The FRDI (The Financial Resolution and Deposit Insurance Bill) is unlikely to become law anytime soon because of the furore over the ‘bail in’ clause. Gross misinterpretation is to blame for the controversy, but the government would want to steer clear of anything perceived to be anti-common man, as it readies for an election-heavy year. And yet, some irreversible changes have been set into motion that will have long-term implications for investors.

FRDI – a brief backgroundWe can’t recollect a bank failure since bank nationalisation. Not to say that no bank has ever been in trouble. But if a financial institution is terminally sick, it better to resolve the problem than risking the financial system by postponing the inevitable.

The need for a strong resolution mechanism, different from regulation, was necessitated by the 2008 global financial crisis. Since modern financial system is highly interconnected, failure in any one sector can have a domino effect and rattle the system as a whole.

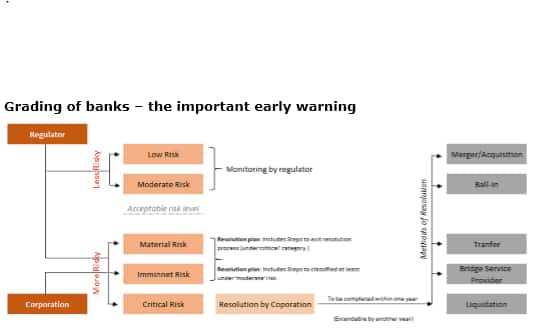

The new entity – Resolution CorporationThe Resolution Corporation proposed to be set up under the FRDI Bill is tasked solely with resolving failed financial institutions; it has no role in the day-to-day working of financial institutions such as banks and insurance companies.

The central government will establish a Resolution Corporation. It will provide deposit insurance to banks (in fact with stronger features than the existing deposit insurance of Rs 1 lakh under DICGC) and grade all covered financial institutions on a five-point scale of risk to viability. The Resolution Corporation will have no power as long as an entity is in good financial health and its risk of failure is below acceptable levels.

We perceive the grading of banks on this five-point scale a potent early warning. Only when an entity is classified at “critical risk to viability”, or simply put, it has failed, will the Resolution Corporation step in. It will begin the resolution process, using traditional tools such as liquidation, merger or amalgamation, transfer of assets and liabilities to a healthy entity etc.

Bail-in is one of the many resolution methods proposed in the Bill. Bail-in means cancellation or modification of certain liabilities to the extent necessary to recapitalise a financial entity from within. It certainly does not imply this tool can be used by the government arbitrarily. It can only be employed by the Resolution Corporation in consultation with the relevant financial sector regulator – the Reserve Bank, in the case of banks.

Given the checks and balances it is impossible to assume that there is any risk to depositors money. In fact, even today, beyond the insured amount, depositors money are unsecured liabilities. In fact, the grading mechanism will diagnose the problem early so that corrective action is taken well in advance which is similar to Prompt Corrective Action framework that exists under RBI.

What are the danger signs for banks?Investors should, therefore, incrementally focus on the five-point scale of risk to viability. The factors that will have a bearing on the risk scale could be – Capital adequacy, asset quality, management capability, earnings sufficiency, leverage, liquidity ratio, sensitivity to adverse market conditions etc.

When the risk is ‘material’ or ‘imminent’ the entity may be prohibited from accepting deposits, granting loans, paying dividends to shareholders and bonus to employees, acquiring another company, and raising capital. So, the objective here is to contain the problem through restrictions.

FRDI - a precursor to consolidation?So what does it mean for investors looking to buy banking shares?. Post 2019 general elections, the financial service sector could witness a churn that will reduce the number of state-owned banks in business. This Bill could facilitate a smooth and least disruptive implementation of the same. This is likely to be a gradual process which will benefit strong competitors both from the private as well as public sectors.

Of course, a key factor here will be the outcome of the elections and the stability of the government that comes to power.

Low level of capital in any case will not permit these entities to expand.

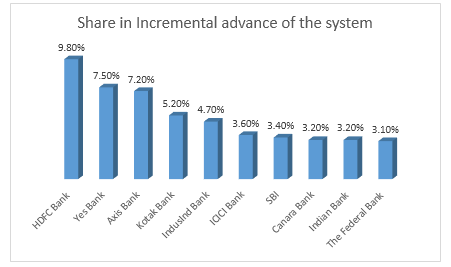

The shift in favour of stronger entities is already visible and will only accelerate as efficient banks wrest a greater share of incremental business.

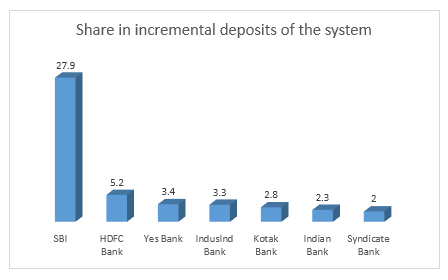

So who is growing in Indian banking now?

Weighed down by asset quality and lack of capital, the share of public sector banks in advances have fallen from 75 percent to 70 percent in the past two years as their incremental share is falling fast. Selective recapitalisation will improve outlook for some of them.

Private sector banks have hugely benefitted with their market share in incremental advances jumping to 46 percent from 26 percent in the same period last year.

Private sector banks, however, have not done equally well in improving their market share in deposits. But as weak banks are restricted from taking on fresh business, private sector banks should benefit, as will the larger public banks.

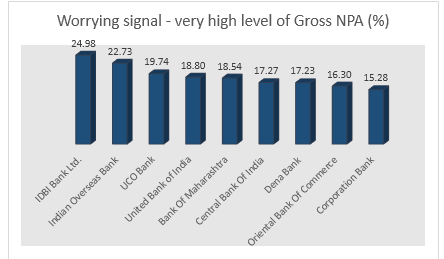

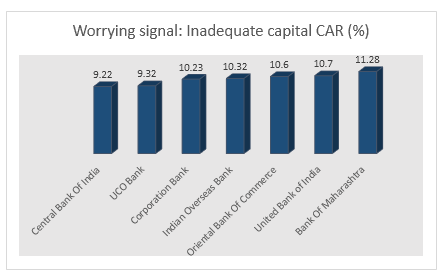

The weaker entities – still control a meaningful share of businessTake nine state-owned banks whose financials prima facie look extremely vulnerable– IDBI Bank, Central Bank, UCO Bank, Corporation Bank, Indian Overseas Bank, Oriental Bank of Commerce, United Bank, Bank of Maharashtra and Dena Bank.

While their market share in incremental advances declined by 8 percent in the period ending September 2016, it has declined even more steeply to 15 percent in the period ending September 2017.

On the deposits front, while these banks were still garnering market share in September 2016 (8.5 percent growth), in September 2017 their share in incremental deposits of the system has declined by close to 10 percent. Having said that their legacy business is still meaningful.

To put it in perspective, the aggregate deposits of these nine entities is close to 16% of system’s deposits. Even in the event of a merger with a larger efficient bank, some migration of customers and business to well-run private players should be expected.

The big boys in the street are upping the ante with smart capital raising, to play a bigger role in a changed landscape. SBI, PNB, Kotak Bank have already raised capital and HDFC Bank is also planning to.

Investors should, therefore, know which bank to back. In the regime of “survival of the fittest” the depositors will also be able to figure out early on on whom not to back, thanks to the early warning of the bill.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!