Jitendra Kumar Gupta Moneycontrol Research

A lot of pure transmission and distribution (T&D) players are increasingly finding it difficult to cope up with the drop and possible slowdown in transmission capex, particularly in the conventional energy sector. Capex by Power Grid Corporation of India (PGCIL) has slowed and is expected to slow further due to lack of visibility in the power generation space. A lot of focus is shifting towards development of state transmission under state electricity boards (SEBs), the tendering of which is highly competitive, slow and a risk to cash flows.

Falling apart GE T&D India is one such player with a market share of close to 60 percent in the high-grade equipment and high-voltage direct current (HVDC) category. Orders in the T&D market are drying up considering the slow capex by PGCIL. This is now reflecting in the company’s performance, whose annual order intake has dropped to Rs 3,900 crore in FY18 from Rs 4,300 crore in FY17. In H1 FY19, order inflows dipped 42 percent on a year-on-year basis. Moreover, revenue visibility (order book-to-sales) has dropped from 2.4 times in FY16 to 1.6 times in FY18 and about 1.4 times at present.

Balancing act The company is now looking at export markets such as Nepal, Bangladesh and Africa. Currently, exports account for about 10 percent of sales. The management said there is a possibility of large projects in these markets and is eyeing orders in renewable energy transmission, which is a mere 5 percent of overall sales. Though it is of the view that the power generation mix could shift over the next decade or so, India would still require power considering the low consumption at present and future demand in light of the economic growth. This, irrespective of the generation mix, would require capex in T&D. To capture the value chain, GE is entering into lower voltage segments. It has already received one order from the railways.

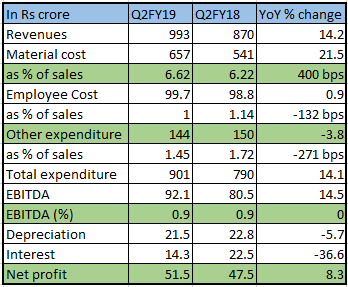

These orders may compensate for the revenue loss in existing portfolios. It would also be worth noting the timing and quantum of such a tactical shift. However, the same is bound to put pressure on margin because of competition. Part of this is already reflected in its reported numbers. During Q2 FY19, the company reported a 400 basis points (100 bps = 1 percentage point) decline in gross margin. Despite a 14 percent growth in revenue, reported profits grew a mere 8 percent to Rs 51 crore.

Besides, the management is looking to improve the quality of earnings, with increased focus on profitability and cash flows, which is now yielding results in terms of reducing working capital days and generating net free cash flows from operations.

Valuations Despite pressure on revenue and margin, the company continues to trade at very rich valuations. Based on the estimated profit of about Rs 200-220 crore in FY20, the stock at the current market price is trading about 28-31 times FY20 estimated earnings, which is clearly expensive. The company usually trades at about 24-25 times one-year forward earnings.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.