Thirty-three-year-old Manoj Kalwar of Mumbai feels the challenge of having become self-employed since April this year. While working as a salaried employee earlier, he was a project manager in an information technology firm for eight years. But he now follows his passion for travel. So, he has turned a treks and tours operator.

Says Manoj, “In last three months, I have observed that monthly expenses remained similar to my salaried years, but income inflow from treks and tours conducted were erratic. This is because the business is seasonal, trekking equipment is costly and there is competition from established players in the field. Thus, I feel the need to plan my finances differently from being salaried earlier.” Being self-employed, statutory employee benefits will not be available to him. So, he needs to plan better than a salaried person to secure his family’s future appropriately in terms of insurance and investments.

Manoj’s case is not unique. India has the world’s second largest freelance workforce after the United States, according to a Truelancer freelancer India survey report of 2018. The report further states that, at present, 60 per cent of the freelancers in India are millennials, i.e., under 30 years of age. They have a desire to establish themselves in the field of their interest.

So, here are some steps that you need to take for your financial well-being, if you decide to be on your own as a self-employed person.

Build a contingency fundFor self-employed professionals and freelancers, income is irregular. A contingency fund is the money set aside to cover unexpected situations or losses in business, usually supplementing a contingency reserve. The purpose of the fund is to improve your financial security by creating a safety net of funds that can be used to meet emergency expenses.

Gaurav Mashruwala, a Sebi-registered investment adviser says, “You should have sufficient money in your contingency fund to cover three to four months of living expenses. In case the monthly income is highly volatile, then increase it to up to six months.” All the mandatory expenses in your family should be a part of the contingency corpus to be built. For instance, grocery bills, medical bills, equated monthly installment (EMIs), insurance premiums, school fees, etc. should be considered.

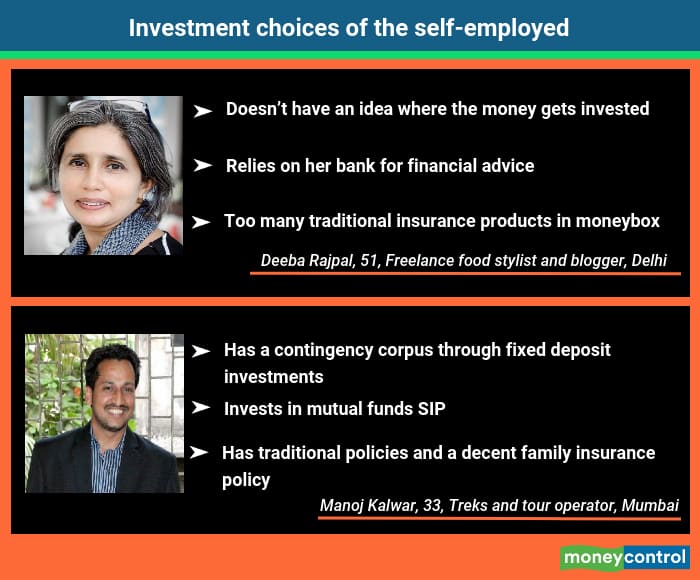

Manoj had built a contingency corpus of Rs 4 lakh through fixed deposit investments while being employed. He took extra part-time work on weekends and managed to save an additional 10-15 per cent from his monthly income in the last 18 months to build this corpus.

Being self-employed, Manoj’s income is now dependent on tours conducted in a month, advances received and final payments from customers. So, for any uncertainty, he has built this contingency corpus.

Maintain a monthly budgeting sheet and cash-flow statement.

Buy term and health coversSelf-employed professionals and freelancers must buy a health cover because they won’t have any insurance from their previous employers anymore. Abhishek Bondia, the co-founder and principal officer of SecureNow says, “The amount of health cover for the family should be equal to one year of annual income. For a term plan, taking ten times the annual income from freelancing or self-employment is recommended.”

Deeba Rajpal, 51, a freelance food stylist and blogger residing in Delhi has too many traditional insurance products in her portfolio and pays an annual premium of Rs 5 lakh. Bondia suggests, surrendering such traditional plans as they carry very high charges and recommends that she opt for a term plan.

It is important to have some additional health cover of your own at an early age and not be dependent entirely on your office-provided cover during your employment years. If at an advanced age you become self-employed, you would then already have a separate cover. Buying your own cover at 51 like Deeba could prove to be expensive.

Apart from health insurance, self-employed people should also buy a critical illness insurance plan. Why? As they are working independently, if some ailment were to occur to them, they won’t have any other income sources.

