UPL, the undisputed king of the agrochemicals sector in India, has been plagued with problems in the last one year – declining growth, a drop in chemical prices across the world, and perhaps the biggest of them, a sticky debt. As a result of this, analysts are increasingly turning bearish on the counter.

Take a look at the data: just a year ago, about 93 percent of analysts or 28 out of 30 had a BUY call on the stock. That number is now 77 percent, or 23 out of 30.

This shows even though a large section of analysts are still bullish, UPL is among those names that have seen maximum analysts turning bearish during the last one year. Even the few of those who have maintained BUY calls have either cut down target prices on the stock or their revenue and EBITDA estimates.

Also read: UPL Q1 Results: Net profit plunges 81% to Rs 166 crore, misses expectations

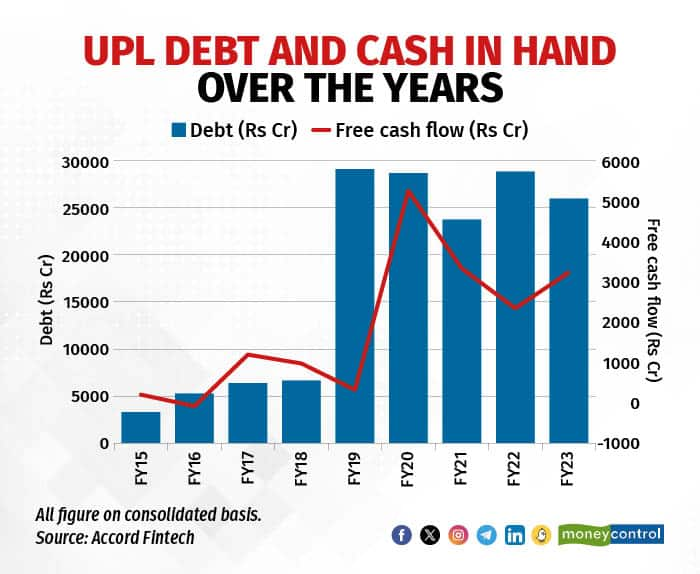

The big fat debtAs per data available with Accord Fintech, UPL had a consolidated debt of Rs 26,000 crore as of FY23-end. Though the debt has reduced compared to previous years, it is still relatively high, eating into the company’s profits as finance costs remain a burden.

Moreover, the UPL’s cash flow has been erratic and has come down sharply from the highs of FY20. This also makes reducing debt at a rapid pace a tall task. Recently, analysts noted that its working capital days increased due to reduced factoring and lower payable days, affecting net debt and cash generated by the business.

Still, the company is aiming to reduce its net debt in the medium term, with a focus on bringing the Net Debt/EBITDA ratio below 1x and maintaining its ‘investment grade’ credit rating. During Q1, the company said, it reduced its net debt by $160 million (about Rs 1,330 crore) on a year-on-year (YoY) basis with a plan to bring it down further during the year.

Another trouble for the agrochemical company is lower sales in North and South America and Europe. During Q1 of FY24, its revenue from North America declined 52 percent YoY due to channel inventory-led challenges coupled with lower volumes and pricing pressure in glufosinate, s-metolachlor and clethodim products. Latin America revenue declined 14 percent YoY led by a decline in non-selective herbicides. Its India revenue too has seen stagnation.

These challenges along with a drop in chemical prices do not bode well for the near term as well.

“We see near-term challenges in the global agrochemical industry due to the accumulation of high inventory as distributors are opting for need-based tactical purchases, and declining agrochemical prices, led by aggressive price competition from Chinese post-patent exporters,” said Sumant Kumar, Research Analyst at Motilal Oswal. “Considering the short-term challenges, cash flow generation and debt repayments remain the key monitorables.”

Also read: Sluggish demand, unclear debt reduction target push UPL into a pool of downgrades

The outlookMost analysts believe the next couple of quarters will be tough for UPL’s business. They see the company’s revenue growing in low single digits while its EBITDA rising in mid-single digits over FY23-25. This is after they have cut down their earlier estimates.

![]()

The stock price has also followed these expectations. UPL stock is down about 16 percent so far in this calendar year. In the last six months, it is down 17 percent. Thanks to falling prices, the consensus target of Rs 769 is showing a potential upside of 27.6 percent in the next 12 months.

Investors and analysts will now keep an eye on the performance during the second quarter of this fiscal.

Disclaimer: The views and investment tips expressed by experts are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before making any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.