")

Nine days after Avraham Eisenberg began to borrow curve cryptocurrency tokens on Aave, a decentralised lending platform for digital assets, he found his $38 million loan abruptly liquidated by terminator bots.

An estimated $10 million loss on a failed punt sounds only mildly annoying, compared with everything else going on in Eisenberg’s life — the self-described “applied game theorist” was arrested in Puerto Rico recently for allegedly draining $110 million from trading platform Mango Markets. Still, the zapping of the trader’s short CRV position, as the curve tokens are known, has sparked a lively debate.

The abruptly curtailed life of the loan is a feature of decentralized-finance, or DeFi, marketplaces that allow volatile cryptocurrencies to be lent against one another. The trader had borrowed CRV tokens by posting USDC, a dollar stablecoin, as collateral.

If this were conventional debt, the borrower would get a margin call when the lender became uncomfortable with the collateral covering it. On a public blockchain, anybody can track such situations. To keep the system safe, arbitrageurs are encouraged to step in. These are algorithms that raise a so-called flash loan (more on them later) to liquidate vulnerable short positions. They pocket a reward from the software code — smart contract — running lending protocols such as Aave.

Although not directly linked to the Eisenberg loan, recent work by academic researchers has concluded that DeFi harbors a systemic fragility, wherein liquidations engender other liquidations. Collateral prices get affected across trading venues; the malaise spreads. Flash loans are to blame — they’re so fast and frictionless that decentralized lending becomes inherently crash-prone.

At the opposite end are practitioners who believe teething problems are normal for a nascent industry. DeFi deserves a fair chance to create a cheaper alternative to intermediary-driven traditional finance, or TradFi, which — for all the progress since the advent of the 17th-century goldsmith-banker — still relies on expensive taxpayer-funded bailouts. Remember the subprime crisis?

