Aditya Iyer

On May 23, India voted for a decisive mandate, which granted Narendra Modi a second stint as the prime minister of the country. The certainty of a stable government was lauded by the market, as Nifty and Sensex surged to all-time highs of 12,000 and 40,000 respectively.

For equities as an asset class a stable government has always heralded an increase in risk appetite amongst investors. We saw that in 2014, when small cap stocks went through the roof along with a broad basing of market movements and we expect a similar phenomenon to transpire stepping into Modi 2.0.

Rally in non-Nifty stocks giving the first indication

A study on the volume action and price action of non-Nifty stocks indicate that the market is willing to look beyond the select mega caps and the risk profile of market participants might be changing.

Interestingly, in the past few days, the volume of midcaps as a percentage of total NSE volumes have risen sharply and is currently accounting for more than 50 percent (after dipping down to about 37-38 percent recently).

Generally, when the risk appetite is low, Nifty stocks form majority of volumes as was seen much through 2018 where they accounted for nearly 60 percent of NSE volumes.

However, when the risk on sentiment returns, this trend has reversed. For instance, Nifty volumes to total NSE volumes kept declining from 46.9 percent in 2014 to 38.6 percent in 2017, when mid-caps ruled the roost. Hence, the market preference towards mid cap is usually a feature of bullish sentiments and suggests a stance by investors towards riskier assets.

Also, sectors that have been beaten down for years have started heating up. For example, Nifty Reality, which had been down for 10 years, has risen 22 percent since February lows and the Nifty PSU index has moved 31 percent from its February lows.

Moreover, the number of stocks recovering from their recent lows, have displayed the fastest ever rise above 20-DMA since January 2017.

This is another signal of some aggression to buy and perhaps attests to a large amount of money waiting in the wings to be deployed into the market. So far, the market was dominated by a few stocks and now we are seeing the rally become more broad-based.

Gradual mean reversion will ensure midcap outperformance

The mid and small cap universe have had huge underperformance compared to large caps. In the midcap space, stocks are still trading up to 83 per cent lower from their 52-week highs. The valuation differential also is hitting historical highs. The midcap forward PE, which is currently trading at a 19 percent discount to Nifty forward PE, is moving towards historical extremes and eventually it will have to mean revert.

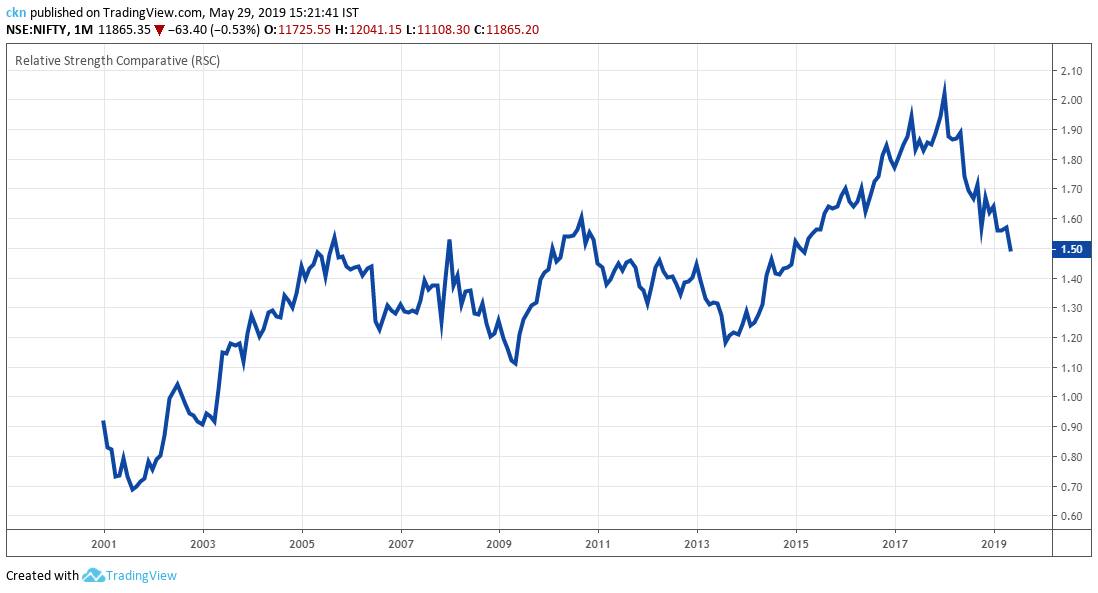

The mid cap index to Nifty ratio is at 1.5, the last time we witnessed these levels was in 2005.

