The shares of State Bank of India fell more than 5 per cent intraday to hit a near-five-month low on August 5 even as brokerage houses slashed price target, as the country's largest public sector bank missed profit expectations in the June quarter (Q1), and slippages were higher.

The stock has fallen more than 21 per cent since July 17, 2019. It was quoting at Rs 294.40, down Rs 14.05, or 4.56 per cent on the BSE at 1125 hours IST, before staging a partial recovery.

The country's largest lender reported a standalone profit of Rs 2,312.20 crore in Q1, against loss of Rs 4,875.85 crore in year-ago period. Net interest income increased 5.2 per cent year-on-year to Rs 22,938.8 crore during the quarter.

Asset quality was stable, with gross non-performing assets as a percentage of gross advances flat at 7.53 per cent in Q1, compared to the previous quarter. However, gross slippages, at Rs 16,212 crore for the June quarter, rose by a steep 62.38 per cent year-on-year and 116.01 per cent sequentially.

Hence, the slippage ratio increased significantly to 2.83 per cent in Q1FY20, from 1.39 per cent in Q4FY19.

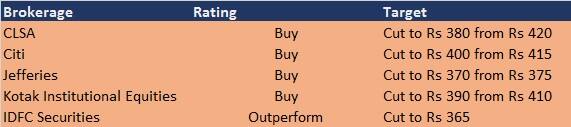

Brokerages retained a positive stance, but slashed the price target following the higher slippages. They see scope for higher credit cost in FY20 and see downside risks to earnings from a larger watchlist.

"Higher slippages disappointed, and Q1 net profit were below our expectations due to higher credit cost," said CLSA. which has a buy call on the stock but cut price target to Rs 380 from Rs 420 per share.

The global brokerage further said key disappointment was rise in SBI's delinquency ratio to 3.4 per cent of the past year’s loans, and said it sees scope for credit costs to remain higher in FY20.

However, the upside can arise from the resolution of cases at NCLT like Essar Steel, CLSA said.

Here is what other brokerages say about the SBI stock and its earnings:

Brokerage: Kotak Institutional Equities | Rating: Buy | Target: Rs 390

The bank reported a weak start to FY20 with slippages at 3 per cent of loans. Higher slippage from agriculture and SME are seasonal in nature and less worrying.

Timing is uncertain but Kotak is optimistic that FY20 should be better against FY19. It maintained buy call on the stock and cut target price to Rs 390 from the previous one of Rs 410 per share.

Brokerage: IDFC Securities | Rating: Outperform | Target: Rs 365

The management has revised guidance of core return on assets (RoA) to 0.5-0.6 per cent from 0.6-0.7 per cent.

The brokerage cut earnings estimates and price target to Rs 365 per share, but maintained its outperform call on the stock on inexpensive valuation.

IDFC sees downside risks to earnings from a weak macro, high pension costs and the larger watchlist.

Brokerage: Citi | Rating: Buy | Target: Rs 400

SBI reported healthy loan growth but slippages increased in Q1. Its Q1 net profit was below brokerage and consensus estimates, due to higher provisions (9 per cent ahead of estimates) and lower treasury income.

Loan growth was healthy at 14 per cent YoY driven by retail. Citi maintained its buy call, but slashed the target price to Rs 400 from Rs 415 per share.

Brokerage: Jefferies | Rating: Buy | Target: Rs 370

Quarter did not have much to cheer about, said Jefferies, which cut its price target to Rs 370 from Rs 375 per share after reducing EPS estimates for FY20 by 7.8 per cent and FY21/22 by 3.2/5.5 per cent.

Disclaimer: The above report is compiled from information available on public platforms. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.