Engineering construction behemoth Larsen & Toubro has announced buying Mindtree investor V G Siddhartha's 20.32 percent stake in the company at a price of Rs 980 per share. The deal doesn’t stop there. L&T intends to mop up Mindtree shares from the open market and do an open offer up to 31 percent of Mindtree’s equity. What does this mean for different stakeholders and how should investors be positioned in this takeover battle?

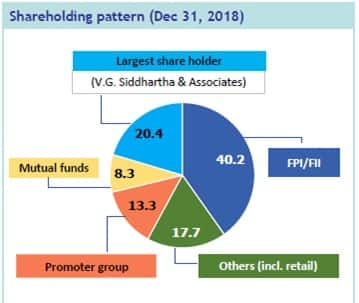

First and foremost, let us remember that barring L&T’s deal with V G Siddhartha, nothing else is cast in stone at this point in time. The founder promoters of Mindtree Krishnakumar Natarajan, NS Parthasarathy, Rostow Ravanan and Subroto Bagchi, who hold 3.72%, 1.43%, 0.71% and 3.1% respectively, are opposed to the idea of giving up control. The total holding of promoter and promoter entities is 13.32 percent.

The stance of the promoters will remain critical as promoters would like to thwart the deal to the extent possible. The success of L&T would largely hinge on the other prominent shareholders of the company.

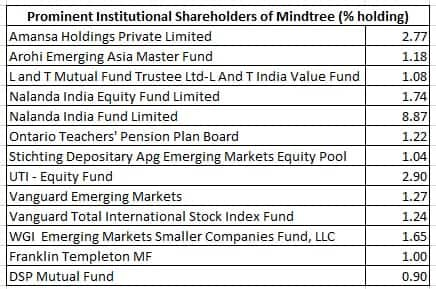

Of this L&T Mutual Fund wouldn’t be an issue, but the approach of the other shareholders would be key. It is important to mention that Pulak Prasad’s (ex Warburg Pincus) Nalanda holds a significant stake (10.61 percent) and if they are backing L&T, the road will be less rocky for the acquirer.

Can minority shareholders ask for more?

L&T has proposed to buy a stake in Mindtree at a price of Rs 980 per share valuing the company at 17.8x FY20e earnings.

Going by its recent track record of performance, Mindtree is obviously a highly sought-after company, which has carved out a niche for itself in the areas of new technology with its early adoption of digital that is beginning to yield rich dividends now.

Hence, to get excited about an exit, it is likely that institutions, as well as minority shareholders, would only be keen to get a significant premium.

At a valuation similar to the bellwether TCS (21X Fy20e earnings), the price for Mindtree would have been Rs 1155 per share (the 52-week high price for the stock is Rs 1182).

What’s the risk for Mindtree minority shareholders?

The biggest risk for Mindtree shareholders is the probable business disruption due to the ongoing ownership battle which might consume disproportionate management bandwidth and could even make clients wary. So the likelihood of a few soft quarters cannot be ruled out.

However, if L&T is desperate to own a majority in Mindtree, it might have to pay a higher price than what has been proposed now. In sum, existing shareholders of Mindtree should stay put.

L&T – a clear shift in focus

The proposition for L&T is interesting and marks a change worth taking note of. The keenness to acquire a rival IT company (after already having two in its own stable) clearly shows a shift in strategy of this infrastructure company away from its exposure to the investment side of the economy to asset light services business.

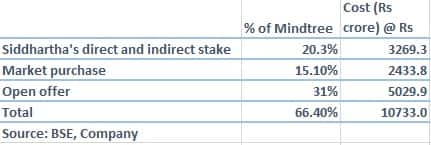

L&T proposes to do this Mindtree transaction in three stages with a total outgo of close to Rs 10,733 crore at the proposed price of Rs 980 per share.

L&T would be using its own balance sheet for funding. In FY18, its standalone networth was Rs 49,000 crore and total borrowings (short term as well as long term) were Rs 10,561 crore and it had over Rs 4000 crore in cash.

It is important to remember here that L&T in recent times was mulling a buyback to the tune of Rs 9000 crore. So we do not expect L&T to significantly leverage up for this transaction. Should it succeed, L&T would have access to Mindtree’s incremental profit of close to Rs 590 crore in FY20, and we do not see earnings dilution unless L&T has to pay a much steeper price than what it has proposed now. In the long term, the addition of a high return, low capital intensive business should be value accretive for the shareholders.

What does it mean for shareholders of LTI?

While it is premature to comment on the future and the likelihood of bringing LTI (L&T Infotech) and Mindtree together, synergies will flow through should such an integration eventually takes place.

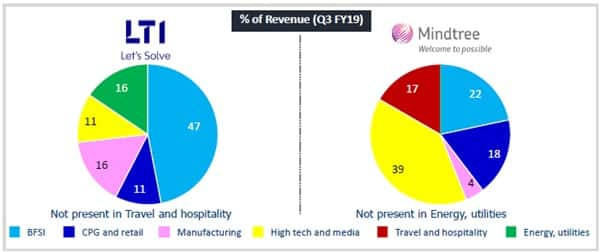

In terms of verticals, LTI has a lot to gain as Mindtree has a strong presence in technology, media & services (close to 39 percent) where the rate of growth of digital adoption is very high. The other verticals where Mindtree has a strong footprint are retail and CPG (consumer packaged goods) and travel and hospitality – industries that are in the forefront of digital adoption. In fact, the share of digital in total business for Mindtree is much higher at 49.5 percent compared to 37 percent for LTI. There is very little client overlap between the two companies.

For LTI shareholders, should Mindtree eventually comes under its fold, there would be synergistic gains. LTI has been reporting a much better operating margin of close to 20 percent compared to 15 percent for Mindtree. While for LTI this has come with a record high utilisation rate of 82 percent (compared to 74.6 percent for Mindtree), we feel the synergistic benefits coupled with sharper focus of LTI management can lead to improvement in Mindtree’s margin performance.

Since the LTI balance sheet is not being used for this acquisition, this is good news for LTI shareholders. After a period of underperformance (mainly due to concerns of the acquisition), the stock is valued at 16X FY20e earnings. With a key event risk behind us, we recommend accumulation.

L&T has a 74.8 percent stake in LTI and 80.4 stake in L&T Technology Services (engineering focused IT). Should it succeed in getting a majority stake in Mindtree, the combined revenue of the three entities for the first nine months of FY19 would have been $2.2 bn.

But the key questions at this point are: will the promoters of Mindtree give up and will the other minority shareholders agree to sell at a price of Rs 980?

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.