With the start of the new financial year 2022-23 on April 1, several changes in income tax rules come into force. Here are six important changes:

Taxation on virtual digital assets

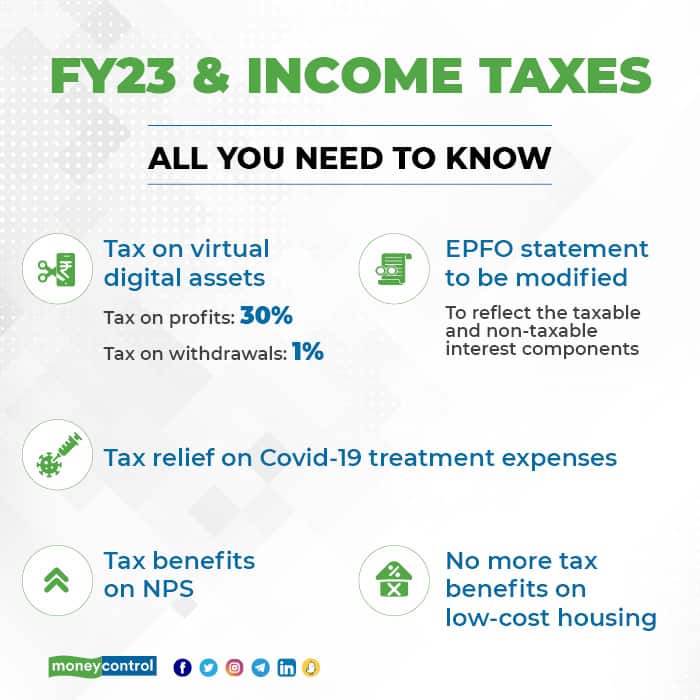

In Budget 2022, the government said it would tax income from the transfer of any virtual digital asset, including cryptocurrency. From April 1, income from cryptocurrency will be taxed at a flat 30 percent.

As per the proposed Section 115 BBH of the Income-Tax Act, 1961, a loss from transferring a virtual digital asset will not be allowed to be set off against income arising from the transfer of another virtual digital asset.

A 1 percent tax deductible at source under Section 194S of the Income Tax Act will apply to every single crypto transaction from July 1, 2022. TDS will be deducted at the time of redemption, whether one makes a profit or loss.

Higher tax benefit on NPS

From 2022-23, state government employees can claim tax breaks of up to 14 percent of their basic salary and dearness allowance on their employers’ contributions to their National Pension System accounts. Until now, the tax break was capped at 10 percent for state government and private sector employees – only Central government employees enjoyed the higher tax concession.

For private sector employees, the maximum deduction remains 10 percent.

Clarity on EPFO tax break-up

Starting in FY23, interest earned on your annual employees’ provident fund (EPF) contribution of over Rs 2.5 lakh (Rs 5 lakh for government employees) is subject to tax. The Central Board of Direct Taxes framed rules on taxing interest earned on this excess contribution in September 2021, effective from assessment year 2022-23.

From April, once the interest for FY22 is credited, there will be two sections in the EPF account statement – one reflecting the taxable component and the other the non-taxable portion.

Tax relief on Covid-19 treatment expenses

In June 2021, the finance ministry said income-tax will not be charged on the amount received by a taxpayer from her employer for Covid-19 treatment expenses.

Likewise, if financial assistance is received from someone else, that amount, too, will not be taxed. In addition, if a deceased Covid-19-affected individual’s family members receive any ex-gratia payment from an employer or anyone else, the amount will be tax exempt.

There are limits and conditions to avail of the relief. If a deceased employee’s family were to receive the ex-gratia from her employer after her death, no limit applies – the entire amount will be exempt from tax.

However, if someone else pays this amount, tax exemption is limited to Rs 10 lakh. Also, the exemption is valid only if the amount is received within 12 months from the date of death. If the family receives financial support from many people, the aggregate amount up to Rs 10 lakh will be tax-free. This amendment is applicable retrospectively from assessment year 2020-21.

Updated income tax returns

In Budget 2022, the finance minister allowed an updated income tax returns facility. Now, one can file an updated return within two years of the end of an assessment year. This facility is meant for payment of certain taxes based on income that may have been omitted from the returns filed earlier.

For instance, an individual can pay tax on foreign income, savings bank account interest or gains from equities which she missed out on disclosing while filing income tax returns.

However, one has to pay additional tax over and above the regular tax, interest and penalty. The tax applicable on updated returns is 25 percent if filed within one year of the end of the assessment year, and 50 percent if the updated return is filed 12 to 24 months from the end of the assessment year.

The additional tax calculation would include cess and surcharge on the base tax.

No more deduction under section 80EEA from April 1, 2022

To promote affordable housing, the government introduced section 80EEA effective from AY 2020-21 (FY 2019-20) with the purpose to provide additional tax deduction to homebuyers, over and above the deduction available under section 24(b) against interest payment on home loan. Under 80EEA a deduction of up to Rs 150,000 was allowed subject to satisfaction of certain conditions i.e. loan should be sanctioned during the year 2019-20, the stamp value of the house should not exceed Rs 45 lakh and the taxpayer should not own any other residential house on the date of sanction of the loan.

The period of sanction of the loan was extended from 31st March 2020 to 31st March 2021 and finally 31st March 2022 in the subsequent Finance Bills. There is no extension now granted.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.