Usually, budgets necessitate at least some modifications to your tax workings and that’s why they create so much noise and excitement. At the same time, most taxpayers only want to know whether they will have to shell out more or less in taxes in the next financial year.

Unfortunately, Budget 2020 has left us with no clear answers. And therefore, it becomes important to solve the mystery that Budget 2020 is.

Unwise comparisonIf you assume the same income in both the regimes, then you will be better off with the new slabs. See the table below, it assumes exactly the same total income between the two regimes. The last column shows how much you’ll benefit from being in the new regime.

However, this comparison is unwise on two accounts. First, we all know that a salaried employee can get a standard deduction of Rs 50,000 without doing anything. Also, all salaried employees contribute to EPF. And this amount is eligible for deduction under section 80C. Employers automatically consider an employee’s contribution to EPF under section 80C deduction. Therefore, salaried employees can bring down their taxable income by at least the amount of standard deduction and their contribution to EPF without doing anything. Besides, all of us have at least some savings account interest and can claim a deduction of Rs 10,000 under section 80TTA.

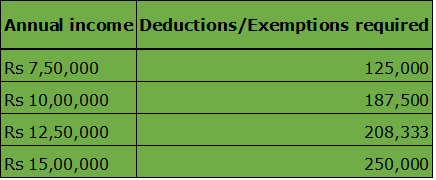

Deductions for saving on taxSo, will the standard deduction and your EPF contribution be good enough to keep you in the old regime? Unfortunately no. We did some analysis to find out how much exemptions and deductions you will need at various salary levels to make sure your tax outgo is the same in both the regimes.

The way to use this table is to keep your deductions and exemptions higher than the cut off number. If you cross this number, you stand to benefit from being in the old regime. At the above stated total of deductions/exemptions, your total tax outgo will be same in both the regimes. You can achieve these deductions with a mix of claiming HRA, LTA, Section 80C, Section 80D, food coupons, NPS investments among others.

It is important to note that senior citizens will not get a higher exemption limit under the new regime. Senior citizens are allowed a higher exemption limit of Rs 3 lakh if they are between 60-80 years of age and Rs 5 lakh if they are more than 80 years of age in the old regime. Even though senior citizens do not typically claim any HRA, LTA etc., they can claim a standard deduction of Rs 50,000 from their pension income. They are also allowed a Rs 50,000 deduction under section 80TTB for interest income. If they intend to park their funds in tax saving fixed deposit or renew their PPF for another 5 years and keep depositing in it, they can claim 80C deduction of Rs 1,50,000. If they are suffering from any specified diseases, they may be able to claim a deduction under section 80DDB. All of this can reduce their taxable income significantly in the old regime. And therefore, it may be worthwhile for them to carefully choose between the two regimes.

(The writer is founder and CEO, Cleartax )

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.