Understanding the difference between financial planning before and after retirement is extremely critical—more so for those planning to retire in the next 10 years.

For simplicity, let’s refer to Financial Planning before Retirement as FP-Before and Financial Planning after Retirement as FP-After in this article.

FP-Before focuses on the accumulation phase—the years before retirement. A good financial plan (before retirement) will make sure that you set a realistic retirement corpus target. It will also push you to invest enough to reach the target retirement corpus at the right time in the future. It goes without saying that in the years before retirement, there are other goals such as children’s education and house purchase too.

So, a good financial plan will take care of all these along with the goal of retirement. FP-After, on the other hand, focuses on how your existing retirement corpus will generate an income stream during your retirement years and how your expenses will be taken care of. It is, as mentioned earlier too, aimed at ensuring you do not run out of money before your years run out.

Sufficient retirement corpusIf you talk to any 60-plus person who isn’t ultra-rich, has retired and is living on income from retirement corpus, his/her concern would be, “Will my money last?”

Let’s take a small example to understand all this.

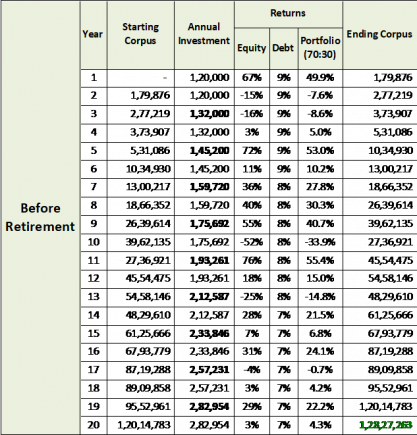

Suppose, at the age of 40, you decide (after procrastinating for several years) that you should begin saving for retirement seriously.

So you start with a small Rs 10,000 monthly investment in a 70:30 Equity:Debt portfolio. You increase the monthly savings amount by 10 per cent every second year. So you put in Rs 1.2 lakh each in first two years, followed by Rs 1.32 lakh in the third and fourth years, Rs 1.45 lakh in the fifth and sixth years and so on. You do this for the next 20 years till your retirement at 60. Assume the returns you get on equity are the same as the actual annual Nifty 50 returns between 1999 and 2018. Debt returns have been assumed to start from 9 per cent and taper down to 7 per cent.

After 20 years of accumulation (without any withdrawals), this is the result:

You retire with a corpus of Rs 1.28 crore. Is it enough? Let’s see.

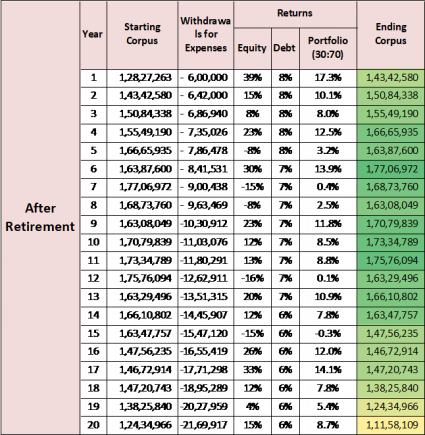

To run the post-retirement scenario (from age 60 to 80), it is assumed that the starting expenses are Rs 50,000 a month (Rs 6 lakh per annum). And this increases by 7 per cent inflation every year. So, it’s Rs 6.42 lakh in the second year, followed by Rs 6.87 lakh in the subsequent year next and so on.

To generate an income for such levels of annual costs, the retirement corpus accumulated earlier (Rs 1.28 Cr) is deployed in a 30:70 Equity:Debt conservative portfolio. Equity returns fluctuate every year and debt returns start from 8 per cent and go down to 6 per cent. Here is the result:

The portfolio survives 20 years of retirement. Good for you.

Return assumptions importantIf you do a more granular examination of the table above, the equity returns achieved in the first 3 years are 39 per cent, 15 per cent and 8 per cent. It seems like you retired in a good market. But what if you didn’t? That is, what if you retired in a bad bear market where the first three years delivered -10 per cent each? What would have happened then?

The money runs out before you turn 80!

This is, as you will agree, a financial disaster for a 79-year old who is going to live for at least a few more years if health permits.

And this is exactly what concerns financial planning after retirement. It tries to ensure that your corpus does not run out due to poor returns or high expenses.

Before retirement, you should not withdraw from retirement portfolio (but rebalance). So, a string of bad years doesn’t affect your portfolio that much, as you get to average down the cost of your investments, if nothing else. But after retirement, you have to withdraw from your portfolio to meet your expenses. And if this withdrawal happens in bad years, the corpus would deplete very quickly as there are the twin blows of withdrawal and market-related decline to the portfolio.

(The writer is the founder of StableInvestor.com)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.