If you had sold shares, mutual funds, jewellery, real estate and so on in financial year 2022-23, you might have ended up with capital gains or losses. Make sure you disclose it properly while filing your income tax return (ITR) this month.

Remember, capital gains and losses are taxed differently and there are specific ITR forms that you need to select for filing of returns. Let’s delve deeper into capital assets, treatment of gains and losses from transactions in capital assets and applicable ITR forms.

Also read: MC Explains: How to get your capital gains statement for MF investments

What are capital assets?

As per the income tax rules, various types of properties held by an assessee, regardless of their connection to the assessee's business or profession, are considered capital assets. This includes land, houses, shops, and apartments, as well as investments in financial instruments such as shares, mutual funds, and gold bonds.

In addition, items like jewellery, valuable gemstones, ornaments made of precious metals like silver, gold, or platinum, archaeological collections, drawings, paintings, sculptures, or any other form of artwork, even if used for personal purposes, are also classified as capital assets.

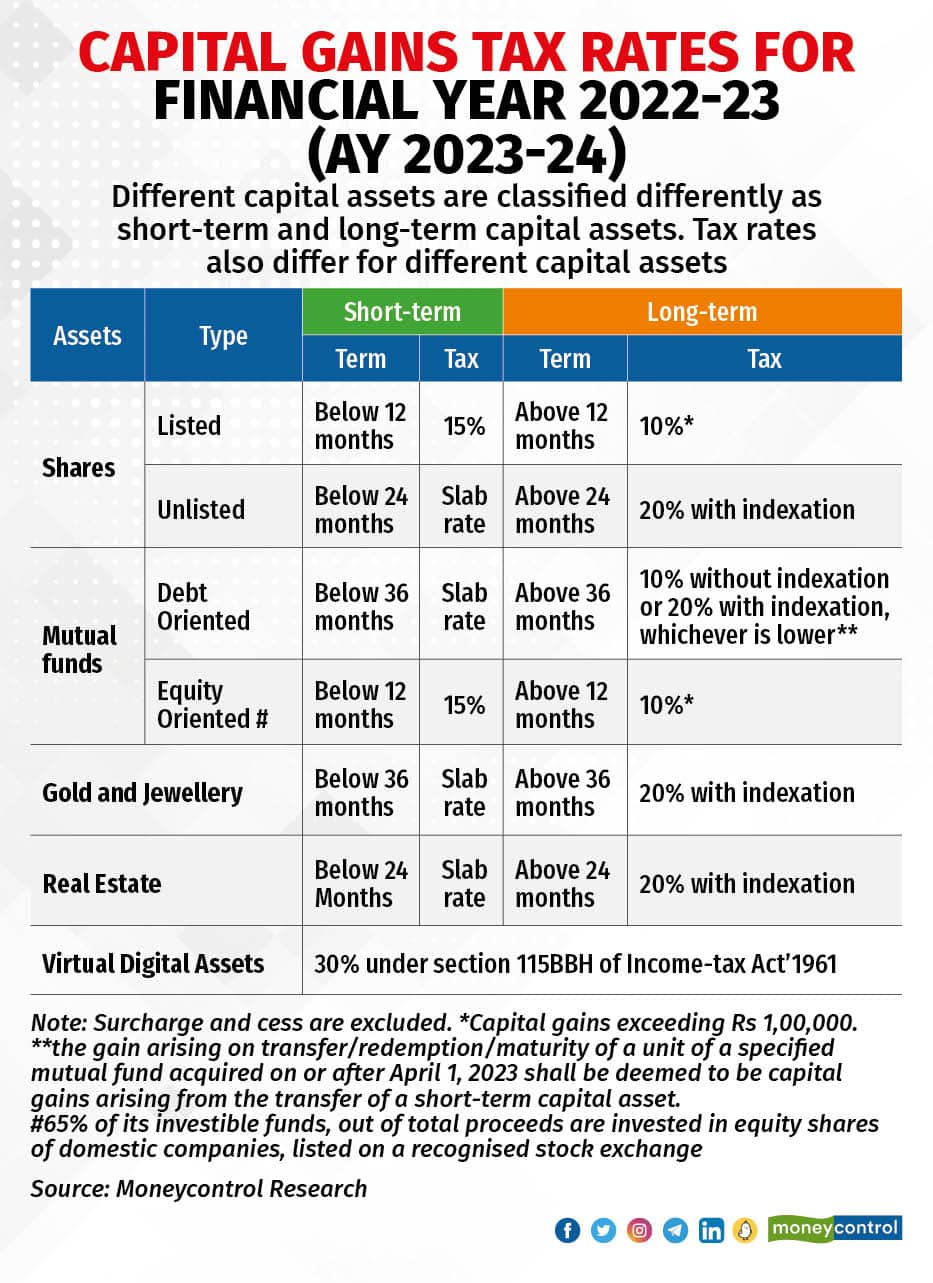

Meaning of short-term and long-term capital gains

A capital asset held for a period of more than 36 months before its transfer is classified as a long-term capital asset (LTCA). However, there are certain exceptions for specific assets. For instance, for shares listed on recognised stock exchanges, units of equity-oriented mutual funds, listed securities like debentures and government securities, and zero-coupon bonds, the holding period is 12 months or more to be considered as LTCA.

