| In-demand jobs: Finance, Sales, Support")

Over the last year, the Indian banking industry has focused on risk mitigation. Major private banks, with a few exceptions, shifted the focus to safer retail assets from high risk corporate loans. This trend has continued in the fourth quarter as well. The common theme in the Q4 earnings report cards of two big private banks—Axis Bank and ICICI Bank—is a clear shift to secured retail advances. Among the banks, ICICI Bank has grown its retail book more aggressively than its rivals. Analysts call this a timely shift to de-risk the loan book. HDFC Bank, on the other hand, chose to grow its corporate book at a faster pace than retail loans.

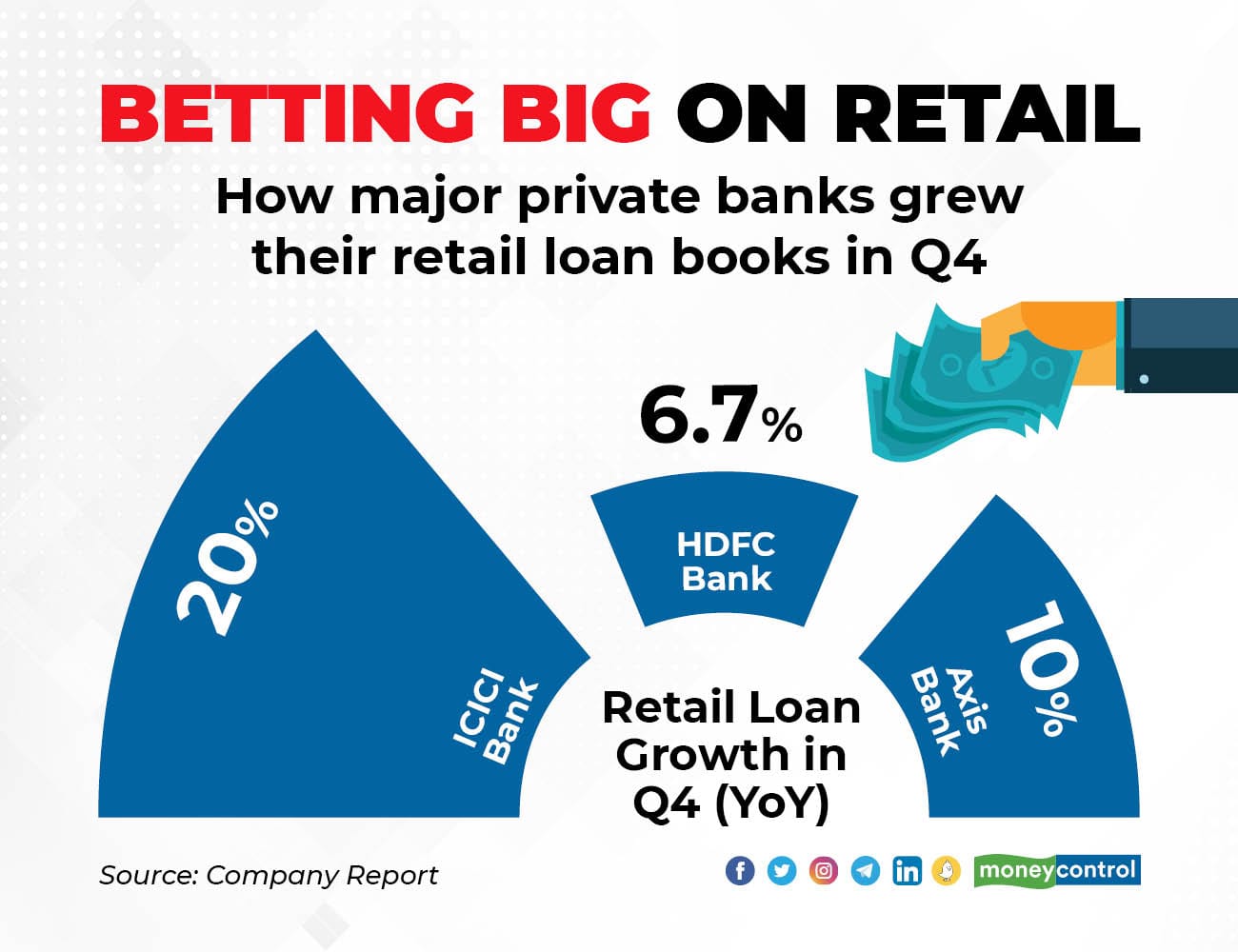

Some numbers first

In the case of ICICI Bank, retail book grew by 20 percent year-on-year (YoY) and 7 percent sequentially during the quarter ending March 31, 2021. Retail loans comprised 67 percent of the total loan portfolio at March 31, 2021. In the case of Axis, the retail loans grew 10 percent YoY (year-on-year) and 7 percent QoQ (quarter-on-quarter) and accounted for 54 percent of the net advances of the Bank. Domestic retail loans grew 11 percent YoY and 7 percent QoQ. The share of secured loans was 81 percent with home loans comprising 36 percent of the retail book.

Retail disbursements touched new all-time highs led by higher contribution from secured loan segments. Disbursements in Consumer segment were up 45 percent YoY and 44 percent QoQ, with secured segments like home loans up 73 percent YoY and 45 percent QoQ, and LAP (loan against properties) was up 53 percent YoY and 51 percent QoQ. Compared with this, HDFC Bank has grown its retail book at a slower pace. It's domestic retail loans grew by 6.7 percent and domestic wholesale loans grew by 21.7 percent. The domestic loan mix as per Basel 2 classification between retail and wholesale was 47:53.

Where is the growth coming from?

According to analysts, banks are growing retail books both through fresh business acquisition and buying out or taking over loan portfolios from NBFCs and cooperative banks where rates continue to be high. “These banks offer lower rates. NBFC and co-operative banks provide high cost loans. They are ripe targets,” said Jyoti Roy, analyst at Angel Broking.

Most of the growth is coming from the home loan portfolio. Within retail, home loans are the favourite of banks because of relatively low risk and high margin. Banks have aggressively grown their mortgage book attracting the retail borrowers with lower rates and benefitting from the recent stamp duty cuts. In the case of ICICI bank, home loans form almost half of the retail loans and this chunk has grown 22 percent on a year on year basis.

