Ruchi AgrawalMoneycontrol Research

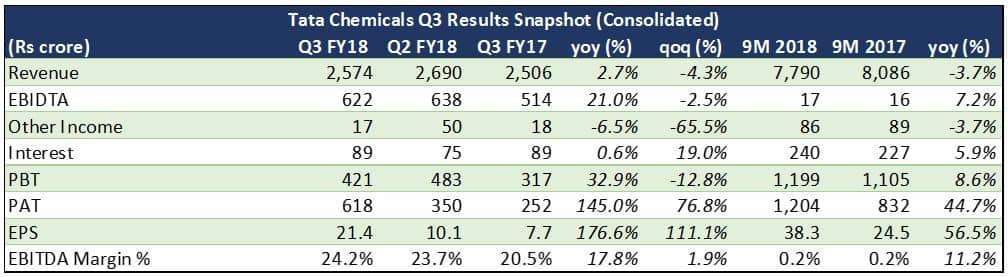

Tata Chemicals (TCH) reported a stellar performance in Q3 FY18 on the back of improved realisations from soda ash and strong domestic volume growth. While consolidated revenue at Rs 2,574 crore grew a mere 2.7 percent, a 360 basis points EBITDA margin expansion due to operational efficiencies led to almost a 21 percent uptick in EBITDA and a 33 percent operating profit expansion.

With completion of the restructuring, the company is now positioned to focus on expansion of core segments amid rapid growth.

Improved soda ash realisations

The company witnessed an improvement in soda ash realisations across geographies due to an increase in soda ash prices following the shutdown of factories in China and reduced supply. While Europe and Africa saw a sharp increase in prices at 8 and 17 percent respectively, North America and domestic prices increased marginally by 3 and 2 percent. The management indicated that the situation was balanced as the decrease in supply from China is being taken over by supply from Turkey.

With rising energy costs the company has further raised the price of soda ash in domestic markets in Q4, due to which margins are expected to remain stable.

Mixed volume growth

Although soda ash prices increased across geographies, the same was partially neutralised by a mixed volume growth. While the domestic soda ash business saw a healthy volume growth of 11 percent and African volumes grew at 15 percent, Europe saw a 15 percent decrease in volumes. North America remained almost flat.

Update on Rallis

Rallis, the Agri arm of Tata Chemicals, reported subdued performance with a contraction in operating margins. Although revenue increased on the back of an uptick in volume, price pressure from imported raw material (45 percent) on account of closure of Chinese facilities weighed negatively on gross margins. The management plans to focus on existing molecules and expand reach through aggressive product registrations. Owing to the contraction of Chinese supply, the management is also exploring opportunities to venture into manufacturing, though skepticism around rapidly changing Chinese government policies would be something to watch out for while evaluating the benefits.

Deleveraging benefits

The company has strategically exited the low profitability and high working capital segment of urea and phosphatic fertilizers post which the business is now net debt free at the standalone level. The divestment would also free up working capital locked in due to delay in subsidy reimbursements and provide additional funds for debt repayment and expansion of specialty chemicals and consumer segments.

New investments to drive growth

According to the management, the new investments for the nutraceutical plant and the highly dispersible silica (HDS) business will be the key growth drivers in the medium term and a return of capital employed (ROCE) of more than 20 percent is expected from the segments. Moreover, the current product portfolio in the consumer products business is expected to break even during FY19, and the company has plans to introduce new products and product lines to capture market share, which would drive growth in the long-term.

Outlook

The core soda ash business is operating at nearly peak utilization levels due to which further growth from there is not expected in the short term. We believe that the completion of restructuring and de-leveraging of the balance sheet, coupled with higher revenue from new investment and the shift to asset light but relatively high-margin businesses will have a positive rub-off on profitability and return ratios in the long-term.

The stock has run up 23 percent over the last 12 months despite the 5-6 percent correction that has been seen in the past one month. The market has been volatile over the past one month. It is now trading at a 2019E PE of 15.6x and an EV/EBITDA of 7.9x. At current price levels, the stock is an attractive buy.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.