Moneycontrol Research

We are recommending Marico as a tactical idea. Unlike frontline FMCG stocks like Hindustan Unilever (HUL), Dabur, Britannia Industries, Marico's stock performance has been uninspiring over the last one year. In fact, the stock had corrected 15 percent from its December 2018 high. Recently, we are seeing the stock move out of a consolidation range. This apparent technical breakout seems to be backed by improving fundamentals.

What make us constructive on the stock?

Domestic volume growth: In a recent business update, the management mentioned that Q4 volume growth is in line with its near-term outlook, translating to around 10 percent volume growth. While it is positive on the prospects of its flagship product – Parachute (36 percent of sales), it is also witnessing improving signs for Saffola edible oil (18 percent of sales) – the erstwhile area of concern.

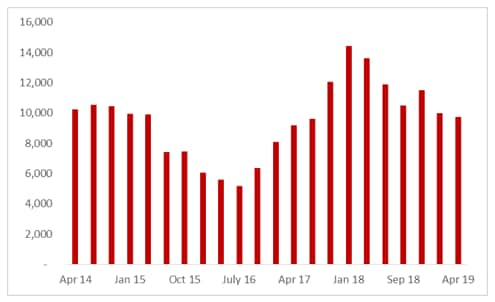

Copra Calicut prices (Rs/100 kg)

Copra cost deflation cycle The management expects operating margin to improve moderately as input costs have eased and operating leverage benefits are also expected to show. Here, the key factor influencing it is the copra cost deflation cycle.

It expects a substantial decline in copra prices (around 20 percent year-on-year) in the new season from March. As copra constitute about 45 percent of raw material cost, this should help company’s earnings in a significant way.

Investment towards diversification The management’s decision to invest raw material cost advantage for long-term investments is a crucial strategic move as it helps in reducing dependence on Parachute and Saffola and drive growth in the premium segment. In this context, we expect categories like male grooming, serums, hair nourishment and foods are expected to have a significantly higher share in the next five years.

Urban-centric trade channels doing well

Urban-oriented channels such as modern trade and e-commerce continue to do well. Share of modern trade in total turnover is expected to be way higher in the current fiscal compared to last fiscal, when it clocked 11 percent of sales. Similarly, as per Q3 update, e-commerce share has already crossed three percent compared to less than a percent a year back.

Risk factors The key risk factor is if the copra deflation cycle doesn’t play out as expected. Along with that, continuation of rural distress can also be a drag, particularly if there is a weak monsoon this year. A partially comforting factor is Marico’s rural exposure (about 30 percent) is relatively lower than major FMCG names – HUL, Dabur and Emami.

Currently, the stock is trading at 40 times FY20 estimated earnings, which is an about 16 percent discount to the market leader. At current levels, the stock provides an accumulation opportunity for an increasingly diversified consumption story.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.