For Axis, the growth in home loans was 73 percent on YoY basis and 45 percent QoQ. Home loans now comprises 36 percent of the Axis’ loan book. HDFC Bank, in comparison, has grown home loans by 10 percent YoY and 5 percent on QoQ. Except in HDFC Bank case, both ICICI Bank and Axis have grown their retail book at a much faster pace.

Another reason why big banks are focusing on retail could be lower demand from corporates. Over the last one year, the economic activity has been severely impacted by the pandemic. This has reflected in demand for fresh loans also. The Indian economy is likely to have contracted by 7.5 to 8 percent in FY21. Not just big corporations, demand from small and medium-sized companies too have slowed down over the last one year.

Will huge growth in retail continue?

In the conference call post the announcement of the results, ICICI Bank management said the high growth seen in retail loans may not be continue going ahead. The lender attributed the high growth in Q4 to reasons like stamp duty cuts and benign interest rate environment. Axis Bank too said it will walk cautiously looking at the quality of assets. “We will grow both our secured and unsecured books but the way things are on the ground, we will be cautious on the unsecured loans,” said the management officials at the post result press conference.

Will the aggressive push on retail loans back fire?

Some analysts have sounded caution. “Retail demand is good but can’t say how the asset quality will pan out after a year,” said Siddharth Purohit, analyst at SMC Global securities. "Banks need to be cautious on asset quality," said Purohit.

Purohit is right. COVID situation is worsening across certain states forcing many states to go into partial or full lockdowns. These include Maharashtra, Gujarat and Karnataka. Prolonged lockdowns can lead to job losses and impact the repayment ability of the borrowers. Last year, the impact of the economic stress was not visible on the bank balance sheets due to the RBI's intervention. The RBI offered support to the banking sector in the form of loan moratorium and restructuring while the government announced an economic stimulus package to fight COVID.

Banks’ aggressive shift to retail assets could boomerang if COVID second wave gets prolonged and vaccination drive doesn’t progress as planned.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.