For years, every Union Budget in India seemed to bring a fresh shake-up in the taxation of insurance products, especially life insurance and unit-linked insurance plans (ULIPs). However, Union Budget 2026, presented by Finance Minister Nirmala Sitharaman on February 1, broke that pattern. Unlike its predecessors, it did not announce any major tax reform specific to the insurance sector.

That silence itself, according to industry practitioners, may be the most significant signal of all. After years of iterative policy intervention, India’s insurance market may finally be moving past an era of regulatory realignment into one of relative stability.

There seems to be a sense of relief across the sector.

The January-March quarter is critical for insurers and typically accounts for 30-40 percent of annual business volumes. "Policy stability during this period is important because any tax or regulatory disruption would have directly impacted growth momentum and year-end performance," an industry practitioner said on the condition of anonymity.

Another senior industry official, speaking on condition of anonymity, said the lack of tax changes was largely expected. “With risk-based capital (RBC) norms on the way, and the GST-cut that happened last year, the sector knew that there would be no major taxation changes. Everyone is preparing for the RBC regime, and any fresh tax restructuring would only complicate that transition,” the official said. "What we did expect was clarity on regulatory developments such as third party motor premiums and composite licensing, but nothing particularly on taxation."

A second executive echoed this view, noting that even Budget 2025 did not introduce substantive structural changes. “To be fair, the government did not technically make major changes in 2025 either, it was largely a clarification on ULIP taxation. The early signs of stabilisation began there. With the risk-based framework coming in, I don’t see the government introducing disruptive changes now,” the executive said.

