Sachin Pal Moneycontrol Research

Highlights:- Steady improvement in terms of top line and bottom line - Electrical consumer durables drove the overall sales growth - Higher advertising spends, technological investments impacted margins - Consumer durables penetration levels are low - Valuations offer favourable risk-reward ratio from a long-term perspective

-------------------------------------------------

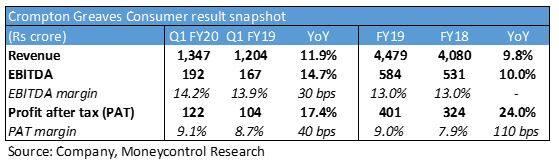

Consumer durable company Crompton Greaves Consumer Electricals (CGCE) sustained its earnings momentum of the previous few quarters and delivered a healthy growth in top line and bottom line in Q1 FY20. Overall performance was quite encouraging despite a weak demand environment.

Key result highlights

Revenues for the quarter increased by 12 percent year-on-year (YoY) to Rs 1,347 crore. Earnings before interest, tax, depreciation and amortisation (EBITDA) as well as profit after tax came ahead of top line on the back of moderate improvement in margins. EBITDA increased 15 percent YoY to Rs 192 crore while profit after tax rose 17 percent YoY.

Electrical consumer durables drove the overall top line growth. Fans, pumps and appliances, the key product categories under this segment, delivered double-digit volume growth during the quarter gone by. A combination of hot weather conditions, premiumisation strategy and market share gains aided the sales of fans in Q1 FY20. For pumps, revenue growth was weaker in comparison to the volumes due to a change in mix towards the economy segment. Crest Mini continued to perform well owing to healthy demand from agricultural and domestic segments.

In appliances, the new products such as geysers and coolers gained traction in the market and reported exponential revenue growth (>40 percent) on a small base. Overall segmental EBIT margins were supported by richer product mix and easing commodity prices.

Performance of Lighting & fixtures was in stark divergence to the consumer durables segment as it reported a contraction in sales as well as margins. Delay in government orders due to the general elections, along with a price erosion in LED bulbs, had an adverse impact on the overall sales. Margins took a hit on account of multiple factors. Advertising spends linked to ICC Cricket World Cup, continued investment in business to business vertical (B2B) and higher bad debt provisions resulted in a disappointing weak margin performance.

The company continues to focus on driving profitability through new innovative products (such as anti-bacterial bulbs) and rationalisation of cost structure. It is also broadening its distribution footprint and looking to enter new product categories through the inorganic route.

Despite the price erosion, LEDs volumes have been growing at a healthy rate and this remains the key revenue driver for the lighting and fixtures business and now contributes around 80 percent to the segment’s top line. Going forward, the management also plans to have a sharper focus on the B2B segment and has invested in both people and technology to drive sales.

Outlook and Recommendation

Consumer durables market is set for a major push, given the low penetration levels of electronics. The growth is being fuelled by some recent trends like the electrification programmes and the rising income levels of consumers across urban as well and rural markets. While the near-term demand trend suggests some weakness on the demand front due to sluggish economic activity, the long-term drivers remain intact due to shift in consumer preferences and changing lifestyles.

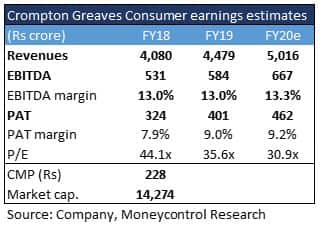

Crompton’s Q1 was ahead in comparison to its larger peer Havells. From a valuation standpoint, Crompton trades at a significant discount to the latter and offers a favourable risk-reward ratio on a relative basis.

We advise long-term investors to make use of any dips in the stock price to gradually build positions in Crompton Greaves Consumer Electricals as the company’s strategy of product innovation, diversification and premiumisation should help it gain scale in coming years.

Also read: This stock could be the next Havells

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed hereDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.