Use the systematic transfer plan route to investDeeba manages to save 60 percent (approximately) of her annual income from assignments, but relies entirely on the advice from her bank’s wealth manager for investments. She doesn’t have any idea on the investment strategy that the wealth manager follows and or the schemes in which her money gets invested in annually from her account. Says Deeba, “The investment portfolio just gave compound returns of 7 percent in the last two years. It seems the wealth manager at the bank has reshuffled my investment portfolio many a times to earn commission income.” It’s important you appoint a SEBI registered investment adviser or a trusted independent financial distributor (preferably, through a recommendation) to advice on investments and manage your portfolio instead of an adviser churning your portfolio to earn income from commission.

Amol Joshi, founder of financial advisory firm Plan Rupee Investment Services says, “A freelancer has the flexibility with work; however, the income tends to be volatile and sporadic, which is difficult to tackle while preparing a financial plan.”

As income is erratic for the self-employed, experts recommend opting for a quarterly systematic investment plan (SIP) in mutual funds, if they are unable to commit to monthly SIP like salaried investors. Mashruwala says, “You can even start investing in a mutual fund scheme with a small amounts of Rs 500 or Rs 1,000 SIP and invest lump-sum amounts in the schemes when you receive money on completion of a certain assignment.”

Alternatively, you can deploy the entire or 20-25 per cent of the lump-sum amount in a liquid mutual fund scheme and from there the amount can be switched out periodically to your chosen equity funds by initiating a systematic transfer plan. With this investment strategy, the objective of investing a lump-sum amount and market averaging, both are achieved.

You should invest in diversified mutual funds and equity linked savings schemes for tax planning. Avoid investing in credit risk, thematic and sector funds.

Separate business and personal accountsMost self-employed people only have a savings account in a bank and do not hold a current account to look after business expenses. So, whatever income is earned is either consumed for personal or business expenses. Shilpa Wagh, Chief Financial Coach at Wagh Financials says, “There needs to be a proper bifurcation of the income you earn. Track your household expenses and know how much is actually getting reinvested into the business.” Such a practice will help you to stay organised with your financials.

Tarun Birani, founder and CEO of TBNG Capital Advisors says, “It’s a good habit to pay yourself a regular salary. So, transfer your personal income (salary) from your business every month. Your lifestyle and other monthly expenses should be limited to this income you get home every month.”

For instance, Manoj operates two separate accounts for business and savings. At the start of the month, he transfers Rs 60,000 to his savings account as salary to himself from his current account. This amount takes care of his personal / family expenses and investments for family goals. In the business account, he revolves the amount for booking future tours, monthly business expenses and to pay salaries to his team. This way, he stays organised with his financials and is able to invest Rs 20,000 as SIP in mutual fund schemes for future goals of the family.

However, if you don’t separate business and personal accounts promptly, you might have to face the consequences. For instance, you mortgage your home (personal property) to finance a working capital loan for the company in which you are owner. If you are unable to repay the borrowed money to the bank in time, the bank could seize your home (a personal property) as it’s mortgaged with them.

Invest for your retirementBeing self-employed or a freelancer, you don’t have the employee provident fund (EPF) to build your retirement corpus as a salaried person would. Also, you are not eligible for gratuity benefits on retirement. So, it’s important to invest for your retirement corpus yourself.

Khyati Mashru, founder and chief financial coach, Plantrich Consultancy LLP says, “Investing in the public provident fund and the national pension system (NPS), as they have longer lock-in periods.” In PPF, there is a lock-in period of 15 years and in the NPS the investment remains locked-in till the age of 60. From the NPS, at 60, you can withdraw only 60 per cent of the contribution, as the balance 40 per cent needs to be invested in an annuity plan. Ankit Agarwal, MD, Alankit Limited says, “For young self-employed professionals, NPS is a profitable option. Apart from tax saving and retirement benefits, it also allows you to invest wisely and earn higher returns. This is the right time to consider NPS to build a substantial retirement corpus while enjoying excellent tax benefits.”

However, if have enough time to retire and a relatively higher risk appetite, then equity mutual funds are another good option. The fund manager diversifies investments across market caps and sectors in a bid to maximise gains for investors. By investing in ELSS (equity linked savings schemes), you can claim tax benefit up to Rs 1.5 lakh u/s 80C of the Income Tax Act.

Avoid investing in credit risk funds because these are the schemes that invest at least 65 per cent of their corpus in securities that are rated AA and below. They take higher credit risk by investing in lower rated papers.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!