Family floater plans are linked to the age of the eldest member of the family and higher the age, higher the cost of the premium. Hence, in such cases a floater health insurance policy may not be the best option for families where the eldest member is over 45 years.

Anurag Rastogi, Member of Executive Management, HDFC ERGO General Insurance, has some words of advice in this scenario.

“If one of the aged parent suffers from a serious medical ailment, a floater cover may not be suitable, as the other members may get deprived of the cover in case the entire sum insured gets exhausted for treatment/ hospitalisation of aged parent during the policy tenure,” he said.

Buy separate policies for elderly parents“Buy separate floaters plan wherever there is a generational gap as it may impact the premium and coverage. For elderly parents one must always look at a separate policy as it is cost effective than buying together with self,” said Vaidyanathan Ramani, Head Product and Innovation, Policybazaar.com.

Senior member of the family might be suffering from existing illnesses. This may require pre-policy medical check-up before issuance of policy. Jyoti Punja, Chief Customer Officer, Cigna TTK Health Insurance cautions, “In such situations, the proposal can get rejected/loaded/accepted at same rates or with special conditions. This in turn may hinder seamless inception of risk coverage.”

“While buying the health insurance policy for aged parents check the basic coverage, waiting period of pre-existing diseases, sub-limits, etc, under the policy. Also, medical inflation is increasing 15% annually and hence it’s vital to have an option of upgrading the sum insured while renewal from your insurer,” said Bhaskar Nerurkar, Head, Health Administration Team, Bajaj Allianz General Insurance.

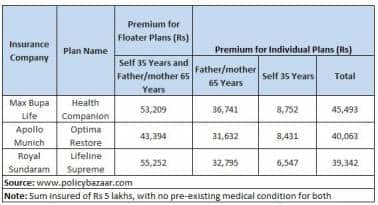

Illustration of self and elderly parent taking individual and floater plans

When you do not make any claim in your health plan, you are entitled to a No Claim Bonus (NCB) in the subsequent year. In floater plans any claim by any member affects the no claim bonus. “So, if elderly parents share your family floater cover, being aged, they might require frequent medical assistance. So, the probability of making a claim in your floater plan increases and you may lose out on the accumulation of NCB,” said Punja.

Tax saving under section 80D for paying medical insurance premium can be taken for both self and parent (senior citizen) policies which may not be possible if parents are covered in a single family floater policy. If your aged parents, or either of them i.e. father or mother are senior citizen, the maximum limit goes up to Rs 30,000 a year.

Limit on Deduction under Section 80 DUnder Section 80D, you can claim the tax benefit subject to the health insurance premiums paid for your family (including your spouse and children) and parents, which are different from the benefits, based on costs related to health check-ups. The deduction limits are as follows:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.