Sailesh Raj Bhan, who took over as the chief investment officer (CIO) – Equity, at Nippon Life India Asset Management, is no stranger to the fund house. He has spent over 16 years at the fund house, India’s fourth largest, with assets worth Rs 2.97 trillion under management. Bhan, who has over 27 years’ experience in the Indian equity market, started out at Nippon MF as an equity fund manager in 2006.

So far, Bhan has been managing multiple flagship funds, namely, Nippon India Large Cap Fund, Nippon India Multi Cap Fund and Nippon India Pharma Fund, for more than 15 years.

As far as investments are concerned, Bhan’s mantra is simple: Keep it simple.

It’s the beginning of a new year and that’s always a good time to start investing. But equity markets are on a high. The S&P BSE Sensex has been at around 60,000 since November 2022. Is this a good time for a novice investor to enter the equity markets?It is not easy to time the equity market. An investor generally targets equities

for medium- to long-term goals. So, it is advisable to enter the markets in a staggered manner; via step-by-step investments or through a systematic investment plan (SIP). That’s the right approach to gradually increase allocation.

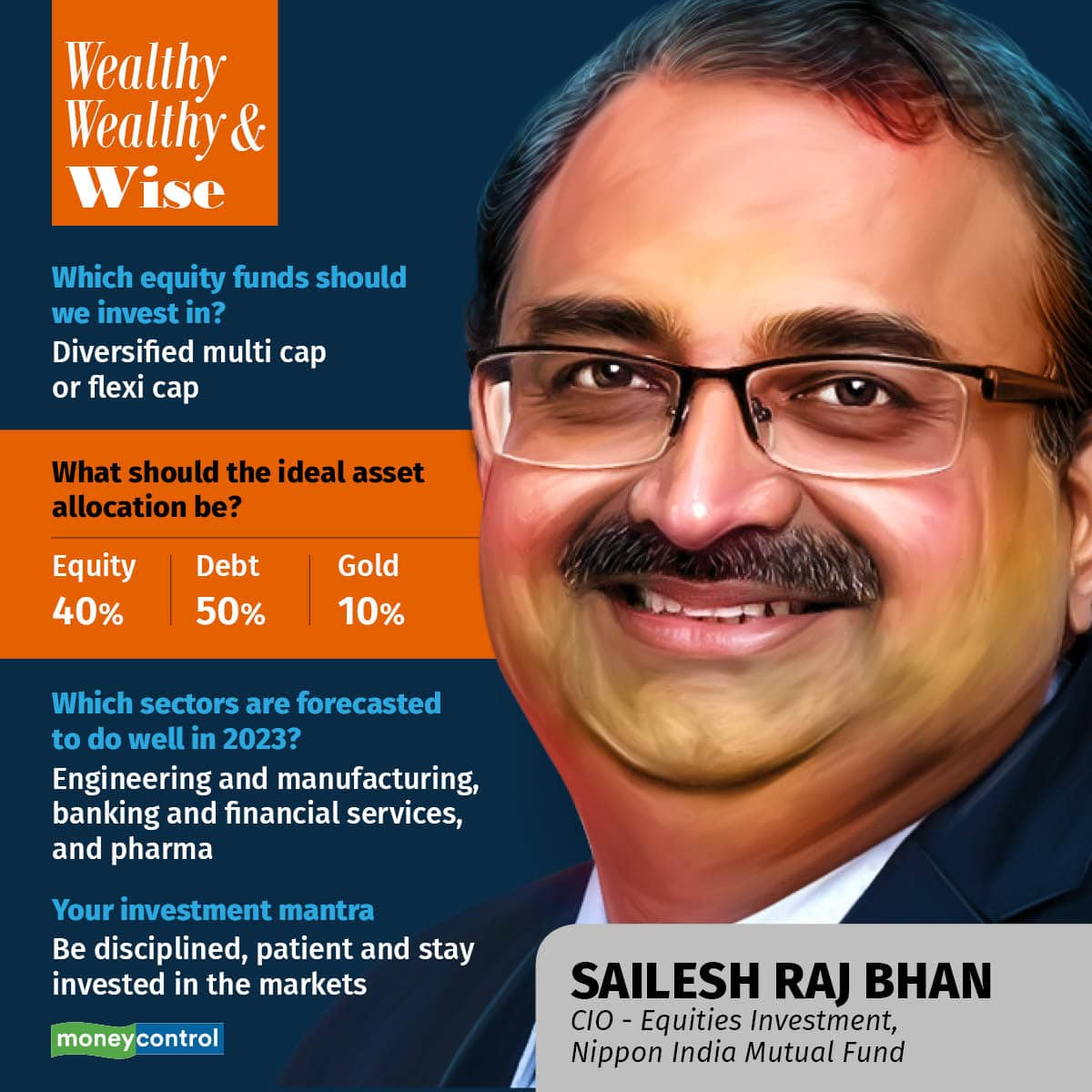

I have Rs 10 lakh to invest today. What do you recommend? I know asset allocation is specific to individuals, but give us your broad guidance.Just stick to two asset classes; debt and equity. You can diversify a bit in gold. But that’s about it. In normal market conditions, I would suggest a 50-50 allocation to equity and debt. But given the high valuations right now, I would recommend 40 percent in equity, 50 percent in debt and 10 percent in gold, as a broad allocation percentage.

Which category of equity funds would you recommend at this time?Stick to diversified funds. A flexi-cap fund or multi-cap fund will give you exposure across all sectors.

Which sector(s) of the Indian economy are expected to perform well and which ones might face a setback this year?In terms of earnings growth, the engineering and manufacturing, and banking and financial services sectors are well-positioned. After a disastrous show in 2020 (a loss of around 9 percent), the pharmaceutical sector might also see a change in fortunes on account of better corporate earnings.

Automobiles, information technology (IT) and consumer staples on the other hand can face a setback. It is expected that the increased demand for automobiles seen during the Covid-19 work-from-home years, when social distancing was necessary, might just reverse. There could be a slowdown here. The IT sector is seeing some terrible layoffs. And consumer staples might face turbulence due to existing high valuations.

You have been managing the Nippon Pharma Fund since March 2005, since its inception. How do you think an investor should approach a sector as complex as this?The best way to invest in a sectoral fund is to look at how much exposure the sector has in a diversified index, like the Nifty 50 index or the S&P BSE Sensex. If you are bullish on the sector, you can invest a bit more — say, 4-5 percent of your portfolio — in the sector, so that your overall effective exposure goes up to around 10-11 percent.

