Aparna Karnik

It is important for investors to know whether their active fund managers are taking enough risk. Otherwise, it would seem that the investor is effectively comfortable with a return that is not expected to be very different from the benchmark index’s (‘might as well buy an index fund!’).

Returns and risks in equity investing are two sides of the same coin. This applies in the context of active funds too. Active funds aim to generate index-beating returns (also called alpha).

Meaningful excess returns over the index cannot be achieved unless fund managers build portfolios that are materially different from the index in their stock and/or sector composition. It would be interesting to put these observations in the context of some numbers.

Studying risks

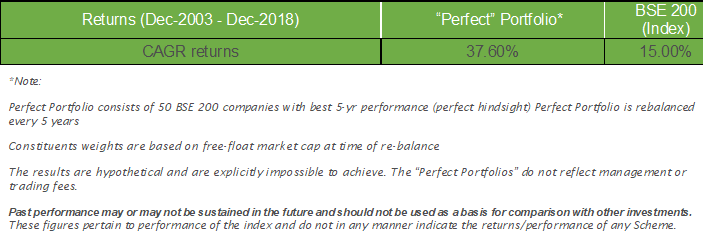

In a previous article, we had discussed our results from the study of the ‘perfect portfolio’. The ‘perfect portfolio,’ while completely hypothetical, serves as a useful point of reference. It assumes a perfect knowledge of the future and deliberately engages in ‘look-ahead’ bias.

We studied the risk statistics of the ‘perfect portfolio’ vis-à-vis the benchmark index (BSE200) and compared it with those of real portfolios. While it is not possible to achieve the sort of excess returns over the benchmark indicated by the Perfect Portfolio, which assumes an impossible level of skill – resulting in an information ratio (IR) of over three. Top-performing active managers typically have long-term IRs of between 0.5 and 1. It’s rare to find an active fund manager with a long-term IR that is more than one.

The IR is commonly used to assess the skill of active fund managers and is a measure of the excess return over benchmark index that the fund manager generates divided by the risk that the manager takes relative to the benchmark. It is computed as the ratio of the active return generated over the benchmark to the standard deviation of the active return (where active return is the difference between the return of the fund and the return of the benchmark index). The higher the IR, the higher the active return of the fund, given the amount of risk taken, and the better the manager.

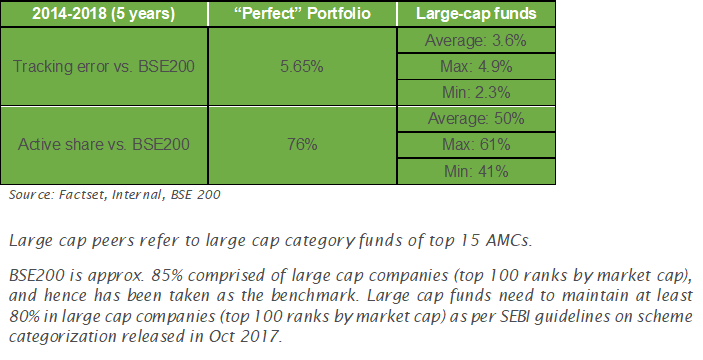

In this analysis, we have measured risk in two ways which are commonly used. The first is active share (the extent to which the fund deviates from the benchmark) and the second is tracking error (the divergence between the price behaviour of the fund and the price behaviour of the benchmark).

An active share of 0 per cent means the fund manager owns the benchmark constituents in the same proportion. An active share of 100 per cent means the fund manager’s portfolio is completely different from that of the benchmark.

Tracking error

Very low tracking error (TE) means that the fund and its benchmark move in perfect tandem. This is typically observed in ETFs or index funds. Another common interpretation of tracking error is that the portfolio returns are expected to be within (TE) percentage plus or minus the benchmark in approximately two out of three years. For example, if the tracking error is 3 per cent, then the portfolio returns are expected to be within + or -3 per cent of the benchmark index returns, for two out of three years. High tracking error means that the performance outcomes could be significantly different from that of the benchmark.

Self-defeating behaviour

The above risk statistics highlight that risk-taking propensity in many active large-cap funds is generally low. So, while the funds may not underperform the benchmark significantly, they are also not likely to outperform significantly. Adjusted for expenses/fees, the probability of meaningful outperformance becomes even lower.

There is a lot of academic research on the reason for this seemingly self-defeating behaviour of fund managers, part of which is attributed to investors’ short-term horizons for measuring fund managers’ performance. Active fund managers may be averse to truly hold on to big bets since they are not confident of investors’ ability to stay the course. Markets can be irrational in the short term (three years is not a long time in equity markets) and, it takes time, conviction and often involves taking a contrarian view to generate alpha. There may be a temptation or peer pressure to cut losses and buy into the popular themes of the day (also known as momentum investing) or to indulge in high trading activity.

To conclude, investors must include metrics such as IR, active share and tracking error when evaluating actively managed funds. Behaviour patterns that are akin to indexing or low risk-taking should not be rewarded in active fund management. In addition, investors also need to introspect and stop chasing near-term (1-year/3-year) performance as the sole criteria driving their investment decisions, since this is a self-defeating proposition and benefits neither investors nor fund managers.

(The writer is SVP, DSP Investment Managers)Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.