Sachin Pal Moneycontrol Research

Highlights:- Topline growth aided by incentive income of Rs 85 crore - Volume growth moderated to 7 percent in Q3 FY19 from 14 percent quarter-on-quarter - Operating margin declined on a sequential basis - Entered into agreement with JSC RZD Logistics to capitalise on international trade opportunities - Stock is trading at 25 times FY19 estimated price-to-earnings --------------------------------------------------

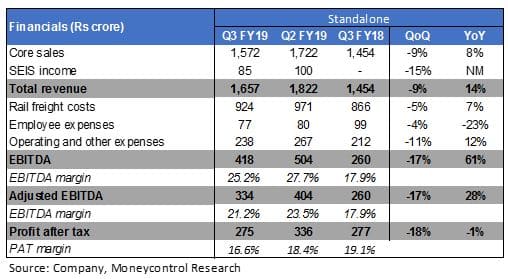

Container Corporation of India (Concor), the leading rail freight transporter, reported a mixed set of earnings for the third quarter of FY19. Growth in topline was driven by steady improvement in volumes and Service Exports from India Scheme (SEIS ) related income incentives of Rs 85 crore. However, the decline in sequential realisations and change in business mix impacted margin as well as the profit for the company in the quarter gone by.

Key Q3 positives

- For the quarter-ended December 2018, Concor’s total revenue increased 14 percent year-on-year (YoY) to Rs 1,657 crore on higher volumes in both EXIM (export-import) and domestic business

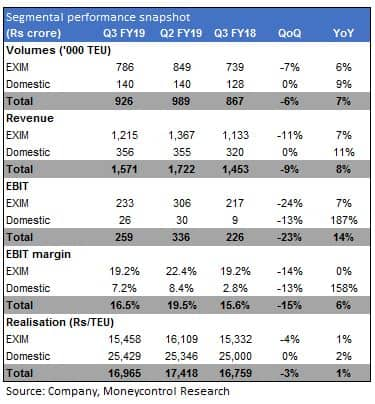

- EXIM volumes forms a majority of Concor’s revenue and continues to drive overall business growth. EXIM volumes for Q3 FY19 grew 6 percent YoY, while the domestic segment reported a 9 percent jump in volumes. Overall, the company’s handling volumes for the quarter under review stood round 0.93 million TEU (Twenty-foot Equivalent Unit), which translates to a volume growth of 7 percent for the overall business

- Adjusted operating margin (excluding SEIS income) improved 340 basis points (bps) to 21.2 percent on account of lower employee expenses (down 23 percent YoY) and significant improvement in profitability of the domestic business (EBIT margin of 7.2 percent in Q3 FY19 as compared to 2.8 percent in Q3 FY18)

- At the start of current fiscal, the management had indicated a foray into coastal shipping with an exclusive business partner. The plan seems to be progressing well as the company has initiated coastal shipping operations in Q4 FY19

- The management is also exploring various opportunities both on domestic as well as international front to tap into the freight and logistics market and emerge as an integrated container rail solutions provider. The company has recently entered into agreement with JSC RZD Logistics (Russia-based multi-modal logistics operator) for exploring logistic opportunities in Russia, India and the international corridor.

Key Q3 negatives - Overall volume growth for Q3 was soft at 7 percent as the company had recorded a volume growth in excess of 10 percent in each of the last four quarters

- Despite the recent freight rate hikes (increase of Rs 1,000 per TEU) as well as upward revision in service charges (increase by Rs 1,500 per TEU), realisation in the EXIM business declined 4 percent on a sequential basis. Drop in capacity utilisation levels during November and December 2018 resulted in negative operating leverage. Margin was also adversely impacted by higher volumes at Mundra and east-coast ports, which resulted in lower lead distance and consequently lower realisations.

Outlook and recommendation - Domestic business volumes continue to head higher in tandem with economic activity in the country. EXIM volumes, however, witnessed some tapering in growth on the back of subdued international trade in the latter half of Q3. There exists risk to business volumes with regards to global slowdown concerns that might lead to a subdued trade activity both on the international as well as domestic front.

- For the nine-months ended December 2018, the company has clocked a volume growth of 10.4 percent, which seems in line with the management's FY19 guidance range of 10-12 volume growth. While business volumes needs to be monitored closely, things appear positive as the management is taking multiple initiatives to diversify its business by leveraging its core capabilities and entering new business segments through various strategic partners.

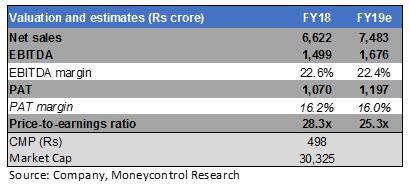

- In terms of valuation, Concor is currently trading at FY19 estimated price-to-earnings multiple of 25 times. We recommend that investors accumulate the stock in a staggered manner as the company enjoys market leadership, healthy balance sheet and strong revenue visibility.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.