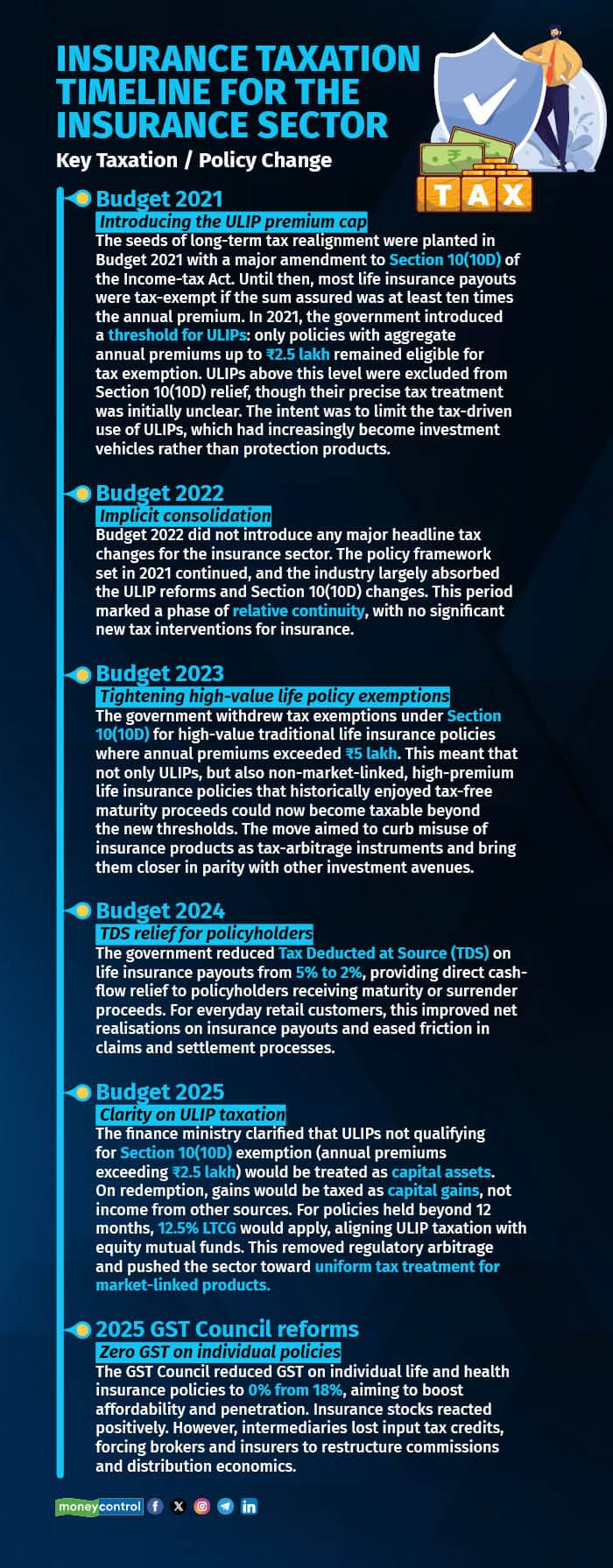

Insurance taxation timeline for the insurance sector

Insurance taxation timeline for the insurance sector

Budget 2021: Introducing the ULIP premium cap

The seeds of long-term tax realignment were planted in Budget 2021. One of the most significant amendments was made to Section 10(10D) of the Income-tax Act, wherein the provision governing tax exemptions on life insurance maturity proceeds. Until then, most life insurance payouts were tax-exempt if the sum assured was at least ten times the annual premium. But in 2021, the government introduced a threshold for ULIPs: only policies with aggregate annual premiums up to Rs 2.5 lakh would remain eligible for this exemption. ULIPs above this level were excluded from Section 10(10D) relief, although their precise tax treatment initially remained ambiguous. The intent was clear, which was to limit the tax-driven use of ULIPs, which had increasingly become investment vehicles rather than protection products.

Budget 2022: Implicit consolidation

Budget 2022 did not introduce major headline tax changes for the insurance sector. The policy framework set in 2021 continued, and the sector largely absorbed the ULIP reforms and Section 10(10D) changes. This period marked a phase of relative continuity, with no significant new tax interventions for insurance.

Budget 2023: Tightening high-value life policy exemptions

In Budget 2023, the government tightened the regime further by withdrawing tax exemptions under Section 10(10D) for high-value traditional life insurance policies where annual premiums exceeded Rs 5 lakh. This meant that not only ULIPs, but also non-market-linked, high-premium life insurance policies that had historically enjoyed tax-free maturity proceeds, could now become taxable beyond the new thresholds. The move aimed to curb the misuse of insurance products as tax-arbitrage instruments and bring them closer in parity with other investment avenues.

Budget 2024: TDS relief for policyholders

By Budget 2024, the narrative began shifting from restriction to operational relief. The government reduced Tax Deducted at Source (TDS) on life insurance payouts from 5 percent to 2 percent. This provided direct cash-flow relief to policyholders receiving maturity or surrender proceeds.

For everyday retail customers, the move improved net realisations on insurance payouts and helped ease friction in claims and settlement processes.

Budget 2025: Clarity on ULIP taxation

Budget 2025 delivered the most consequential clarification for the sector in recent years by resolving long-standing ambiguity around ULIP taxation. The finance ministry clarified that ULIPs not qualifying for Section 10(10D) exemption, where annual premiums exceed Rs 2.5 lakh, would be treated as capital assets. On redemption, gains from such policies would be taxed as capital gains, not as income from other sources. For policies held beyond 12 months, long-term capital gains tax at 12.5 percent would apply, aligning ULIP taxation with equity mutual funds. This effectively removed regulatory arbitrage between ULIPs and mutual funds and pushed the sector towards uniform tax treatment for market-linked products.

2025 GST Council reforms: Zero GST on individual policies

Although outside the Union Budget process, the GST Council’s decision in late 2025 to reduce GST on individual life and health insurance policies to 0 percent from 18 percent marked a major fiscal shift for the sector. The move aimed to boost affordability and penetration, and insurance stocks responded positively. However, it also created unintended consequences, where intermediaries lost input tax credits, forcing brokers and insurers to restructure commissions and distribution economics.

Against this backdrop, Budget 2026’s absence of insurance-specific tax changes becomes meaningful. While income tax laws were amended, including the transition toward a new Income Tax Act effective April 1, 2026, there were no provisions targeting life insurance, ULIPs, or insurance taxation.

An executive added, "With ULIP taxation aligned to capital markets, TDS reduced, and GST exemptions improving affordability, insurers can now focus on core business fundamentals such as expanding coverage, improving product relevance, strengthening distribution, and building trust, rather than redesigning products in response to fiscal changes."

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.