49,000 after 30 percent tax.

• Tax-Free Bond at 5.5 percent: ₹55,000 interest remains fully intact.

The difference? A derisked ~12.3 percent higher post-tax yield.

Who should invest?1. High tax bracket investors: if you’re in the 30 percent slab, tax-free bonds are your secret sauce. The higher your tax liability, the brighter these bonds shine.

2. Senior citizens: with predictable cash flows and near-zero default risk (most issuers are AAA-rated), they’re ideal for retirees prioritising capital preservation.

3. Portfolio diversifiers: even aggressive equity investors benefit by balancing volatility with steady, tax-smart income.

No new tax-free bonds have been issued by the government since a long time, making the secondary market the only avenue to acquire them. While these bonds often trade at a premium (e.g., ₹1,050 for a face value of ₹1,000), the calculus still favours buyers for a couple of reasons:

• Yield-to-Maturity (YTM) clarity: even at a premium, the effective YTM often beats taxable alternatives. A 5.5 coupon bond bought at ₹1,050 might offer a 4.8 percent YTM — equivalent to 6.85 returns on a taxable bond for investors in the 30 percent bracket.

• Rate-cut tailwinds: as the RBI trims repo rates, existing bonds with higher coupons become pricier. Early buyers will lock in today’s yields before fresh rate cuts erode future returns.

Also read | Falling interest rates: Senior citizens should lock into longer-term FDs, small saving instrumentsKey considerations1. Credit quality: stick to bonds from government-backed entities for peace of mind.

2. Liquidity vs hold-to-maturity: some bonds trade infrequently. If liquidity is a concern, align purchases with your investment horizon.

3. Tax on capital gains: while the interest is tax-free, selling before maturity will attract capital gains tax. Hold until maturity unless market prices justify an early exit.

4. Inflation hedge: with tenures of up to 20 years, ensure the YTM outpaces the expected inflation (currently ~5 percent).

While tax-free bonds shouldn’t dominate a growth-focussed portfolio, they play a critical role. Hence, allocate:

• 10-20 percent for aggressive investors: stabilise equity-heavy portfolios.

• 30-40 percent for conservative investors: replace FDs with better post-tax returns.

• 40+ percent for seniors: ensure reliable, low-stress income.

The suggested allocation is illustrative and represents a general trend, it's not personalised advice.With the Reserve Bank of India’s (RBI's) rate-cut cycle gaining momentum and finite supply in the secondary market, delaying could mean paying steeper premiums later. Here’s a potential action plan:

1. Assess your tax bracket: if you’re above 20 percent, tax-free bonds merit serious consideration.

2. Screen bonds: filter by issuer rating (AAA), maturity (10-15 years), and YTM using SEBI-registered platforms.

3. Consult an advisor: align purchases with broader goals — retirement, education, or legacy planning.

Also read | Equity mutual fund inflows hit 11-month low of Rs 25,082 crore in March: AMFIIn an era of fleeting stock market trends and inflationary pressures, tax-free bonds offer a rare blend of safety, tax efficiency, and predictability. They aren’t just a defensive play; they’re a strategic tool to optimise post-tax outcomes. As SEBI (Securities and Exchange Board of India) and online bond provider platforms democratise bond market access, this is a good time to embrace this asset class.

The author is co-founder of IndiaBonds.comDisclaimer: The views expressed by experts on Moneycontrol are their own and not those of the website or its management. Moneycontrol advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.