Krishna Karwa Moneycontrol Research

Highlights: - Lack of clarity on accounting methodologies and elevated valuations could restrict re-rating in the near-term

- Top-line growth will be driven by network expansion and new products

- Adoption of asset-light manufacturing and retailing should have a positive rub-off on margins

- Competition from foreign brands is a key risk

--------------------------------------------------

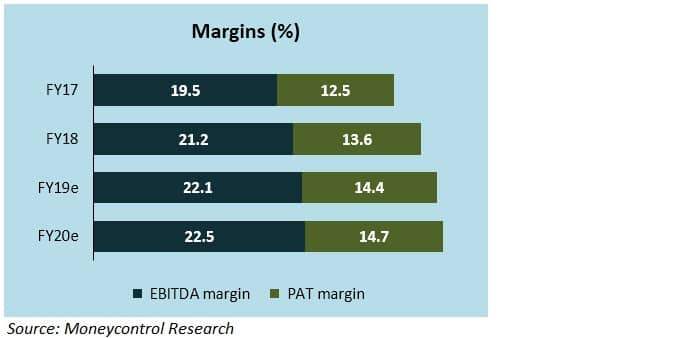

Page Industries reported a visible improvement in its Q3 performance sequentially and year-on-year (YoY). Going forward, network augmentation and new product lines should drive revenue growth. Margin accretion would depend on low capex intensity and fewer discount days.

The stock is slated to go through a rough patch until issues pertaining to financial reporting are taken care of by the management.

Page Industries has the exclusive right to manufacture, distribute and sell innerwear cum leisurewear products under the ‘Jockey’ brand in India, Sri Lanka, Maldives, Bangladesh, Nepal and UAE. It is also a licensed retailer of ‘Speedo’ swimwear products and accessories in India.

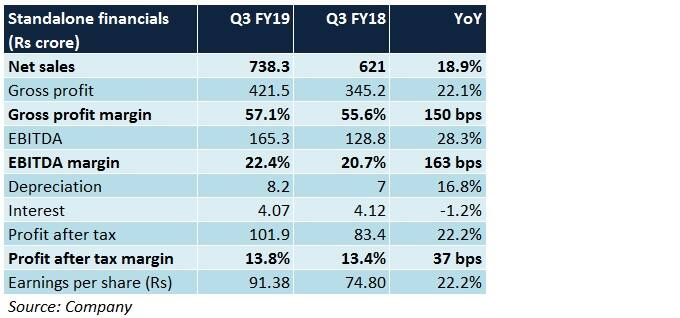

Q3 review Positives - Optically, revenue growth was strong YoY because of festive sales

- Operating margins expanded on account of sale of high-margin thermal wear products

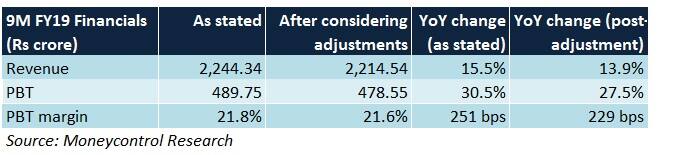

Negatives - For 9MFY19, Rs 29.8 crore in revenue and Rs 11.2 crore in PBT are attributable to accounting adjustments only. If we exclude the impact of these, the 9-month numbers would be as follows:-

- Lack of clarity regarding the performance of the relatively smaller segments (women’s wear, children wear, girls wear, active wear) raises questions as to whether the historically robust growth observed in menswear can be replicated in the other areas as well

Observations

Exclusive brand outlets (EBO) to drive growth To capitalise on Jockey’s brand appeal and explore cross-selling opportunities, the management aims to double the EBO count over the next two years (from the 500-550 mark at present).

Other retail formats also being strengthened To improve brand visibility, the company offers most of its products on e-commerce marketplaces. It is also investing heavily in its own website, besides bolstering presence across multi-brand outlets and departmental stores.

Brand extension gaining momentum The company is gradually transitioning itself from being a men-centric brand to a multi-gender, multi-category one. Product launches will be undertaken in the women’s, sportswear and children’s space at regular intervals.

Impetus towards an asset-light business to continue By the end of FY21, nearly 45-50 percent of the manufacturing processes would be outsourced (from 30 percent at the moment). In the retailing department as well, most of the new stores may be franchise-run.

No steep discounts offered Unlike its peers, the company rarely resorts to any form of steep discounting or EOSS (end-of-season-sale) schemes. Consequently, there should not be any significant strain on margins.

Outlook Despite good Q3 results, the stock corrected due to two reasons -- non-disclosure of segment numbers and accounting revisions (which artificially inflate the financials).

For a company that trades at a steep premium to its competitors, ambiguities associated with growth across segments make it hard for investors to determine if the heady valuations can be sustainable.

While we are enthused by the long-term prospects and market leadership of the company, given the ongoing market volatility and above-mentioned concerns, there is a dim chance of a major re-rating in the near future.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed hereDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.