With the Reserve Bank of India (RBI) recently cutting the repo rate, many savers are taking a fresh look at their fixed deposits (FDs). As FD rates begin to decline, conservative investors naturally turn to bonds in search of slightly higher returns. But the shift isn’t as straightforward as it appears because bonds can come with risks that FDs don’t.

The first is credit risk. Government securities are backed by sovereign guarantee, while corporate bonds depend entirely on the issuer’s financial strength. Then comes interest-rate risk, as a rise in rates can push down bond prices, particularly for longer-duration bonds.

“Another point many overlook is liquidity. Breaking an FD is usually easy, even if there’s a penalty. Selling a bond before maturity might not always fetch you a fair price,” says Shubham Gupta, CFA, co-founder of Growthvine capital. And unlike FDs, which are insured up to Rs 5 lakh per depositor under DICGC (Deposit Insurance and Credit Guarantee Corporation of India), bonds offer no such protection.

Government bonds Vs Corporate bondsIn a falling-rate cycle, investors should choose between G-Secs, state development loans (SDLs), and corporate bonds, based on their risk appetite and income needs.

G-Secs are ideal for investors seeking high safety and capital protection, as they benefit directly when yields decline. G-Secs in India generally yield between about 5.6 percent and 6.7 percent, depending on maturity and market conditions.

“SDLs offer slightly higher returns than G-Secs with a similar level of safety, making them suitable for risk-averse investors who want better yields without taking significant credit risk,” says Swapnil Aggarwal, Director, VSRK Capital. SDLs in India typically offer returns in the 7-7.5 percent range, depending on the state and maturity.

Corporate bonds trade at a premium to government bonds to compensate for their higher risk, which is known as ‘credit spread’.

During a slowing economy, credit spreads may not compress, or even widen, meaning that the corporate bonds may not outperform government bonds because the extra risk isn’t rewarded. Moreover, during such times, sticking to high quality AAA/AA issuers becomes critical.

