Madhuchanda Dey

Moneycontrol Research

In the April 2017 Policy, the Reserve Bank of India was hawkish on inflation and bullish on growth. What has happened over the past two months suggests that its fears and hopes were somewhat misplaced: inflation has nosedived, and so has growth. Will this potent combination of softer prices and faltering growth prompt the RBI to budge?

Not so quickly perhaps. The ground reality might warrant a change in policy stance from ‘neutral’ to ‘accommodative’ before the Street should start expecting a decisive rate cut.

Soft Growth and Benign Outlook The latest GDP print deserves attention. The headline growth number showed the GDP falling to 7.1 percent in FY17 compared to 8 percent in the previous fiscal and the gross value added (measure of real economic growth) falling to 6.6 percent from 7.9 percent in the previous fiscal. In fact, the GVA at constant prices at 5.6 percent in the fourth quarter of FY17 is the weakest in the past two years. However, the number that should really concern policy makers is the investment rate measured by gross fixed capital formation – that has declined from 31.2 percent in Q1 FY16 to 28.5 percent in Q4 FY17.

Can rates revive the economy? There is no straight answer. But the road ahead has multiple soft patches, hence we are quite circumspect about RBI’s bullish stance on growth in FY18.

While prima facie the GST regime is unlikely to be inflationary, we believe industry is likely to pare inventory levels during the transition to the GST, mildly dampening production in Q1 FY18. Moreover, Q2 and Q3 are likely to witness some adjustment as businesses get used to the new compliance procedures and higher working capital requirements. The positive impact of the GST on economic activity is likely to be visible only from Q4 FY18 onward.

The resolution of the bad asset problem through the Insolvency and Bankruptcy Code could exert further pressure on the financials of banks, should the quantum of haircut far exceed the existing provision, and could turn them more risk-averse in the short term. Recent data suggests the deceleration in bank credit continues unabated in the current fiscal.

With growth unlikely to look up in a hurry, is inflation the prime concern?

In April 2017, the MPC had indicated that it expects the CPI inflation to average 4.5 percent in H1 FY2018, before rising to 5.0 percent in H2 FY18, with risks evenly balanced around this projected trajectory.

The headline print shouldn’t worry RBI. The year-on-year (YoY) CPI inflation eased sharply to a series-low 3.0 percent in April 2017, led by food inflation. Moreover, the core-CPI inflation (excluding food & beverages and fuel & light) declined to 4.5 percent in April 2017 from 4.9 percent in March 2017.

The imminent revision in house rent allowance based on the Seventh Central Pay Commission’s recommendations might push up housing inflation in the ongoing fiscal.

However, there are a fair number of tailwinds. As per the projections of the Indian Meteorological Department, India is likely to emerge unscathed from El Nino weather pattern as it is expected to set in only during the latter part of the 4-month monsoon season. Expectations are that price rise is likely to be moderate under MSPs (Minimum Support Price).

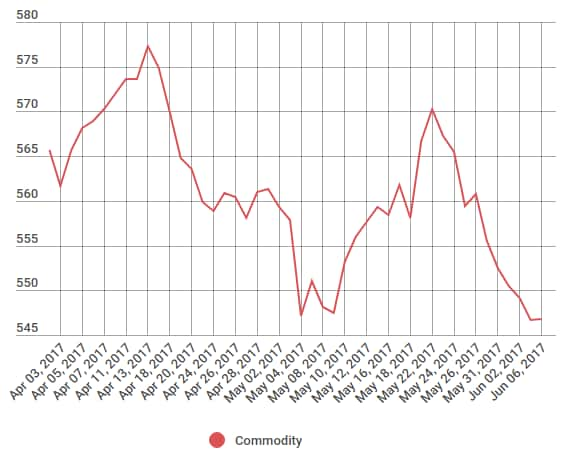

With Trump trade waning, commodity prices have cooled off and are unlikely to rear their ugly head any time soon.

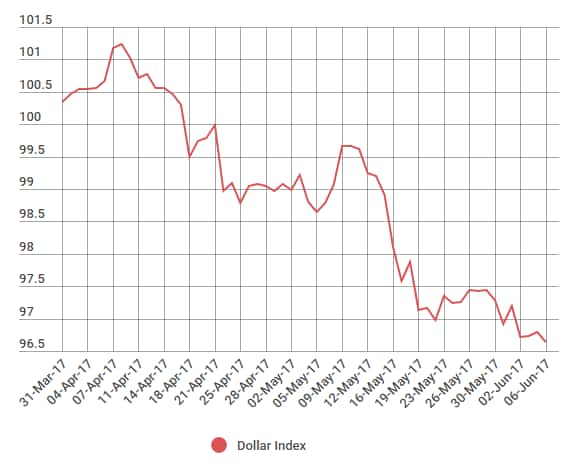

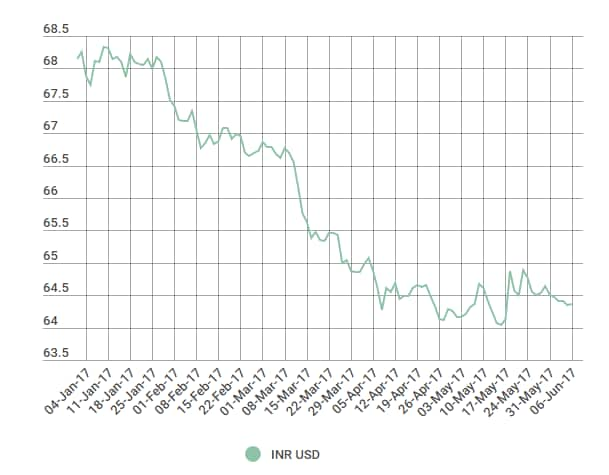

While the strength of the rupee has added to the disinflationary forces, a big reversal of the same is unlikely given the heightened interest of global liquidity for India.

What could go wrong?

What could still emerge as lingering concerns for the RBI is the temporal and spatial distribution of monsoon and its impact on prices. The ongoing unrest by farmers in Maharashtra demanding a loan waiver, and its potential to spiral into a multi-state movement, could also be a matter of concern.

As the Central Bank starts deliberating on its Monetary Policy stance, the Street will be watching out for

• RBI’s change in stance from ‘neutral’ to ‘accommodative’

• The central banks’ take on inflation trajectory

• RBI’s prognosis on growth and GDP in FY18

While the RBI has been given a significant mandate to steer the NPA resolution in the system, the Street, by and large, does not expect the focus of the policy to include NPAs, as it will be dealt with at length separately. A section of the market would perhaps be looking up to the central bank for probable introduction of any new instrument for liquidity management like Standing Deposit Facility (SDF).

In sum, the focus of attention will be on how Urjit Patel and team grapple with the classic growth vs inflation dynamics.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.