Maneesh Joshi, a 39-year-old Mumbai based documentary producer and director, is quick to emphasise on the financial goal of funding his son’s higher education.

While his 7-year-old son Rikhil Joshi is busy with class III studies, the father has all the plans in place to fund his education. Maneesh invests regularly in equity mutual fund schemes to ensure that he gets a sizeable corpus over a long-term. He is also investing in fixed deposits to balance the risk.

“It is too early to talk about Rikhil’s academic choices. He may go overseas for higher education or may choose a premier institute in India. Whatever he chooses, I should have the corpus ready,” says Maneesh Joshi.

Setting the goal right

Education has become a significant cost head for most urban middle-class households with kids. Personal finance experts are quick to point out that though the school education is relatively expensive compared to what it was two decades ago, the regular income is sufficient to pay for the school education. The challenge is in the form of funding the higher education, typically the post-graduate or masters studies.

Even if many parents are aware of the need to create a corpus for education, most parents find it difficult to estimate the costs they would incur on their kid’s education. There are two factors that make an estimate difficult – first, it is a long term goal and second, they do not know which course the child will opt for.

“It is all about assumptions now. So you should be focussing on what you can afford now,” says Pankaj Mathpal, founder and CEO of Optima Money Managers.

For example, if you think an engineering degree is a minimum you would be willing to pay for, start with it. If it costs Rs 10 lakh, then apply inflation to it. “Education costs in Indian premier institutes are escalating at 10 percent CAGR and hence you should factor in that in all your estimates,” says Mathpal.

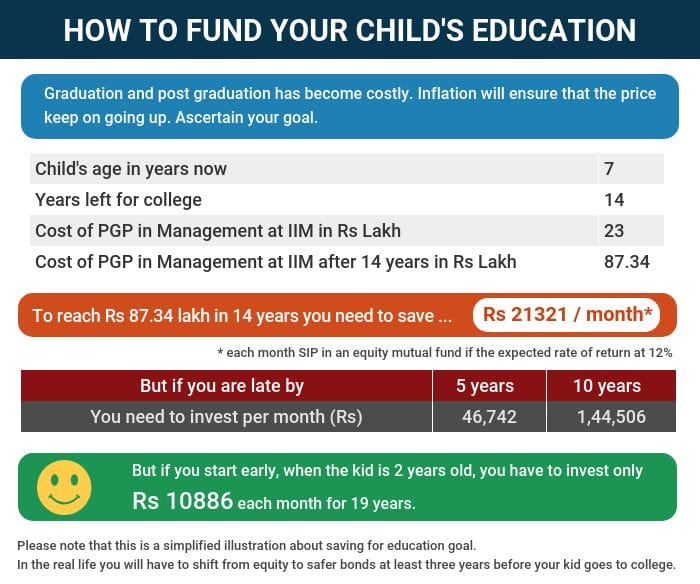

If Rikhil Joshi decides to opt for a post-graduate programme in management at IIM Ahmedabad 14 years from now, then he should be prepared to pay Rs 87.37 lakh. It costs Rs 23 lakh now.

If you expect your kid to take up specialisation overseas, you have to factor in that cost too. “If you expect your child to go overseas, do take into the education inflation in that country and the currency impact,” says Vishal Dhawan, founder and chief financial planner, Plan Ahead Wealth Advisors.

If your child aims to go to the US for higher education, consider the rate of education inflation (around 5 percent) in the US and the foreign exchange rate movement in the US dollar and Indian rupee. We inflate the goal value by 9 percent to factor in both these factors, says Dhawan.

Though the numbers may look simple, do not forget to add on other lifestyle costs. “If your child is going overseas or plans to stay in a different city, then the cost of education also includes travel costs, hostel expenses that can be a sizeable amount. Do account for it in your calculations,” says Ravindra Deshmukh, certified financial planner and founder of Pune based Arthamitra Wealth Creators.

Investment plan

Financial planners advise staying away from child focussed products as many of these come with problems such as high costs, stringent conditions about payoffs, lack of intermittent liquidity among others. For example, we come across many child plans that promise to pay in instalments when the child reaches the age of 18, 20 or 22.

The issue is education related payments may not happen at that time and one may have to run from pillar to post to tide over intermittent cash needs. One may be forced to take costly short-term personal loans.

Same is the case with Sukanya Samriddhi Yojana (SSY). It is one of the best investment options available for a girl child as it pays the highest tax-free rate of interest with a sovereign guarantee. But the payoffs take place when the girl child turns 18 and 21 years of age. The education provider won’t wait for payments in the interim period.

Mutual fund schemes dedicated for funding child’s education come with a lock-in typically till the child turns 18 years of age and they invest heavily (around 65 percent to 75 percent in stocks). If your lock-in period does not let you shift your money to safer fixed income options well ahead of your financial goal, there is a chance that you will see the corpus value erode if there is a massive correction in the market.

It is better to start with two important numbers – the future value of the goal and the time on hand. If Maneesh Joshi wants to fund Rikhil’s education at IIM, then he should be investing Rs 21,321 each month for the next 14 years if the expected rate of return is 12 percent.

Manage cash flows

Financial planners emphasise on the ‘in-built flexibility’ in your investment plan. “When we are saving to create an education corpus, we do not know how the future will be. The cash flow needs may be far different from what we foresee them now,” says Dhawan.

Consider a situation wherein an individual has planned for graduation in an Indian institute and post-graduation in an overseas institute, but the reverse happens. In such a case, the amount and timing of cash flows will widely differ from what was envisaged.

Handling cash flows are a tricky area for most parents. “You can postpone your foreign vacation dream by a year or two just because you are running short of money. But your kid’s education can’t be postponed,” says Mathpal. Many individuals buy a property or land and earmark it for funding their kid’s education. Such individuals should be selling that asset much ahead (at least two years) of the timing of payment. That said, physical assets like land or a house to fund a future financial goal are best avoided because of liquidity problems.

Have you started late?

All is well if you have started early in your life. But if you have started late, then you will find it tough to raise a large sum of money in the short span.

If Maneesh Joshi decides to fund his son’s education seven years from now, he will have only seven years on hand to accumulate Rs 83 lakh. In that case, he will have to invest Rs 68,455 per month, assuming his equity fund grows at 12 percent rate of return.

A word of caution

Do not fall for any gimmicky investment plan. Instead, increase your saving and investment if you have the child education goal in your financial plan. “Whatever fund you may have created over your earning lifetime, can be supported by education loans which are relatively cheap. Do not dip into funds for your retirement,” says Deshmukh. Always remember that you can get a loan for anything from buying a home to fund education. But you won’t get a loan to fund your retirement.

When you plan it well, there is a high chance that you will accumulate the desired corpus. Many times you may start small but as your income increases, you can make up for the shortage in the past. However, do not forget to buy adequate term life insurance for yourself. Even in case of eventuality, the education of the child must happen as per plan.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.