While a moratorium is not a new concept in the banking space, many home loan borrowers are not well-acquainted with it. This has resulted in a bit of chaos. Some banks and housing finance companies received a flurry of queries from customers wishing to take the moratorium soon after the Reserve Bank of India’s (RBI’s) announcement. However, many are not aware of the impact of RBI’s statement that interest would continue to accrue during the period of the moratorium.

If you intend to opt for moratorium, get rid of these misconceptions before you initiate the process:

‘The loan tenure will be extended by just three months’No. The moratorium (assuming you availed of one in March) allows you to pause EMI payments for three months. But it does not mean that your loan tenure will get extended by an equal number of months. This is because the RBI has stated that interest will continue to accrue during the period. It is not a waiver, so those who are not facing financial upheaval due to the COVID-19 pandemic and the lockdown across the country are better off not opting for it.

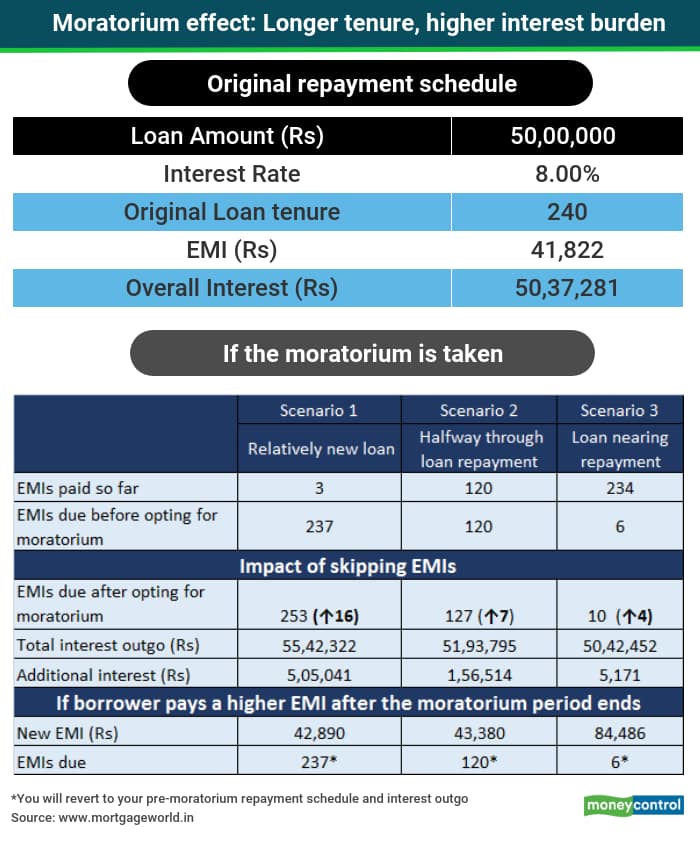

The detailed FAQs released by banks make it clear that the interest during the period will be compounded. It will be added to your outstanding loan amount and the entire sum will attract the interest rate applicable, thus increasing the interest burden for you over the loan tenure. This will result in an extension of your loan tenure to well beyond the imagined three months. For example (see table), in scenario 2, the remaining tenure increases from 120 months to 127 months, which means you will have to pay seven more EMIs. So, sign up for the moratorium only after you have exhausted all alternatives for raising funds.

‘The interest burden won’t be high, as only three EMIs are deferred’Again, it’s the principle of compounding at work, along with the long tenures of home loans. In addition, the age of your loan also counts – in the initial years of repayment, the interest component in the equated monthly instalment (EMI) is significantly higher than the principal amount. Towards the end of repayment tenure, it’s the principal amount that dominates the EMI, with the interest component making up a much smaller portion.

As the example illustrates (see table), for a 20-year loan taken three months ago, the increase in interest due to a moratorium will be as high as Rs 5.05 lakh. “The balance tenure will increase from 237 months to 253 months. “This means you will have to pay 16 more EMIs compared to your original schedule,” explains Vipul Patel, Founder, Mortgageworld.in.

On the other hand, if your loan is set to be repaid within six months, opting for moratorium will mean a higher interest outgo of just over Rs 5,000.

You do stand to benefit. For one, if you are facing a temporary fund crunch after the nationwide lockdown due to COVID-19, you will get some breathing space. The instalments falling due between March 1 and May 31, 2020 will be eligible for the moratorium. You will not have to worry about getting calls from banks or recovery agents asking you to pay up the dues. Ordinarily, you would have been treated as a defaulter for not meeting your EMI commitments, which will not be the case now. Missing EMIs affects your credit report and score adversely, thus reducing your chances of securing a loan in the future. The moratorium ensures that borrowers do not have to be concerned about such challenges. You can, instead, focus on putting your finances in order and working your way out of the crisis during the period.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.