Foreign education doesn’t come cheap. As per Moneycontrol's calculations, you need to set aside Rs 1.25 lakh – 1.75 lakh a month to pay for your kid’s foreign education. But two other sources of money help: loans and scholarships. Let’s talk about loans. And see if you’re eligible for one.

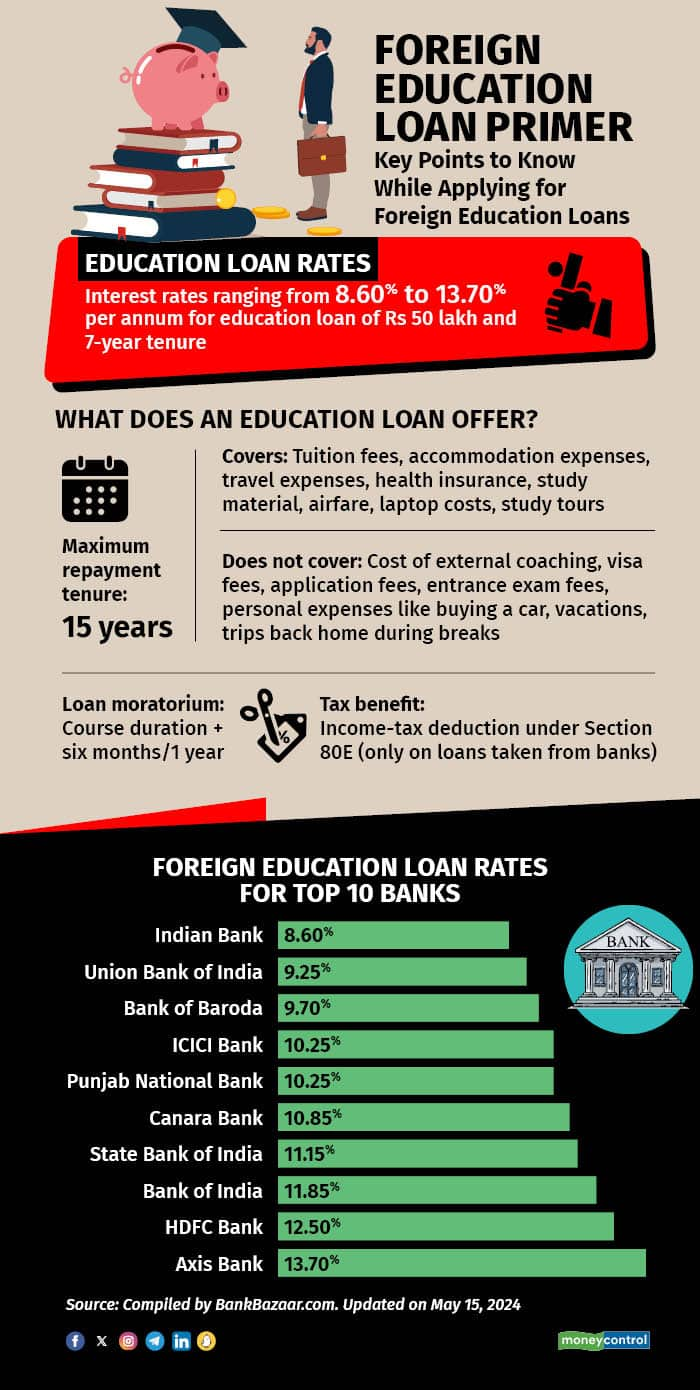

Most banks have dedicated loan schemes for students planning to study overseas. These banks offer foreign education loans at interest rates that ranged from 8.60 percent to 13.70 percent per annum as of May 15, 2024, as per data compiled by BankBazaar.com.

Also read | How to plan financially for your child’s foreign education

What it covers and what it doesn’t

An overseas education loan covers expenses such as tuition fees, accommodation, travel, insurance, books, and equipment for courses such as a laboratory apparatus or a laptop. Other expenses directly related to education such as resident permit charges, student union fees, library fees, and laboratory fees are also covered.

Not everything gets covered, though.

“They won't pay for your study visa, any fees for entrance exams like the IELTS or GRE, or application fees for the colleges you want to attend,” says Ankit Mehra, co-founder of GyanDhan, a firm that offers education loans.