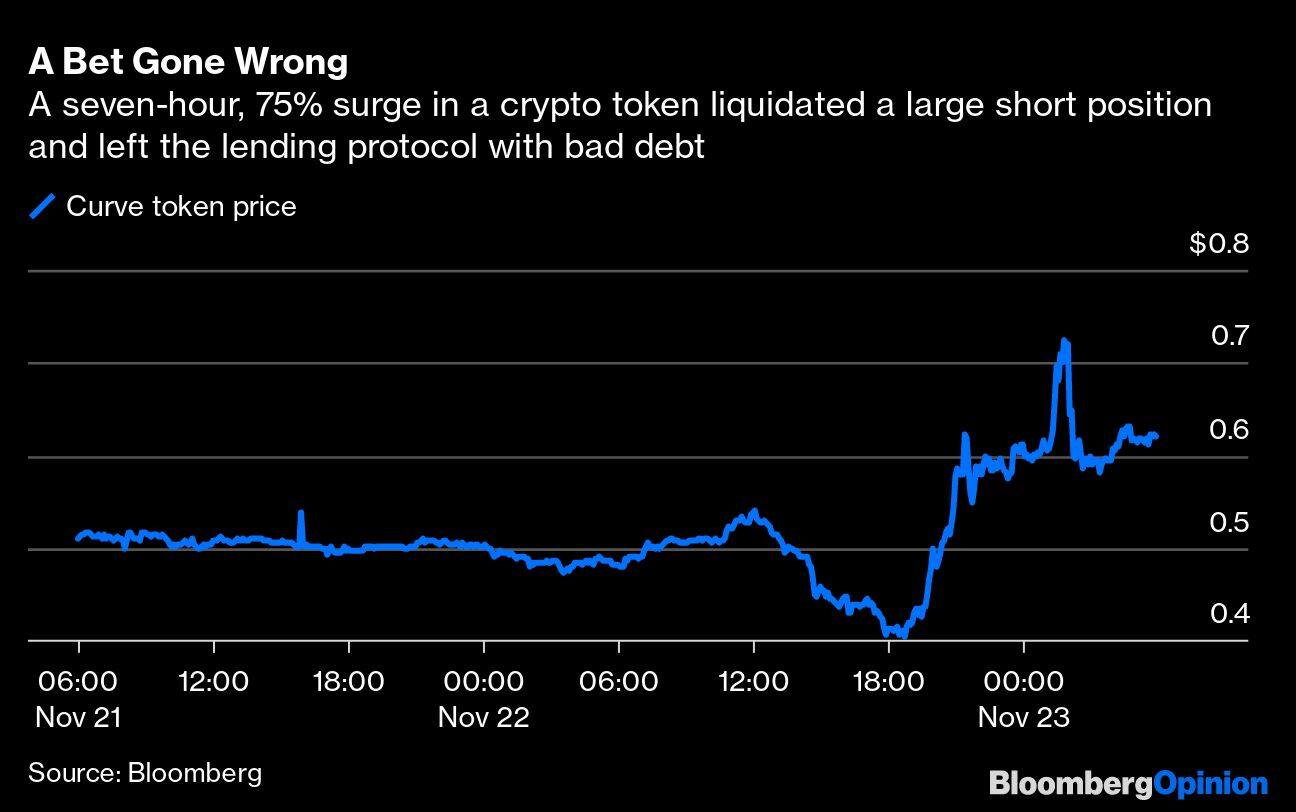

In Eisenberg’s case, there’s nothing remarkable about his own loss. What’s problematic is that Aave, the platform, was left nursing a $1.6 million bad debt after algorithms — taking advantage of a 75% run-up in CRV on Nov. 22 — closed the short position. At first blush, this seems to be a point in favor of the fragility hypothesis of University of Calgary economist Alfred Lehar and Christine A. Parlour, a UC Berkeley finance professor. According to them, a crucial difference between DeFi and TradFi is that the former doesn’t place any capital constraints on arbitrageurs. Is that a problem? Well, it could be.

DeFi borrowing and lending is anonymous. In the absence of credit-scoring, or recourse to the borrower or his reputation, loans must always be worth considerably less than the collateral, especially because the token that’s being borrowed and the coin it’s being borrowed against can both fluctuate wildly. To keep the lending pool secure, algorithms scour digital platforms for breaches of loan-to-value norms. When they zero in on shaky debt — Eisenberg’s position exceeded the system-set permissible LTV of 0.89 on Nov. 22 — they’re programmed to seek a flash loan, use the proceeds to close some part of the original debt, wrest the collateral and sell it to cancel their liability.

Unlike in conventional finance, these four things happen in a single block of validated information. Either the transaction goes through in its entirety and all copies of the distributed ledger reflect it, or not at all. Which is why the bots don’t need to bring in capital to pocket their promised liquidation incentive — 4.5% in the Eisenberg episode. They don’t pose any credit risk to lenders advancing the money to carry out the kill. “Expertise is more likely to be the constraint rather than capital because of the existence of flash loans,” Lehar and Parlour note.

That’s full marks for capital efficiency. But we must also count the cost to the lending system from the absence of friction. And therein lies the nub of the “whither DeFi” debate: Did the bad debt left to Aave result from an irresolvable fatal flaw, or could a design tweak have prevented it?

In a paper covering the episode, a group of blockchain professionals have come up with a possible answer. Beyond a threshold, liquidations on Nov. 22 turned toxic. Each forced closure of his loan made Eisenberg’s remaining position a little riskier when weighed against the available collateral. That, in turn, invited another bot, and the whole thing cascaded out of control. If the fixed 4.5% liquidation incentive had been dynamic, if it had fallen progressively with the thinning of the collateral cover, the platform could have avoided accruing any bad debt.

“Toxic liquidations are dangerous for the protocol since they mathematically guarantee that the user’s portfolio health will worsen through no fault of their own,” Jakub Warmuz and his co-authors note. “As a general rule of thumb, sudden short-minded responses to complex dynamical behaviors lead to outcomes worse than what the response set out to achieve. They should be avoided unless absolutely necessary.”

Fixes need to arrive sooner rather than later. Not because our next mortgage is going to be DeFi — good luck with putting a municipality’s property register on a public blockchain. The main motivation is that a big part of the conventional trade in goods could benefit if decentralized finance allows a crate of wine or the Japanese yen owed by its importer to become an asset on the blockchain. So that money could be raised against it more cheaply than would be possible now after paying fees to middlemen. In November, JPMorgan Chase & Co. did a small trade on Aave, taking its first live position on a public blockchain. With giants of TradFi starting to dabble in DeFi, the whole thing is turning serious.

Whether the future of DeFi is utopian or dystopian isn’t something finance professors or practitioners can determine on their own. A piece of software code acting as a complete contract, leaving no room for courts to intervene if things go wrong, requires us to imagine, among other things, a less salubrious ending to Shakespeare’s “Merchant of Venice.” Legal and cultural philosophers should also bookmark the Eisenberg liquidation. They might have to wade into the debate soon.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services in Asia. Views are personal and do not represent the stand of this publication.

Credit: Bloomberg

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

| 1W returns9.06% |

| 1W returns4.68% |

| 1W returns3.98% |

| 1W returns3.25% |

| 1W returns3.18% |

| 1W returns2.10% |

| 1W returns-0.74% |

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.