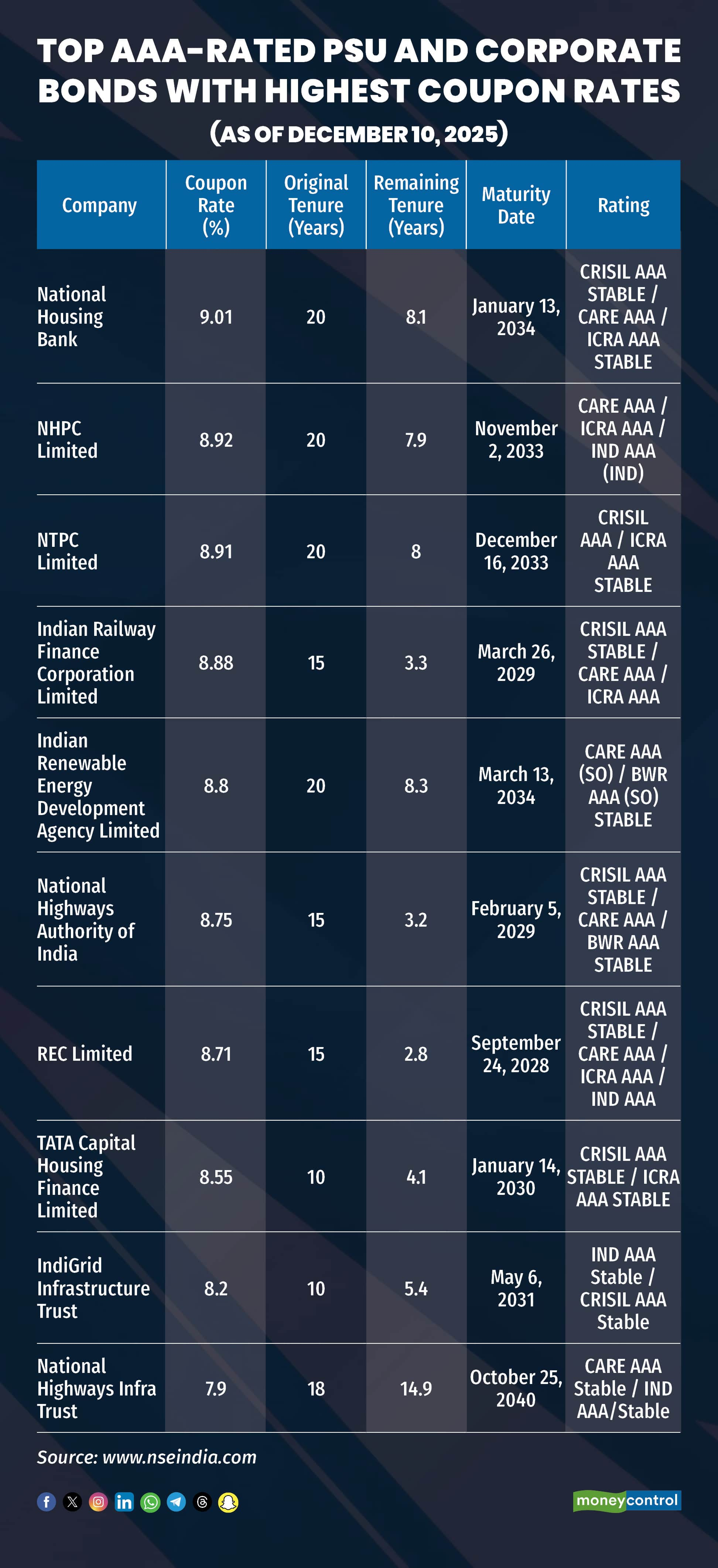

AAA corporate bonds in India have historically delivered about 7 percent to 8.5 percent yields, with total returns occasionally higher during falling interest-rate periods.

For investors looking for extra returns with controlled risk, AAA-rated bonds are a good option. BBB- rated bonds, for example, can provide returns between 9 percent-12 percent but the risks of default are higher.

For retail investors, entering the bond market directly usually requires a higher minimum investment. “Typically, direct bond investments start around Rs 1–2 lakh, and an amount closer to Rs 5 lakh is considered more practical to allow spreading investments across multiple issuers and maturity periods,” says Aggarwal.

On the other hand, debt mutual funds are far more accessible for small investors. One can begin investing through SIPs (Systematic Investment Plans) with amounts as low as Rs 500–Rs 5,000. This makes debt mutual funds a suitable option for those seeking diversification with lower initial capital.

“Direct investment in bonds can lead to reinvestment risk of the coupon and an unnecessary headache for a retail investor, while in debt mutual funds, the task is transferred to a skilled fund manager,” says Harsimran Sahni, EVP & Head - Treasury, Anand Rathi Global Finance.

Also Read: Should you invest in bonds? Key benefits, risks and SEBI warnings explained

Finding the right bond duration mix“Long-duration bonds do offer the strongest gains when yields fall, but they come with high price volatility risk, so they suit only investors who can withstand fluctuations and can hold them for several years. Meanwhile, the shorter maturities provide stability and predictable returns,” says Sahni.

Rather than choosing one over the other, investors may benefit from adopting a balanced approach by combining both long- and short-duration bonds. “This helps manage risk while still allowing participation in favourable yield movements, aligning investments with individual financial goals, risk tolerance, and investment timeframes,” says Aggarwal.

Three risks first-time bond investors must understandWhen investors move from the comfort of FDs to bonds, they are entering a market that behaves very differently. Three key risks deserve attention:

Credit Risk: Government securities don’t carry this risk, but corporate bonds carry a credit risk. “Corporate bonds rely entirely on the issuer’s financial strength. If the company’s health weakens or it defaults, returns can be hit, including your principal. Hence, the extra yield offered isn’t “free”” says Gupta.

Interest-Rate Risk: Bond prices move in the opposite direction of interest rates. If rates rise, the value of your bond can fall, even if coupons are paid on time. Longer-duration bonds feel this volatility more sharply.

Liquidity Risk: Unlike FDs, where breaking the deposit is straightforward, selling a bond early may not always get you a fair price. Secondary-market trading can be patchy, especially for lower-rated or smaller-issue bonds.

“It is better to invest in bonds with a ‘Hold-to-maturity’ mindset to offset the impact of interest rate and liquidity risk,” says Gupta.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.