Unlisted shares in a company are considered LTCA if the holding period is 24 months and above. From the Assessment Year 2018-19, the holding period for immovable property (land or building) has been reduced to 24 months from 36 months earlier.

Also read: Planning to sell your property? Know your responsibilities as a seller

The treatment of gains and tax rates differ for different assets. In some cases, the nature of gains from capital assets also differs based on how it was transferred. For instance, where the property is transferred without consideration or for inadequate consideration, the same would be subject to tax as income from other sources u/s 56(2)(x) of the IT Act in the hands of the recipient of such specified property.

Also, “taxpayers dealing in futures and options trading, or intraday trading of shares and securities need to offer the gains or losses from such trading activities under the head business income. Similarly, taxpayers who trade significantly in shares and securities are allowed to classify income from such trading activities under business income,” said Sudhakar Sethuraman, Partner, Deloitte India.

Set-off and carry forward of capital loss

Adjusting losses from transactions in capital assets against income from salary, business, or profession to reduce net income and tax liability is not permissible under income tax regulations.

“Taxpayers need to keep in mind that the IT Act does not allow loss under the head “capital gains” to be set off against income from other heads,” said Suresh Surana, founder, RSM India.

However, “capital loss arising from one capital asset can be set off against losses arising from another capital asset subject to certain conditions,” added Surana.

These conditions state that, “Short-term capital losses can be set off against both short-term as well as long-term capital gains. Long-term capital losses can be set off only against long-term capital gains,” he explained. However, capital losses from Virtual Digital Assets (VDAs) like cryptocurrencies, and non-fungible tokens (NFTs) are treated differently. “No capital losses can be set off against gains from VDA nor any capital loss from such VDAs can be offset against any other capital gains,” said Surana.

If you have incurred long-term capital losses that cannot be set off against income in the same year, you have the option to carry forward those losses to offset against potential gains in future years. “Capital losses which cannot be set off during the relevant financial year would be allowed to be carried forward for 8 years immediately following the year in which such loss is incurred,” said Surana.

This allows you to utilise the losses effectively and reduce your overall tax liability over time. However, in order to carry forward the losses, it is crucial to fulfil a key requirement, which is filing the tax return within the stipulated due date i.e. July 31 of the assessment year.

Also read: Moneycontrol's income tax return (ITR) filing guide for FY 2022-23 (AY 2023-24)

Basic exemptions and deductions

In addition to offsetting losses against gains, another factor that reduces tax liability on income is the availability of exemptions and deductions. However, when it comes to long-term capital gains (LTCG), claiming the usual deductions against this type of income may not be possible, although basic exemptions can still be claimed.

The basic exemption limit means the level of income up to which a person is not required to pay any tax. The basic exemption limit applicable in case of a resident individual below the age of 60 years for the financial year 2022-23 is Rs 2.5 lakh, for resident individuals of the age of 60 years or above but below 80 years, the exemption limit is Rs 3,00,000.

For resident individuals of the age of 80 years or above, the exemption limit is Rs 5,00,000. For non-resident individuals, irrespective of the age of the individual, the exemption limit is Rs 2,50,000 and for Hindu Undivided Family (HUF), the exemption limit is Rs 2,50,000.

One more thing to remember is that you can adjust the basic exemption limit against LTCG but such an adjustment is possible only after making an adjustment of other income. In other words, the first income other than LTCG is to be adjusted against the exemption limit and then the remaining limit (if any) can be adjusted against LTCG.

It is important to note that deductions under sections 80C to 80U cannot be claimed from LTCG. This means that investments made in life or health insurance, public provident fund, equity-linked savings schemes, NPS, and other eligible deductions in case of salary or business income cannot be claimed against LTCG.

In certain situations, it is possible to reduce your tax liability on LTCG or even avoid paying taxes altogether by reinvesting the profits. For example, if you sell a residential property and earn LTCG, you can save on taxes by reinvesting the gains within the specified timeframe. This can be done by investing in 54EC bonds or purchasing another residential property. Read more here:

Which ITR form to select?

There are different types of ITR forms to choose from based on the source of income and level of income. “Taxpayers having gains or losses from capital assets are generally required to fill ITR-2 provided they do not have gains or losses which are to be taxed under the head business income. In such a case, taxpayers must file ITR 3 and for those opting presumptive taxation only can file ITR 4,” said Sethuraman.

Selecting the correct ITR form is a must, filing a return in the wrong ITR form makes it invalid or will be considered as not being filed at all.

Also read: How to select the right ITR form

Things to keep in mind while filing return

Appropriate and accurate reporting of income from capital assets is crucial when filing ITR. Sethuraman mentioned that some of the relevant considerations while filing ITR with income from capital gains include the classification of gains or losses appropriately between long-term and short-term.

He also said that quarterly reporting of gains is mandatory for the purpose of computing interest for delayed payment of advance taxes. So if you have made any capital gains in the first quarter of the financial year and not paid any advance tax, then the due tax will attract interest on a per month basis.

Also read: Know how to calculate your advance tax liability

Also, remember that there have been a lot of amendments in the calculation and taxability of capital gains from different assets, so keep a watch on this, especially in the case of LTCG. For instance, Sethuraman said that “taxpayers holding investments prior to January 31, 2018, must report the long-term capital gains security wise to arrive at the Fair Market Value as on January 31, 2018, for the purpose of computing capital gains.”

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.