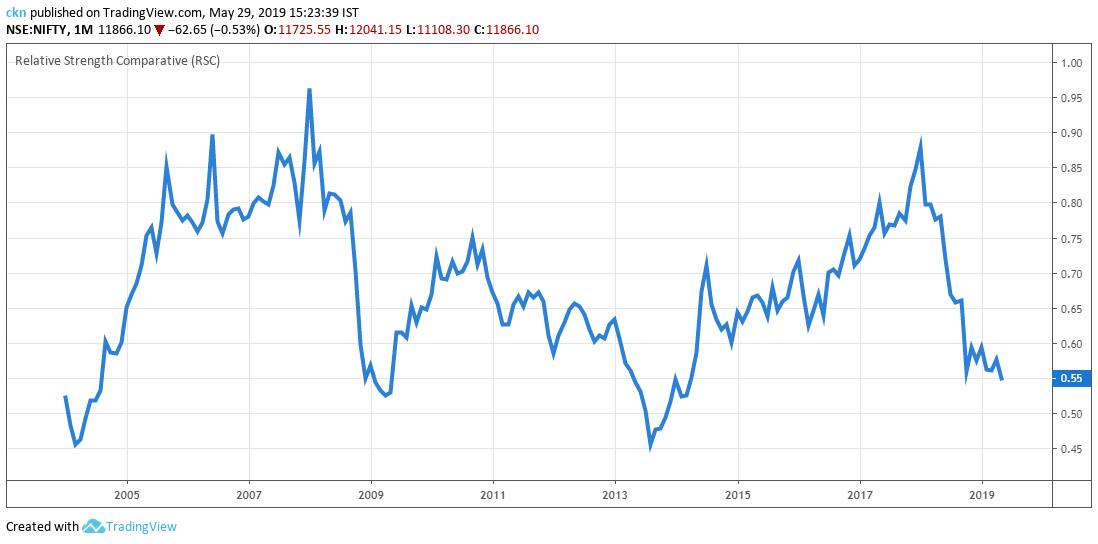

Similarly, The Small cap index to Nifty ratio is at an abysmal 0.5

Similarly, The Small cap index to Nifty ratio is at an abysmal 0.5 Both these ratios are well below the 15 year average and have moved into extreme zones. Prices will not sustain at such extremes for long and will eventually have to mean revert. Once the mean reversion process begins, we will start witnessing a catch up trade in these counters that will create the bouts of momentum waiting to be grabbed. Pace of equity inflows to increase Equity inflow into the market will definitely see a significant increase in the coming months. As I stated in my last article, FII flows will continue to increase, domestic institutions who were net sellers will also start going long. Since the election uncertainty has ended and we have clear road ahead, the pace of SIP and mutual fund flows into the market will increase as incremental bunched up domestic flows that were sitting on the sidelines will be unleashed in the market. Case in point would be the recent MSCI rejig which the market gobbled up in one day. Passive FPI outflows have been replaced by active FPI inflows and DII inflows. Retain bias towards midcaps, albeit with a balanced approach Opportunities will arise in various pockets of the market, a decline in oil prices and rupee appreciation can benefit OMCs who gain from lower under recoveries and manufacturing companies that get a fillip in the form of lower input cost inflation. Through these letters we have been urging our investors to increase allocation towards midcaps. We believe there must be a balanced approach as both types of flows will enter the market; i.e. retail and institutional flows. This will create momentum breakouts in many stocks that investors can use to profit from. Our property investment model is built to take advantage of these factors and investors can reach out to Plus delta portfolios to gain from these investment themes. The author is the Fund manager of Plus Delta Portfolios- PMS vertical of Growth Avenues Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on moneycontrol.com are their own, and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Both these ratios are well below the 15 year average and have moved into extreme zones. Prices will not sustain at such extremes for long and will eventually have to mean revert. Once the mean reversion process begins, we will start witnessing a catch up trade in these counters that will create the bouts of momentum waiting to be grabbed. Pace of equity inflows to increase Equity inflow into the market will definitely see a significant increase in the coming months. As I stated in my last article, FII flows will continue to increase, domestic institutions who were net sellers will also start going long. Since the election uncertainty has ended and we have clear road ahead, the pace of SIP and mutual fund flows into the market will increase as incremental bunched up domestic flows that were sitting on the sidelines will be unleashed in the market. Case in point would be the recent MSCI rejig which the market gobbled up in one day. Passive FPI outflows have been replaced by active FPI inflows and DII inflows. Retain bias towards midcaps, albeit with a balanced approach Opportunities will arise in various pockets of the market, a decline in oil prices and rupee appreciation can benefit OMCs who gain from lower under recoveries and manufacturing companies that get a fillip in the form of lower input cost inflation. Through these letters we have been urging our investors to increase allocation towards midcaps. We believe there must be a balanced approach as both types of flows will enter the market; i.e. retail and institutional flows. This will create momentum breakouts in many stocks that investors can use to profit from. Our property investment model is built to take advantage of these factors and investors can reach out to Plus delta portfolios to gain from these investment themes. The author is the Fund manager of Plus Delta Portfolios- PMS vertical of Growth Avenues Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on moneycontrol.com are their own, and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.