Rising inflation is back in focus, shaping expectations around the Reserve Bank of India’s next monetary policy decision. According to an ICRA report, WPI inflation is expected to rise to 3.2 percent in March 2026, which would mark a 21‑month high, amid higher prices of crude oil, natural gas, and edible oils linked to the ongoing West Asia conflict.

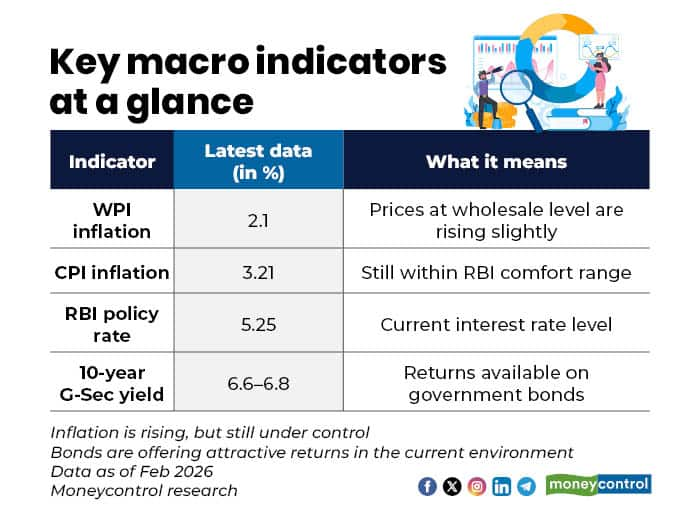

WPI inflation rose to an 11-month high of 2.1 percent in February 2026, compared with 1.8 percent in January.

With the Monetary Policy Committee (MPC) meeting approaching in April, bond investors are watching closely for signals on interest rates, liquidity, and the central bank’s broader stance. Inflation trends play a direct role in determining yields, and even small policy shifts can move bond prices sharply.

As we approach the upcoming RBI MPC meeting, the fixed-income landscape is shifting. With interest rates currently at 5.25 percent and a "neutral" stance in place, many investors are wondering how to position their bond portfolios.

Bond portfolio strategy

Some experts believe inflation may not force immediate rate hikes. "India’s CPI at 3.21 percent still gives the RBI enough room within its 4 percent plus-minus 2 percent framework, and any inflation led by oil spikes may be short-term. Our view remains that rates would actually stay lower for longer because growth is the larger priority," said Vishal Goenka, Co-Founder of Indiabonds.com.

Today, the 10-year government bond yield in the 6.6-6.8 percent range offers a relatively steady income stream, even when equity markets are volatile. Experts suggest that investors adopt a structured approach to manage interest rate risks in the current environment.

"For a well-rounded portfolio, consider a 'Laddering Strategy.' By spreading investments across bonds with different maturity dates (e.g., 1, 3, and 5 years), you can reinvest the money from maturing bonds into new ones at higher rates if the RBI continues to tighten policy. This helps mitigate interest rate risk while keeping your portfolio's yield-to-maturity (YTM) healthy," said Anup Bhaiya, Founder of Money Honey Financial Services Ltd.

From an investor’s perspective, bonds are also less about high returns and more about predictability. "In the current environment, locking into high-quality bonds yielding around 6.7–7 percent can be a sensible move, especially if you’re looking for steady income. Even if interest rates move slightly higher, holding these bonds to maturity ensures you still receive your expected returns," said Karan Rijhsinghani, Director & Head – Product & Advisory, Atom Privé Financial Services.

Moreover, bonds can help cushion portfolios against market volatility. Corporate bonds, particularly high-yielding ones, do not always react as sharply to short-term inflation moves. That is why bonds play an important role in investors’ portfolios, said Goenka.

How do bond investments work?

The best time to lock in bond investments is when rates are high or peaking, rather than at their lowest. When the RBI raises interest rates, newly issued bonds offer higher coupons (interest payments).

However, there is a catch. Bond prices and interest rates have an inverse relationship, which means that when market interest rates rise, the price of existing bonds falls. Therefore, if you believe rates are near their peak, buying "long-duration" bonds allows you to lock in high yields. If rates eventually fall, your bond’s value will increase, providing capital appreciation on top of interest.

Imagine you buy a 10-year Government Bond (G-Sec) today for Rs 1,000 with a fixed coupon of 6 percent. If next month, the RBI raises rates, and new bonds start offering 7 percent, then no one will want to buy your 6 percent bond for Rs 1,000 when they can get 7 percent elsewhere. To sell your bond, you would have to drop your price to, say, Rs 930.

"If you hold to maturity, you still get your 6 percent and your Rs 1,000 back. But if you need to sell early in a rising-rate environment, you may incur a capital loss, said Bhaiya.

How inflation impacts bonds

Inflation is the "silent enemy" of the fixed-income investor. It impacts bonds in two primary ways:

"If inflation rises, it eats into real returns and can also push bond yields up, which impacts prices in the short term. That’s why focusing on the right duration and sticking to high-quality issuers becomes important," said Rijhsinghani.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.