Jitendra Kumar Gupta Moneycontrol Research

Vedanta, one of India’s oldest and largest metal companies, boasts of a strong balance sheet on account of its cash and liquid investments of about Rs 35,251 crore in the books.

This cash, which is almost 42 percent of its current market capitalisation and 55 percent of FY18 shareholders' funds, on the contrary indicate weak capital allocation.

During the quarter the company booked other income of Rs 418 crore, which on an annualised basis gives us a yield of 4.77 percent on the cash and investments in the books. Despite the huge cash in the books, the company still prefers maintain gross debt of Rs 65,161 crore.

On an analyst call, management indicated it is looking to make use of this cash and is actively looking for ways to add value to its shareholders. Repaying debt, making acquisitions in related areas, investing in organic growth and payment of dividends to shareholders are some of the things that are being deliberated upon.

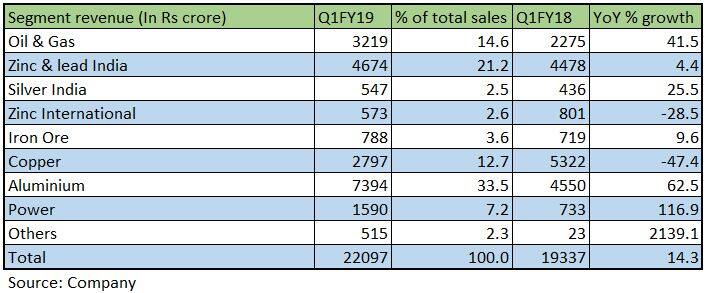

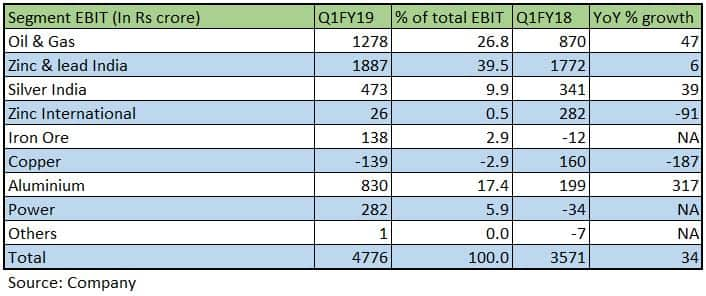

Q1FY19 results at a glance

In this context, it would be worth keeping an eye on cash and its deployment over the next few quarters. Meanwhile, thanks to a greater amount of diversification because of exposure to different commodity businesses (eight reported segments), Vedanta was able to mitigate some of the impact of slow growth reported by its key segments.

During the June quarter, the company was able to report closer to 15 percent growth in its revenues. This growth would been higher had its key segments such as copper and zinc (India business) grown at a decent pace. These two segments, which account for 33 percent of its revenue, reported 24 percent decline in sales, negating some of the gains seen in oil & gas segment (14.6 percent of revenue) that grew by 41.5 percent on year on year basis.

The copper business has suffered because of the shutdown of its Tuticorin copper plant. It not only dragged revenue growth but also hit consolidated profitability as a result of EBITDA loss of close to Rs 87 crore as against a profit of Rs 213 crore in the corresponding quarter last year.

Nevertheless, aluminium, its biggest segment accounting for 33.55 percent of the revenue, saved the day recording a strong 62.5 percent growth in sales led by strong growth in volumes and realisations.

During the quarter, LME aluminium prices were up by 18 percent to $2259 a tonne. And because of the ramp up in capacity and availability of alumina, the segment saw a strong 37 percent year on year growth in aluminium volumes to 4.8 million tonnes.

Moreover, the company’s efforts to save cost through optimisation of capacity and reduction in power and fuel cost has yielded good results translating to $50 a tonne saving in the cost of production. As a result of this, aluminium segment’s EBITDA saw a robust 138 percent growth. This is precisely the reason that the overall consolidated EBITDA saw a 31 percent growth in June 2018 quarter.

However, this did not add to profits, which grew by a modest 2.1 percent to Rs 1533 crore. The key reasons for the lower growth in profits was higher depreciation (in aluminium, oil & gas and zinc business) increase in tax and lower other income because of the dividend pay-out and mark to market impact on investments.

Valuations

Vedanta has brought in greater amount of stability to its business as a result of diversification and when few businesses perform below historical average the others takes care. Now with the acquisition of Electrosteel it has greater expectations in terms of its strong IRR post-integration and contribution to overall profitability.

LME prices have been moderately stable, with the global economy picking up and oil prices are on an upward trajectory. Keeping these factors in mind and large cash in the books, at current market price of Rs 223, the stock discounts its estimated FY20 earnings by 8 times which is reasonable.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.