In the past 2-3 years, exchange-traded funds or ETFs have become popular. More so in the large-cap category because it has become increasingly difficult for large-cap funds to beat their benchmarks. And ETFs charge very low expense ratios. But did you know that the actual cost of owning an ETF is much higher?

ETFs require demat accountsSince ETFs are traded on the stock exchange, you need to have a demat account. Most demat accounts charge Rs 300-450 per annum. For active investors or traders, sometimes, these charges are waived.

Further, there are brokerage charges as well. Most brokers charge between Nil-0.5 percent for every trade. Along with brokerage, you may have to pay a slew of other charges, including GST.

That’s not all. Many times, ETFs suffer from low liquidity. There might not be enough buyers for your ETF units when you wish to sell them. Or, you might not be able to buy at the market price. So, in the first case, you may have to settle for a slightly lower price and in the latter case, a higher price. This difference is called the bid-offer spread or the impact cost. For instance, the impact cost for Nippon India Nifty BeES on NSE was 0.03 percent (March 11, 2021).

“The total expense ratio is not the only cost an investor of an ETF incurs. What we need to look at is the Total Cost Ownership (TCO), which includes basic expense ratio and other costs such as brokerage, spread, NSDL charges in demat account, etc”, says Anil Ghelani, SVP & Head-Passive Investments and Products, DSP Investment Managers.

While the capital market regulator, Securities and Exchange Board of India (SEBI) has fixed an upper limit of 2.5 percent for actively-managed equity funds, index schemes and ETFs can charge a maximum base expense ratio of one percent. In addition to that, mutual funds can charge 50-70 basis points under various sub-heads as prescribed by the SEBI.

In reality, they charge much lower rates. The average expense ratio of the regular plans of active large-cap funds as of February 2021 was 2.25 per cent, and that of the regular plans of index funds and ETFs was only 0.8 and 0.2 per cent, respectively.

The ETF’s tracking error is usually lower than that of an index fund as it tracks the index more closely. And its automated structure is also why its cost structure is even lower than an index fund.

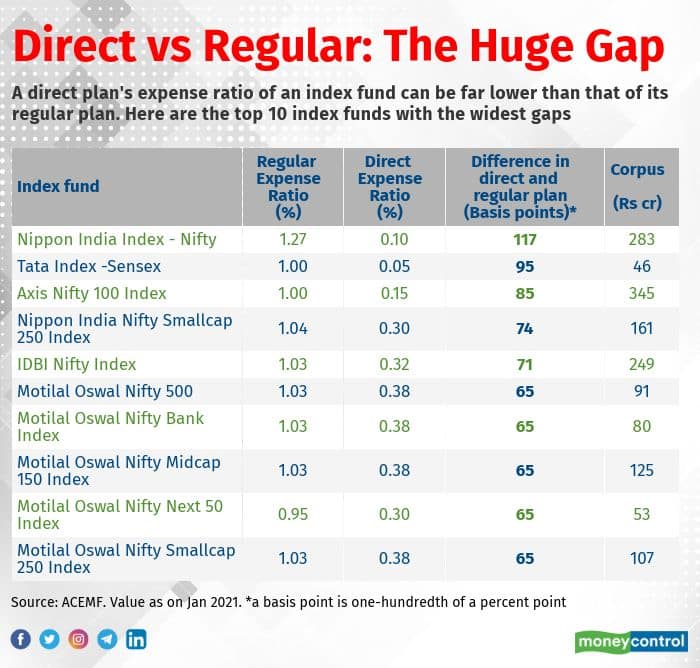

Direct plans of index funds are better than ETFsInterestingly, the direct plans of the index funds score over the regular plans of those index funds as well as the ETFs on the cost front. Direct plans do not come embedded with distribution cost. Funds are bought directly from the fund house, by avoiding distributors.

For index funds tracking the Nifty 50 index, the expense ratios of regular plans (as of February 2021) were 0.14-1.27 percent, while for direct plans, the figures were 0.05-0.91 percent.

On the other hand, the expense ratios of ETFs tracking the Nifty 50 index were 0.05-0.16 percent. If you calculate the TCO (total cost of ownership) for these ETFs, then it would increase to 0.47-0.58 percent.

Chetan Gill, a Chandigarh-based mutual fund distributor, says that passive investment is for all those who wish to get index-based return without any additional active fund manager risk.

ETFs these days offer you a lot more choices. But unless fund houses appoint and nurture more market makers to create liquidity, direct plans of index schemes may well hold the edge over ETFs over the long term.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.