Saurabh Mukherjea

Most of the drivers of the current slowdown appear to be transient and related to channel financing/GST credit issues. Understanding why the economy has slowed down at various levels (i.e. consumer, dealer, distributor, and manufacturer) is central to investing sensibly in this time of flux. Whilst heavy repo rate cuts are needed, the notion that structural reform is needed to resuscitate the economy is damagingly misguided.

The reset is now well understood…

Most people now understand that India is gradually transitioning from: (a) a country where it was easy to transact in cash to a country where it has become hard — albeit not impossible — to transact in cash; (b) a country where SMEs routinely used to evade taxes to a country where such routine tax evasion has become much harder; and, (c) from a country where the scope of operation for more than 90 per cent companies was local/regional to a country where a far higher proportion of companies is operating on a nationwide scale, courtesy the much improved transport and communication networks, and due to an integrated nationwide framework for indirect taxes (GST).

Plenty has been written on these subjects. For instance on August 13, 2018, we said in our note to clients: “Small/informal businesses flourish in an underdeveloped economy where due to the lack of availability of electricity, good roads, reliable communication networks and affordable credit, businesses can operate only a small scale and that too within the confines of their immediate locality….India seems to be going through period comparable to what America went through in the 50 years post the Civil War. Over the past ten years, the length of roads in India has increased from 3.9 million km to 5.6 million km (implied CAGR of 4.2%). The number of mobile phone subscribers has increased over the same period from 234 million to 1.2 billion (CAGR of 20%)…These factors have made it easier for smaller companies to build pan-India franchises….It goes without saying that not every small firm will be able to build a national niche. The winners will be those who have: (a) the work ethic to build a pan-India brand and national distributor-dealer networks; (b) the capital allocation skills to rationally & patiently invest in building long term competitive advantages....”

…but the economic slowdown is misunderstood

Yet, although everyone understands that we are in the throes of change, most people — investors & companies alike — find it hard to understand how this change will play out. Who will be the winners and losers? How long will the transition to the new world take? How painful will the transition be? In this note, we offer our few paisa worth of wisdom regarding these questions.

The economic slowdown that is impacting India can be broken down into its constituent components:

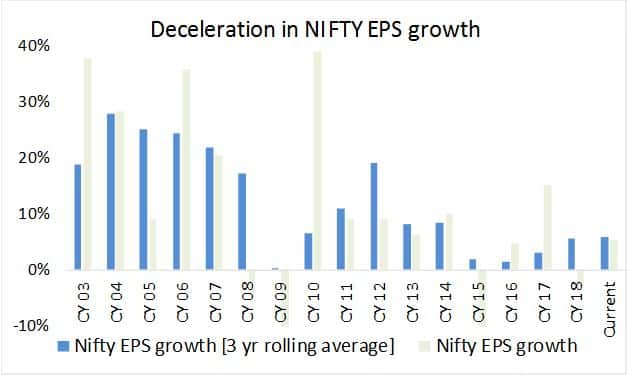

Challenge 1: The capex conk-off a decade ago — The Indian economy’s slowdown started within three years of 2008 Great Financial Crisis. Ever since 2012, India’s earnings growth started decelerating arguably because the era of crony capitalism (during which promoters got easy money from Indian banks and/or global financial markets) ended with the unveiling of the 2G spectrum scam in 2010. As capex growth gradually decelerated, earnings growth for the Nifty started sliding (see chart below created using data from Bloomberg).

The impact on growth of this capex conk-off was buffered by households’ savings rate falling from around 25 per cent of GDP 10 years ago to around 17 per cent now. Basically, as corporates lost the appetite to borrow, lenders focused their efforts on convincing consumers to borrow for homes, cars and washing machines. Obviously, such a savings conk-off could not continue indefinitely. Hence as the household savings rate bottoms out, and by implication consumption (as a per cent of GDP) tops out, the economy feels the full impact of a conked off capex engine. Let’s label this conk-off in demand as S% CAGR.

Challenge 2: Three shocks in three years (2016-2018) — The impact of three big shocks in three successive years, the latest shock being the NBFC meltdown, has impacted demand further (over and above the demand conk off identified in Challenge 1). This impact is multi-faceted and deserves to be disaggregated carefully:

What is transient and what is structural?

Clearly Challenge 1 is not transient. Barring 1994-97 and 2004-10, India has not seen a capex boom ever. Hence it is unlikely that the capex cycle will turn around in a pronounced manner (i.e. 2004-10 style) anytime soon. Furthermore, thanks to the Insolvency and Bankruptcy Code, the crony capitalists who financed India’s capex historically can no longer default on their loans in the manner in which they are historically accustomed to. Therefore, it seems likely to be while before we see a proper capex boom in India.

However, most of the issues pertaining to Challenge 2 appear to us to be transient provided the government (or the global economy) does not deliver yet another adverse shock. Three weeks ago the finance minister promised to address the GST credit issue which is bedevilling the entire distribution chain.

Second, we are aware that several lenders are working on providing channel financing constructs which address the needs of dealers. Third, the falling prices of steel, rubber, land and capital mean that prices should come off for most products thereby allowing the economy to adjust to a lower level of demand. This is how free market economies adjust to demand shocks. This is how the Indian economy is likely to adjust.

Overall therefore whilst the S per cent conk-off appears unlikely to go away, K, M, P & J per cent look likely to be gradually addressed over the coming year. Hence we do not buy the argument that something fundamental is broken in the Indian economy and structural reforms are the need of the hour. In fact, we would argue rapid structural reform has resulted in many of the issues highlighted above!

To ask for more structural reform at present is therefore misguided. That being said, a logical response to the reduced demand highlighted above would be for the Reserve Bank of India (RBI) to highlight a glide path towards significantly lower interest rates over the next 12 months. We reckon as much as 200bps of repo rate cuts over the next two years could be warranted given the severity of the two challenges outlined in the note.

Investment implications: How can we make money in this slowdown?

Saurabh Mukherjea is the author of The Unusual Billionaires and Coffee Can Investing: the Low Risk Route to Stupendous Wealth, and founder of Marcellus Investment Managers. Views are personal.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.