Tata Consultancy Services(TCS) has been one of the biggest outperformers this year and this performance was once again well justified with a strong quarterly show. Q2 FY19 turned out to be an all-round satisfactory quarter with the company officially clocking double-digit revenue growth both in constant currency as well as in US dollar. The traction in digital was the key driver of this performance. Margin improved on the back of efficiency gains and currency. Most vertical and geographies grew handsomely. And finally, the deal pipeline makes the company confident of sustaining the momentum.

In the past one quarter, the stock had rallied 6.7% thereby outperforming not only the Nifty (-4%) but also the IT Index (2.6%). While a further multiple-rerating is not on the cards and the valuation at 21x FY20e earnings capture the positives; in a turbulent market environment, investors should look to add TCS for high teen returns that should closely mimic earnings growth in the coming years.

Result at a glance

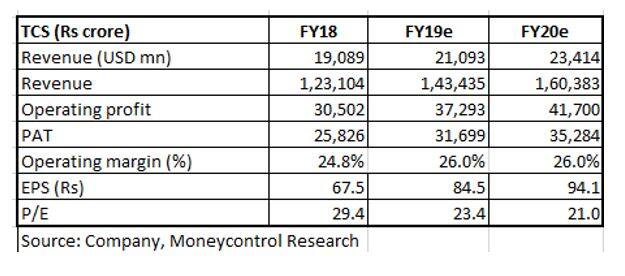

For the quarter ended September 2018, TCS reported US dollar revenues of 5215 mn, up 3.2 percent quarter-on-quarter, with revenues in constant currency growing by 3.7 percent. The year-on-year growth in revenue in US dollar was 10 percent and in constant currency 11.5 percent, thereby marking the company’s re-entry into the long-awaited double-digit growth club.

Geographically, the bright spots for TCS were continental Europe, UK and Asia Pacific. It was heartening to see the biggest market North America with a share of over 50 percent showing a strong growth of over 8 percent as well.

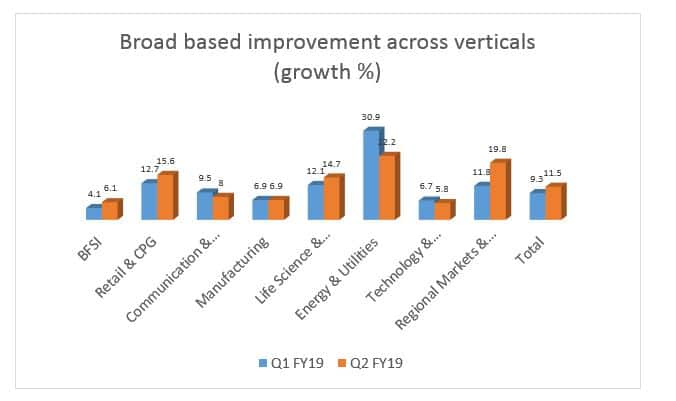

Vertical-wise, BFSI, further consolidated its position with a growth of over 6 percent. BFSI platform also showed strong acceleration. Retail, life sciences and energy continued their strength.

TCS reported significant sequential improvement in operating margin that took it to its stated margin band. The reported margin improvement of 150 basis points sequentially to 26.5 percent was aided by efficiency gains to the tune of 30 basis points whereas the remaining 120 basis points was contributed from the depreciation of the Indian currency.

The strong growth in digital revenue was one of the key highlights of the quarter. In Q2 FY19, the digital business grew by 60 percent year on year and formed 28% of the total revenue. The growth in digital is much higher than the overall growth of the company at 11.5 percent. Management commentary reiterated that digital adoption is becoming a norm now and the industry is witnessing the second wave whereby enterprises are taking digital to the core.

Deal sizes in digital are getting larger and pricing remains stable that should lend stability to margins. With rupee depreciation giving some headroom for margin expansion, TCS will continue to invest in new technology without compromising margin in the near term.

FY19 & beyond – look promisingThe deal pipeline remains healthy. The deal wins in Q2 FY19 was of similar order as the previous quarter at $4.9 bn with 49 percent contributed from North America. Amongst the leading verticals, BFSI contributed 31 percent and retail 14 percent.

TCS added clients across sizes but what’s worth taking note of is the addition of 4 clients in the $100 mn plus bucket.

Companies across verticals are engaging with TCS for their transformation programs. Given the strong outlook, the management commentary did suggest that sustaining the current momentum of double-digit growth shouldn’t be a challenge, going forward.

Strong hiring points to better daysHiring also corroborated this outlook. The company added 10,227 people in the quarter – the highest net addition in the past twelve quarters. In a first of its kind, TCS has started a “TCS National Qualifier Test” to tap entry-level talent across the country. This will enable the company to hire resources closer to demand thereby lowering the cost of keeping a large bench and could impact utilization positively, going forward.

The healthy payoutTCS now adopts a well- defined capital return policy of 80-100 percent of free cash flow. Should it adopt a similar payout policy in FY19 as well (already done a buyback worth Rs 16,000 crore and an interim dividend of Rs 4 per share), on a pre-tax basis, this works out to a yield of close to 4 percent.

While the payout limits the downside, rupee depreciation in a volatile global environment could act as a tailwind. Investors should, therefore accumulate TCS as a core holding in the large cap IT space that could easily deliver mid-teens returns in a choppy market.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!