Remember, don’t invest in multiple sector funds. You might think that you are bullish on multiple sectors, but investing in so many sectors would just replicate a diversified equity fund.

How frequently should you change your asset allocation? If my equity allocation has gone up in the recent bull run, should I sell my equities now?Rebalancing every month will be a deterrent to your portfolio, as one needs to be patient with investments. Rebalancing once a year is a reasonable time frame, or if the equity market witnesses a significant upside or downside. The rebalancing should always keep the volatility and risk of the portfolio under control.

Equities are strictly meant for the long-term. However, equities can give you a dose of returns in 18 months or maybe more than three years. Therefore, hold on to equities for at least three years. But if the markets shoot up very sharply and your asset allocation gets distorted as a result, take some money off the table (book profits) and bring your asset allocation back in line. This could mean selling equities before three years, as a means to rebalance.

Between debt and equity, which of the two asset classes will perform better in 2023, according to you?That’s difficult to say. But debt has come into the limelight after a very long time because of the interest rate cycle we have reached. It is not that one is more attractive than the other, at the moment. But if economic conditions turn favourable again, then equities might do better. Till then it is important to maintain a balance between the two.

Mutual funds have started to launch new fund offers (NFO). Should an investor even look at one, when there are so many existing funds around?If there are alternatives that have a longer track record, then having those in your portfolio is better than going for these launches.

What are the global factors you think may pose a threat to the Indian equity market?The US being in a difficult spot because of the (Russia-Ukraine) war, inflation and recession is a big threat. China’s recovery, global interest rates remaining high, and fluctuating commodity prices are also threats to the Indian economy.

What is your personal asset allocation pattern?As a rough estimate, I have 60 percent allocation to equity and 40 percent to debt.

How do you achieve your fixed-income exposure? Are you invested in long-duration funds?I am not invested in long-duration funds because that would increase my risk. Interest-rate changes make debt funds volatile. For the fixed income part of my portfolio, I stick to fixed deposits and tax saving bonds.

What are your investment mantras?- Practice discipline

- Enter the markets early and spend more time invested

- Be patient

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.