“Students should be aware that certain costs such as extracurricular activities, buying a car, vacations, and personal expenses will not be covered by education loans,” adds Akshay Chaturvedi, founder of Leverage Edu, a platform that helps students with course shortlisting, applications, visas and education loans.

Also read | Studying abroad? Beyond college fees, here are 5 additional costs you should budget for

Evaluation parameters

The amount of loan that gets sanctioned depends on the country of study. That’s why banks evaluate admission letters.

“One crucial aspect is the applicant's academic performance, which includes past academic records, standardised test scores (GRE, GMAT, SAT, TOEFL, or IELTS), and proof of admission to a recognised foreign institution,” says Mehra.

The student and co-applicant’s financial background and credit scores are assessed. The institute’s pedigree matters “because that has a bearing on future employability and earning potential,” says Chaturvedi.

Banks or finance firms?

On account of access to cheaper funds, banks typically offer lower and more competitive interest rates than non-banking financial companies (NBFCs).

It’s best to apply to multiple lenders simultaneously for an education loan.

“This helps if one lender delays sanctioning your loan, a back-up helps,” says Prashant Bhosale, founder of Kuhoo Fintech, an online student loan platform. Multiple sanction offers enable students and parents to negotiate better terms such as loan amount, tenure, repayment models, and interest rates, he adds.

"While shortlisting lenders, compare interest rates, keep an eye on hidden charges and find out if there is a prepayment penalty, among other things," says Arindam Sengupta, co-founder of Edufund, an investment advisory firm that provides education counselling, besides advice on investing for children's education overseas and applying for education loans.

Education loan from overseas

For students who lack both collateral and a financial co-applicant, an education loan from a foreign lending institution is an option. Prodigy Finance and Mpower are international lenders for foreign education. They provide education loans for select courses and universities.

However, the decision to take a loan from an overseas firm depends on various factors and students should carefully evaluate them before proceeding. Check the lender's pedigree.

There are many lenders out there which are not reputed. They might be misguiding the students.

“Borrowers should also keep in mind that international lenders do not provide loans for all countries,” says Mehra.

“The weakening rupee against the dollar means that earning in rupees and repaying a dollar EMI will become increasingly burdensome,” says Saurabh Jhalaria, head of SME and education lending at InCred Finance.

Also, these foreign exchange fluctuations will entail that any advantage because of lower rates is levelled over the tenure of the loan, he adds.

Collateral for the bank

Common forms of collateral include residential or commercial property, non-agricultural land with boundaries, and fixed deposits.

“Lenders do not accept as collateral agricultural land or land that falls under the jurisdiction of a gram panchayat,” says Mehra.

Banks may also accept life insurance policies, stocks, mutual funds, and government bonds as collateral. The value of the collateral should typically cover the loan amount.

“It's essential for applicants to provide clear titles and ownership documents for the collateral to avoid delays in the loan approval process,” Mehra adds.

The specific requirements for collateral can vary between lenders.

"However, if you have secured admission in, say any of the top 10 or 20 universities, some lenders could give you a zero-collateral loan," says Sengupta.

There is flexibility in NBFCs for collateral. Unlike traditional banks that often require collateral, NBFCs like InCred Finance assess loan applications based on the student's academic potential, chosen course, and study location.

Also read | Travelling abroad to study? Here are the best ways to carry forex

Repayment time

The maximum repayment tenure offered by lenders such as Bank of Baroda and Union Bank of India is 15 years (after the moratorium period), irrespective of the quantum of loan. Most NBFCs and fintech companies don’t provide education loans for such a long tenure.

Repayment of an education loan typically begins after the moratorium period, which usually lasts for the duration of the course, plus an additional six months to one year.

“The ideal advice would be to get a long-tenure education loan. After passing and joining a firm, save as much as possible, and repay the loan early,” says Mehra. Paying simple interest during the moratorium period is a good strategy to prevent interest from accumulating, he adds.

Also, before applying for an education loan, you must check whether the bank, NBFC or fintech calculates the interest amount on a reducing balance or flat rate basis. Interest calculation on reducing balance can considerably lower the effective interest rate.

Also read | Five common education financing pitfalls you must steer clear of

Tips to make your loan application stronger

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.