Jitendra Kumar Gupta Moneycontrol Research

Stringent working capital requirements and resultant financial leverage have led many engineering companies to collapse during the last industry downcycle during 2013-14. The ones that survived have most likely practiced the time tested wisdom of using capital efficiently without jeopardising the balance sheet.

Salasar Techno Engineering, incorporated in 2001, is one such company. It has demonstrated such qualities and managed its balance sheet well in different cycles.

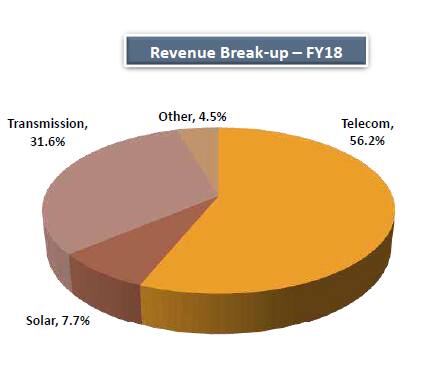

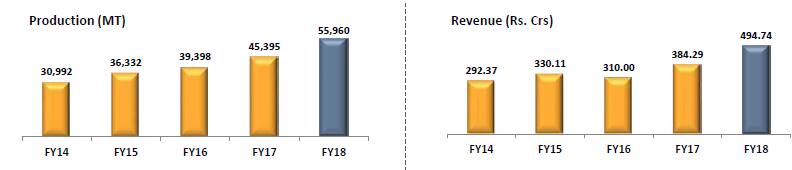

An efficient player Salasar, which engineers and fabricates steel structures used by telecom, power transmission and solar companies, has grown its businesses at 14 percent annually during FY14-18.

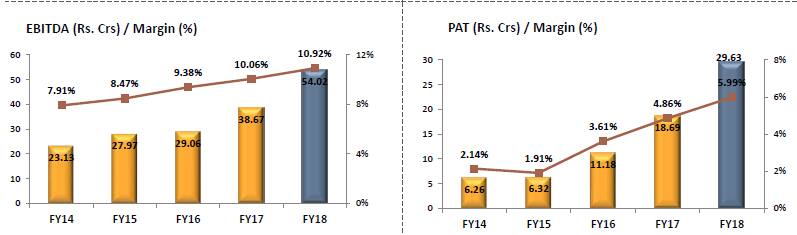

During this period, profits have grown at a faster rate (47.5 percent) annually, led by consistent margin improvement because of operating leverage, cost reduction and integration of its operations.

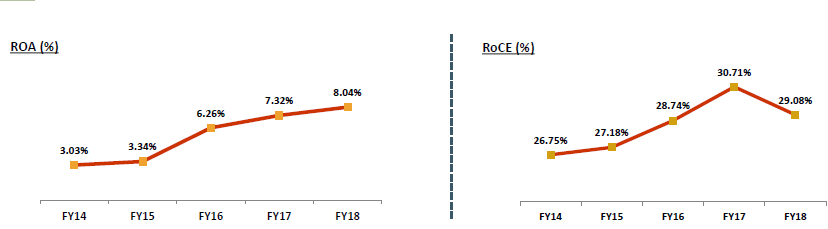

EBITDA margin rose to 10.92 percent in FY18 from 7.91 percent in FY14. Interestingly, its asset turnover ratio doubled in this period to about 2 times without a corresponding increase in debt (debt-to-equity: 0.7 times in FY18), which helped the company consistently improve its return on equity (RoE) from 26.75 percent in FY14 to 31 percent in FY17 and 29 percent in FY18 as a result of equity infusion through an initial public offering last year. No wonder its IPO was subscribed about 273 times.

Growth drivers

The company continues to deliver higher growth even in an otherwise dull market condition. During the quarter-ended September, revenue grew 54 percent to Rs 153.6 crore and profit jumped 42 percent. While the transmission and distribution (T&D) industry is facing demand issues, its strategy to diversify into railways, telecom and other segments is now paying good dividend.

Moreover, the company recently expanded its capacity to 100,000 tonne from 50,000 tonne. Last year, it received approved vendor status from Power Grid Corporation of India (PGCIL), which would be key to achieving higher scale and margin.

Opportunities in the T&D, telecom tower, railway electrification and other value-added products are relatively high. Besides, it is also working on new technologies that can fit other requirements such as smart poles, which are designed in such a way that they can accommodate LED lights, CCTV cameras, pollution sensors, Wi-Fi routers and road display systems for smart city projects.

The company is sitting on an order book of close to Rs 330 crore on an annual sales of Rs 502 crore.

Valuation

Over the past few months, led by broader correction in the mid- and smallcap space, the stock has fallen from a high of about Rs 400 a share in May this year to Rs 240 at present. In H1 FY19, earnings per share grew 33 percent to Rs 12.68. For FY19, we expect it to earn an EPS of around Rs 25. Taking that into account, the stock is currently trading at 9.6 times FY19 estimated earnings, which is quite reasonable for a company that is growing and has strong return ratios.

Moreover, Salasar has worked for almost all major companies in the industry – Larsen & Toubro (L&T), ABB India, Reliance Jio Infocomm, Tata Projects, Vodafone Idea, PGCIL, Bharat Heavy Electricals (BHEL)– demonstrating its capabilities. In terms of risks, investors needs to be vigilant considering it’s a small family run business and industry often goes through a painful cycle.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.